English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Today, futures on US stock indices found solid ground and opened with growth. Discussions about the world's leading central banks starting a significant campaign to reduce interest rates next year continue to fuel demand for risky assets, but not all are equally fortunate. The S&P 500 futures rose by 0.2%, while the high-tech NASDAQ added 0.3%. The industrial Dow Jones increased by only 0.1%. Treasury bond yields remained unchanged at around 4.2%. The Stoxx 600 index traded close to its four-month high after a European Central Bank official indicated sufficient progress in fighting inflation, suggesting that a shift back to a softer policy next year could be considered.

Meanwhile, traders are debating the sustainability of the stock market rally, which is based on hopes for a sharp policy reversal. Some experts note that the recent dovish comments from central bank leaders can be interpreted ambiguously. What is more, it is not certain that policymakers are ready to adopt a softer stance now. Therefore, it is unsurprising that market overbought conditions, coupled with signs that the Federal Reserve may not reduce interest rates as quickly as expected, have triggered a minor bearish correction.

Most likely, a clearer assessment of whether central banks will continue to consider a soft policy next year will depend on incoming data, particularly labor market statistics. Today, the ADP report will be released, and on Friday, we await more crucial statistics on non-farm employment in the US.

As mentioned earlier, in Europe, policymakers' actions have already triggered a bond rally. The more hawkish European Central Bank officials stated yesterday that inflation was showing the expected slowdown. Isabelle Schnabel, who was among the last to suggest it was too early to rule out further rate hikes, added a note of caution, stating that the ECB should be careful in its statements about what to expect next.

In the futures market, six ECB rate cuts by a quarter point in 2024 are now fully priced in. The central bank may cut the key rate by 150 basis points to 2.5%. There is also an almost 90% probability that the easing cycle will begin in the first quarter of next year. This scenario was hardly considered just three weeks ago.

Against this backdrop, US government bonds are in high demand as investors prepare for a potential downturn in the economic resilience of the US, which has made 2023 a challenging year.

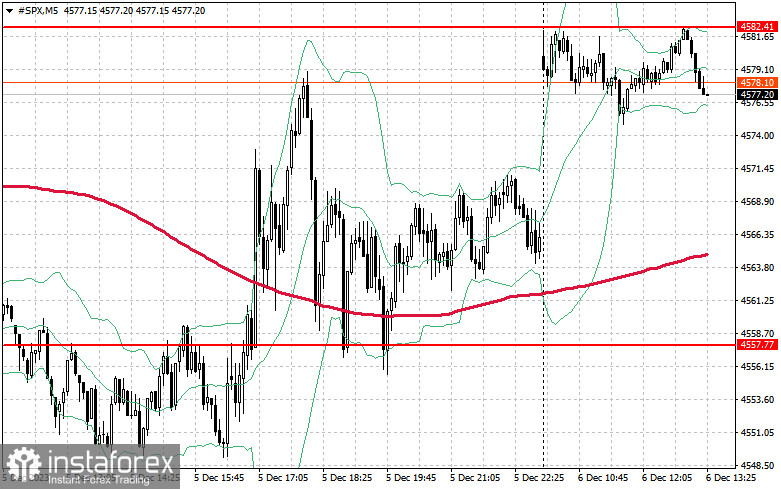

As for the technical picture of the S&P 500, demand for the index rebounded. The main task for buyers today is to defend the $4,557 level and regain control at $4,582. This will help restore the upward trend and open the possibility of a surge to a new level at $4,609. Equally important for bulls will be control over $4,637, which may strengthen buyers' positions. In the event of a downward movement caused by a reduced risk appetite after weak US data, buyers should become active around $4,557. A breakthrough will quickly push the trading instrument back to $4,553 and pave the way to $4,515.