English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Times are changing, and so are perspectives. Once, a price of $2500 per ounce of gold seemed exorbitant. Now, the futures market is actively betting that the precious metal could soar to $3000. For the first time in history, bars weighing around 40 ounces are priced above $1 million, which may not be the limit. Such high demand for gold has not been seen in a long time. And not only in the East.

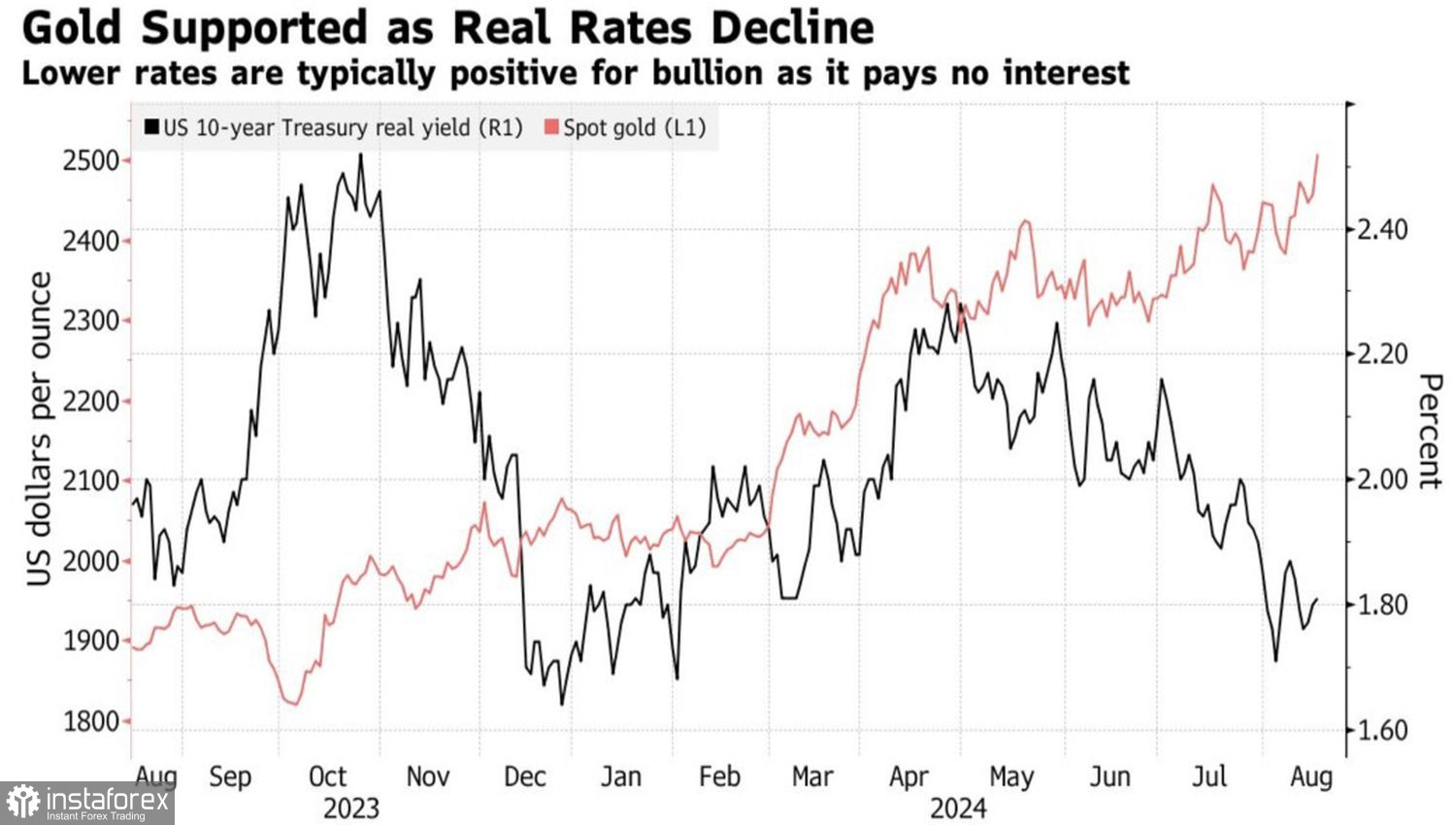

While in 2022-2023, against the backdrop of the Federal Reserve's tightening monetary policy, rising Treasury yields, and the strengthening of the U.S. dollar, XAU/USD quotes were rising due to de-dollarization, geopolitics, active central bank purchases, and increased appetite from China and India, the situation has changed in 2024-2025. Now, it is no longer Asia but North America and Europe that dictate their own rules in the precious metal market.

Gold is regaining the correlations it lost in previous years with Treasury yields and the U.S. dollar. Both bond yields and the U.S. dollar are falling due to expectations of aggressive monetary policy easing by the Federal Reserve. Derivatives forecast that in 2024, the federal funds rate will plunge by 100 basis points to 4.5%, and in 2025, it will drop another 100 basis points to 3.5%. Cycles of monetary expansion have always created a favorable environment for an XAU/USD rally.

Dynamics of Gold and U.S. Bond Yields

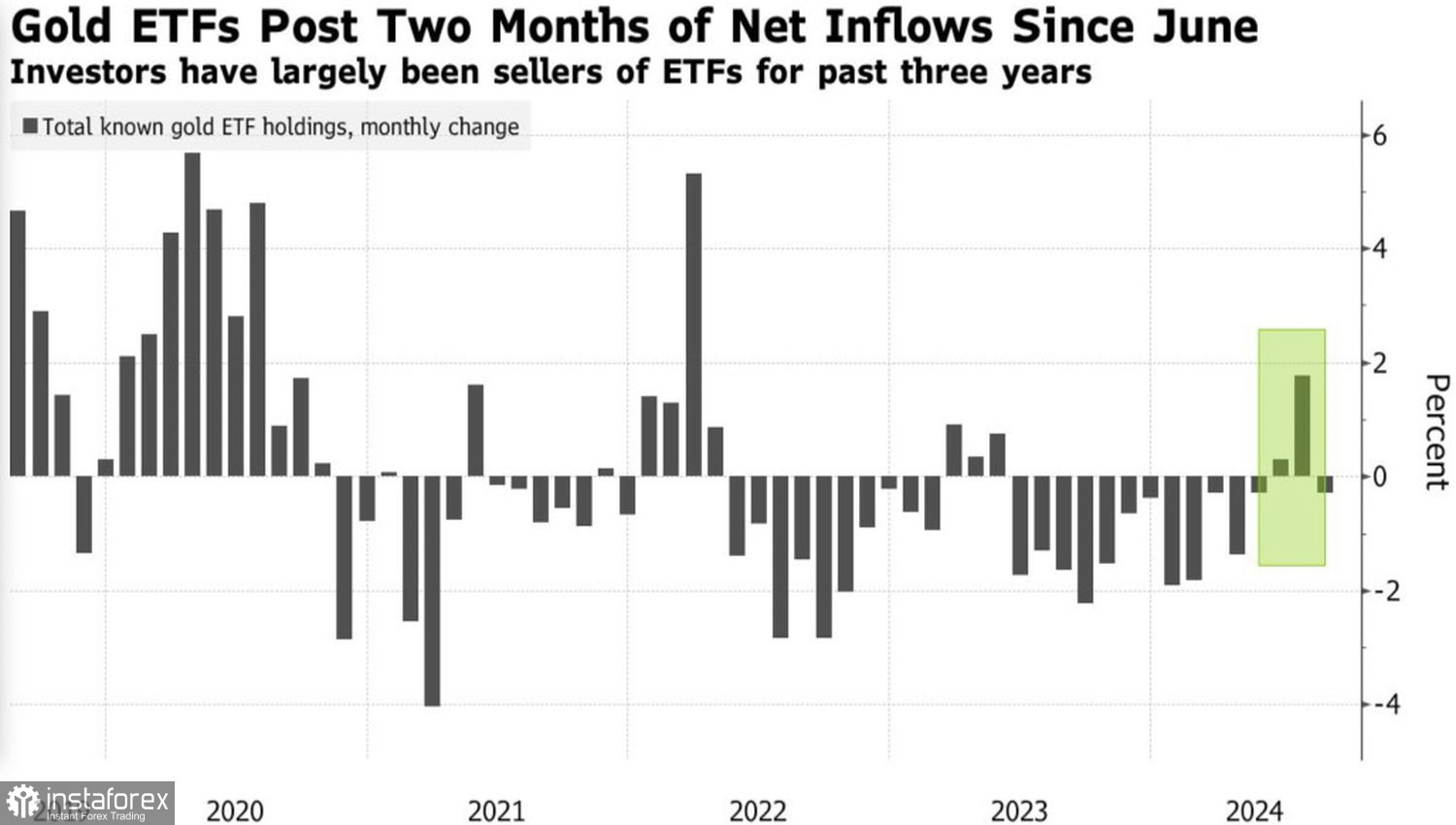

It's no surprise that speculators have increased their net long positions in precious metals to the highest levels over four years, and ETF holdings rose in June and July after months of capital outflows from specialized exchange-traded funds.

Essentially, the West has picked up the falling banner from the East. Indeed, the sharp decline in Chinese gold imports in June and July, the cessation of gold purchases by the People's Bank of China, and lower prices in Shanghai compared to London indicate that demand in Asia is starting to wane. Prices are high.

Dynamics of Specialized Gold-Focused ETFs

What problems could XAU/USD be facing? A recession in the U.S. economy? As events in early August showed, fears of a recession did indeed cause the precious metal to drop. However, this was a momentary reaction to the sharp collapse in U.S. stock indexes. Investors were pulling gold from their portfolios to meet margin requirements for stocks. In fact, a recession is favorable for XAU/USD. In such a scenario, the Fed typically cuts rates sharply, Treasury yields fall, and the U.S. dollar weakens.

Neither a hard nor a soft landing for the U.S. economy is terrible for the precious metals. The country's GDP is slowing down, its currency is weakening, and it no longer has the same advantage over other countries.

Technically, on the daily gold chart, there is a battle for the pivot level of $2515 per ounce. If it remains for the bulls, we will continue to hold and increase our long positions from $2408, targeting $2570. A local victory for the bears would provide an opportunity to buy the precious metal on a pullback to $2480 per ounce.