English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The Fed will not tolerate a cooling labor market, and Jerome Powell is firmly in control of the central bank's actions. These are the two key takeaways from the September FOMC meeting. Nine out of 18 committee members predict a reduction in the federal funds rate by 25 basis points or less by the end of the year. However, nearly all of them, except for Michelle Bowman, voted to cut it by half a percentage point. It seems that the Fed chair found convincing arguments to persuade the dissenters, which pushed EUR/USD quotes to their August highs, though the pair could not break through.

Back at Jackson Hole, Jerome Powell made it clear that inflation was no longer the Fed's primary concern. The central bank is now more focused on the labor market, where unemployment was rising rapidly at that time. Theoretically, this could indicate an impending recession. However, the Fed is aiming for a soft landing, and Powell appears ready to replicate Alan Greenspan's achievement from 1995 when he successfully navigated similar challenges.

Today's situation shares many similarities with events 30 years ago. Just like back then, the Fed began cutting rates when the average job growth dropped from +300K to +100K. The economy was not in a recession, but there were talks of an impending downturn. In the 1990s, derivatives markets anticipated a 200 basis point cut in the federal funds rate, but in reality, the reduction was only 75 basis points. It's possible that the current market appetite is similarly overestimated.

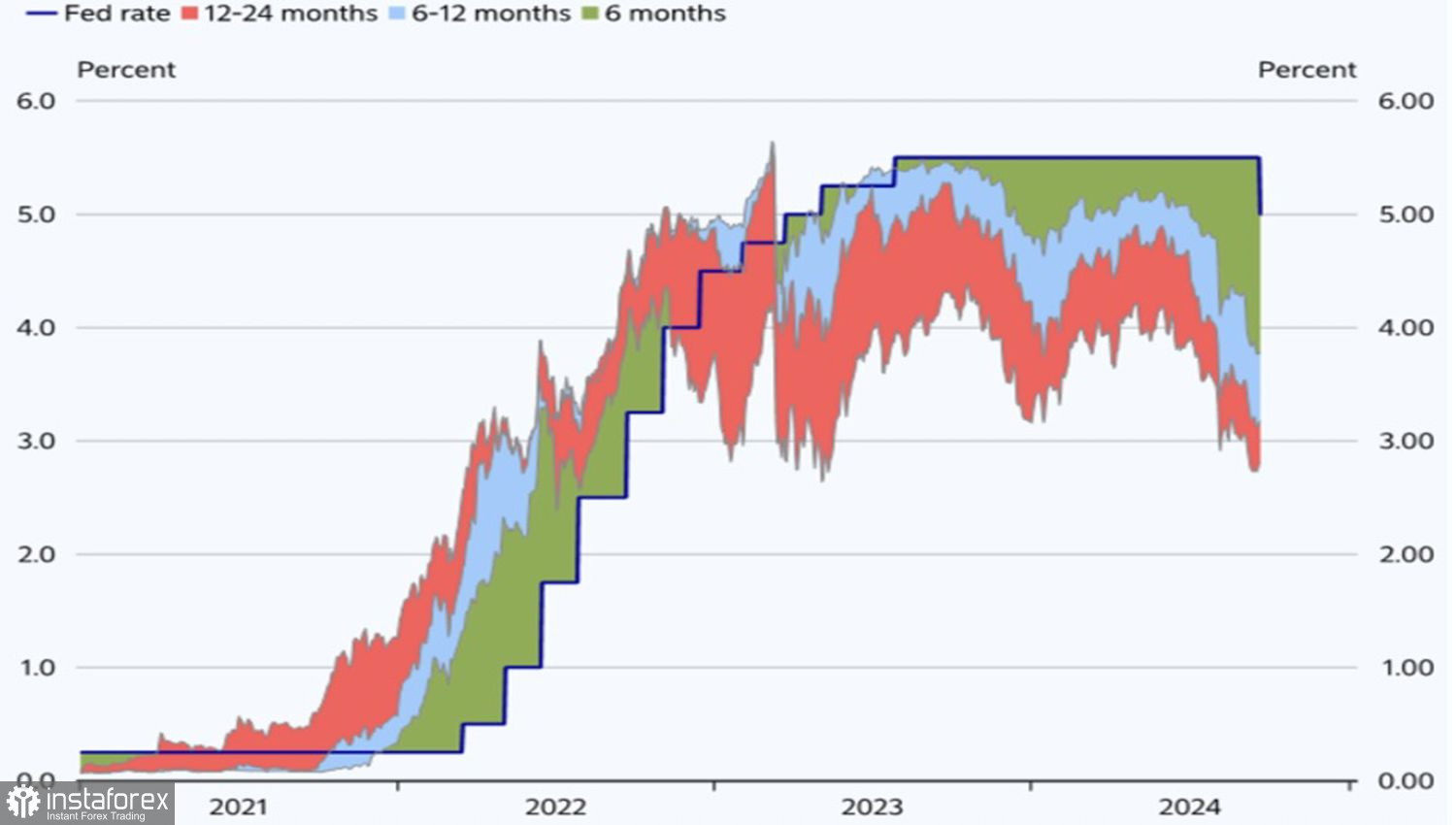

Market Expectations for the Fed Rate

The market forecasts a borrowing cost drop to 2.75% within 12 months, which is notably higher than the FOMC's consensus estimate of 3.25%. This suggests that investors are expecting rate cuts of 225–275 basis points in this cycle, factoring in the September reduction. Meanwhile, the Fed is aiming for a reduction of 175–225 basis points. Drawing parallels to 1995, the final outcome might be closer to 100–125 basis points.

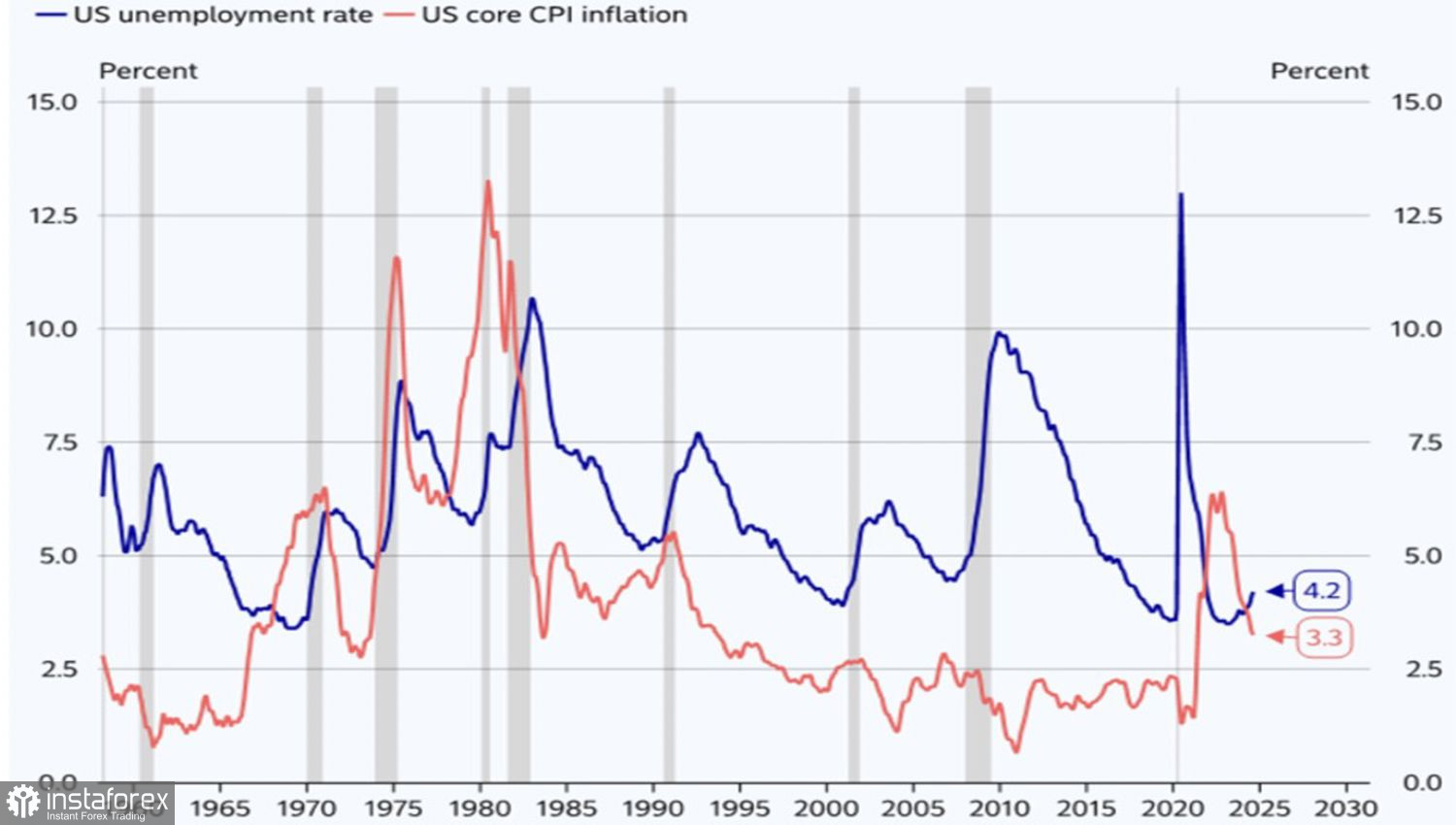

Indeed, if the Fed focuses solely on the employment mandate, it risks overlooking inflation. Who's to say that inflation won't accelerate again amid a still-strong economy and labor market? Yes, the central bank believes it has tamed the inflationary dragon, but could it fall into the same trap as before? In the 1970s, victory over high prices was declared, but when they began to rise again, the tightening of monetary policy had to be resumed. The U.S. economy paid the price with a double-dip recession.

Inflation and Unemployment Trends in the U.S.

For a long time, the market's focus has been on the Fed's monetary policy. However, as the U.S. presidential election approaches, investor attention may shift to the race between candidates. The approval ratings of Kamala Harris and Donald Trump could become just as important as the release of PCE data.

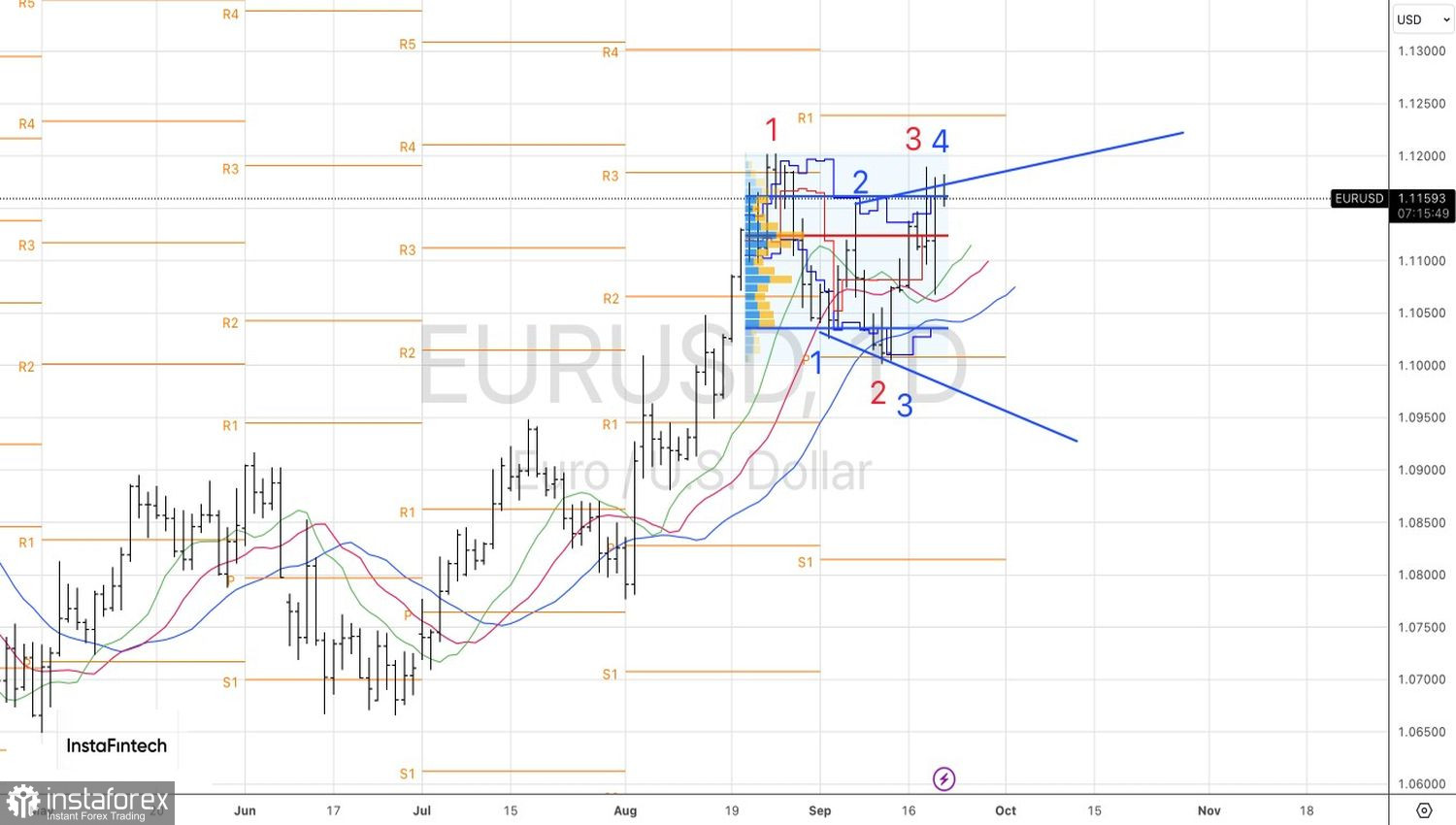

Technical Analysis

On the daily EUR/USD chart, the pair's future depends on whether the bulls can push it beyond the upper boundary of the fair value range of 1.1035–1.1160. If they fail, it would be a signal to sell the pair, targeting 1.1120 and 1.1080.