English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

"Buy the rumor, sell the fact!" The euro fell to its lowest level since mid-December amid expectations of weak statistics on European business activity and a correction in U.S. stock indices. In reality, the S&P 500 rewrote its historical high for the third time, and the manufacturing purchasing managers' indices in the currency bloc in January provided a pleasant surprise. As a result, EUR/USD sellers began to lock in profits, and the main currency pair soared above 1.09.

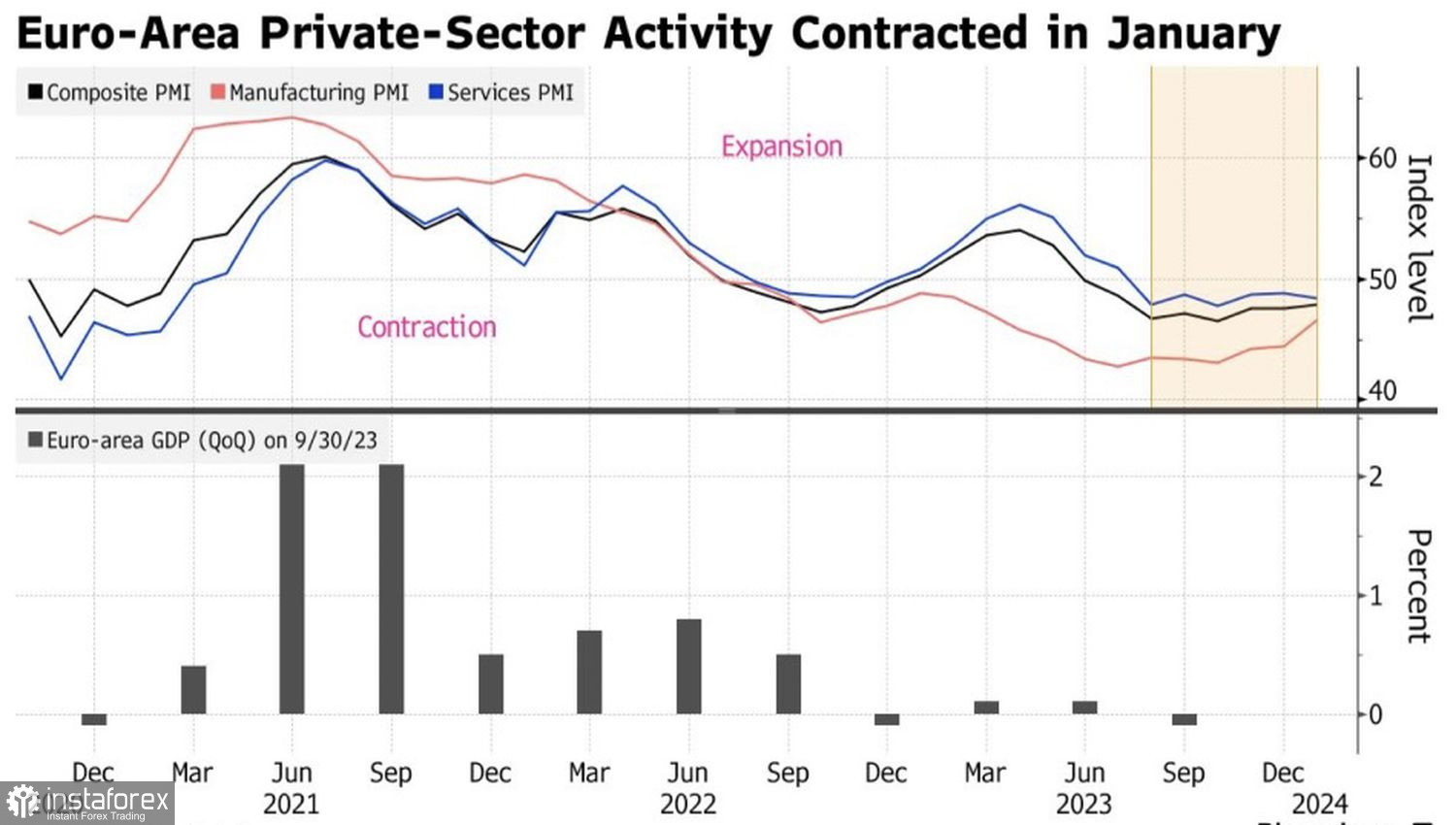

The Eurozone's composite PMI in January rose from 47.6 to 47.9, coming very close to the Bloomberg experts' consensus forecast of 48. Business activity in the manufacturing sector significantly exceeded estimates, while the service sector was somewhat disappointing. The indicators being below the critical 50-point mark signals a recession. However, according to Bloomberg Economics, such a data set will allow the ECB to hold rates. And not just in January, but over the next few months. June remains the most likely time for the start of monetary expansion.

Dynamics of European business activity and GDP

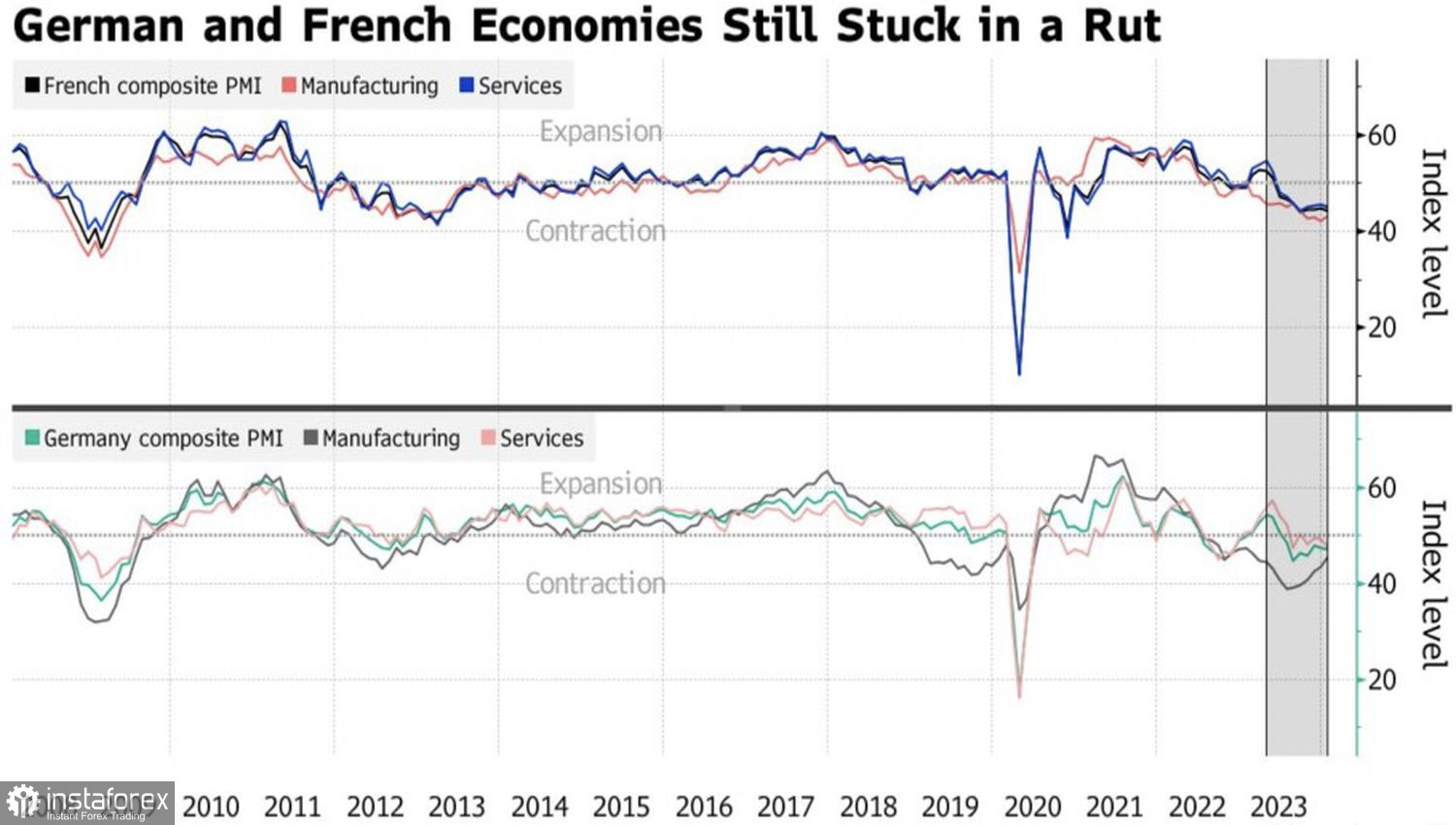

The two leading economies of the currency bloc, Germany and France, pleased with manufacturing purchasing managers' indices and disappointed in the service sector. This is a general trend indicating that the economic recovery after the pandemic has completely ended. As if the tense situation in the Red Sea didn't create new problems. Supply chain disruptions could cause inflation to rise, which the ECB certainly does not need.

European Central Bank President Christine Lagarde is expected to state that the ECB is not ready to discuss rate cuts. According to UniCredit, only a significant deflationary shock will force it to take the first step before June.

Dynamics of business activity in Germany and France

Both the "hawks" and the "doves" of the ECB have their own arguments. Proponents of maintaining the deposit rate at the current level of 4% argue that due to the conflict in the Middle East, a strong labor market in the Eurozone, and improved financial conditions, inflation will be able to stabilize at higher levels. Their opponents, on the contrary, believe that the weakness of the currency bloc's economy, the fall in wholesale gas prices to a two-year low, and declining producer prices will push CPI lower and lower. Who is right and who is to blame will be judged by the data. For now, the best decision for the ECB is a pause.

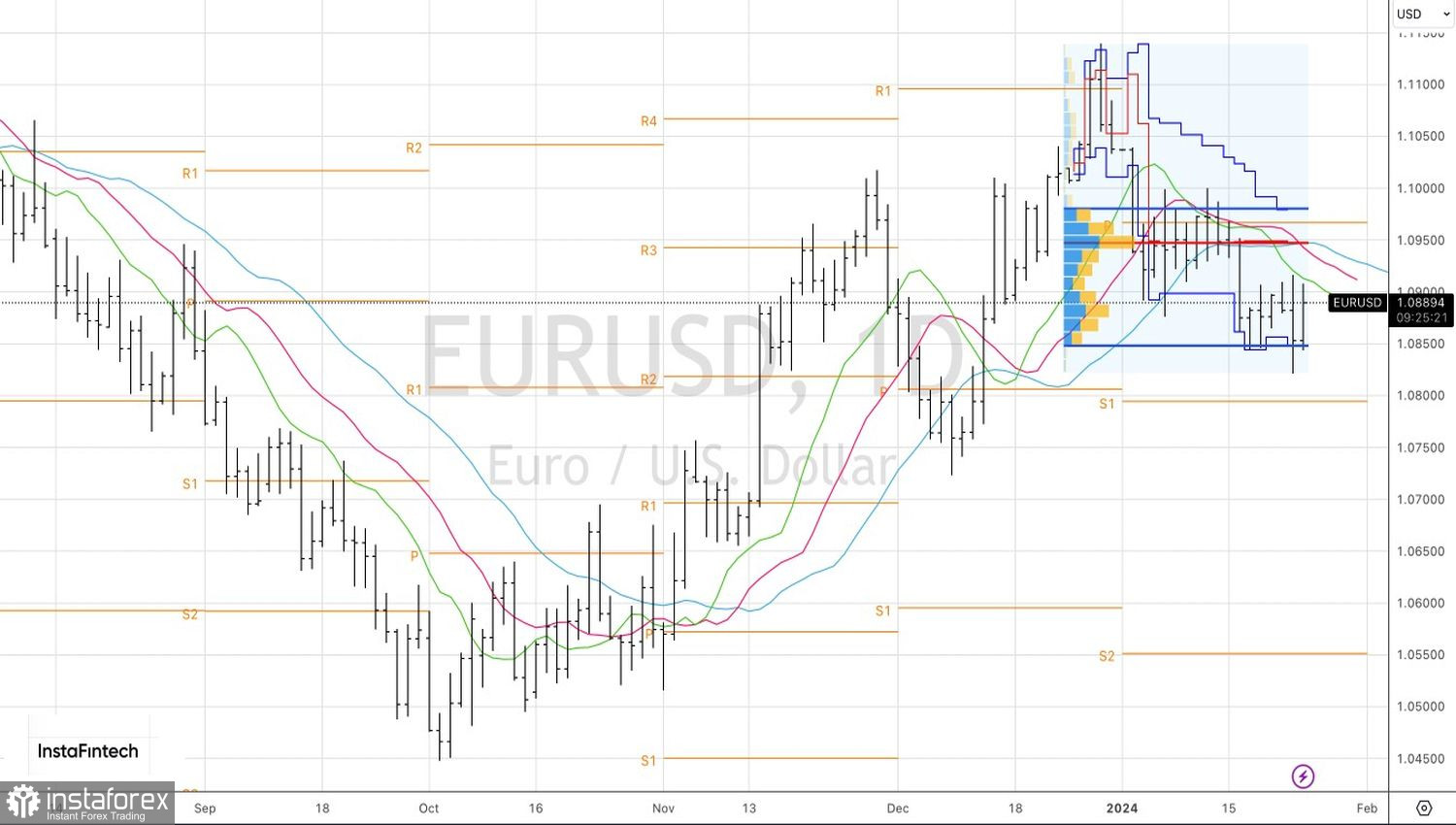

It's not only necessary for central banks but also for EUR/USD. The main currency pair has been trading in a narrow range of 1.085–1.100 for several weeks now, and neither strong U.S. employment, inflation, and retail sales statistics nor S&P 500 records could drive it out of there.

Technically, on the daily chart, EUR/USD is returning to the range of fair value 1.085–1.098. The inability of the bears to drive it out of there is a sign of their weakness. At the same time, a rebound from the resistances at 1.095, 1.097, and 1.098 will be a reason for selling.