English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Greed is to blame for everything. Investors never anticipated that interest rates in 2022-2023 would rise so quickly and to such heights. Now, no one wants to be late for the moment when they start to decline. As a result, the markets have repeatedly stepped on the same rake: expecting a dovish pivot from the Federal Reserve, but it never came. In the end, after a strong last year and the current one, the U.S. dollar becomes the main favorite. However, investors repeatedly try to express their disgust for it.

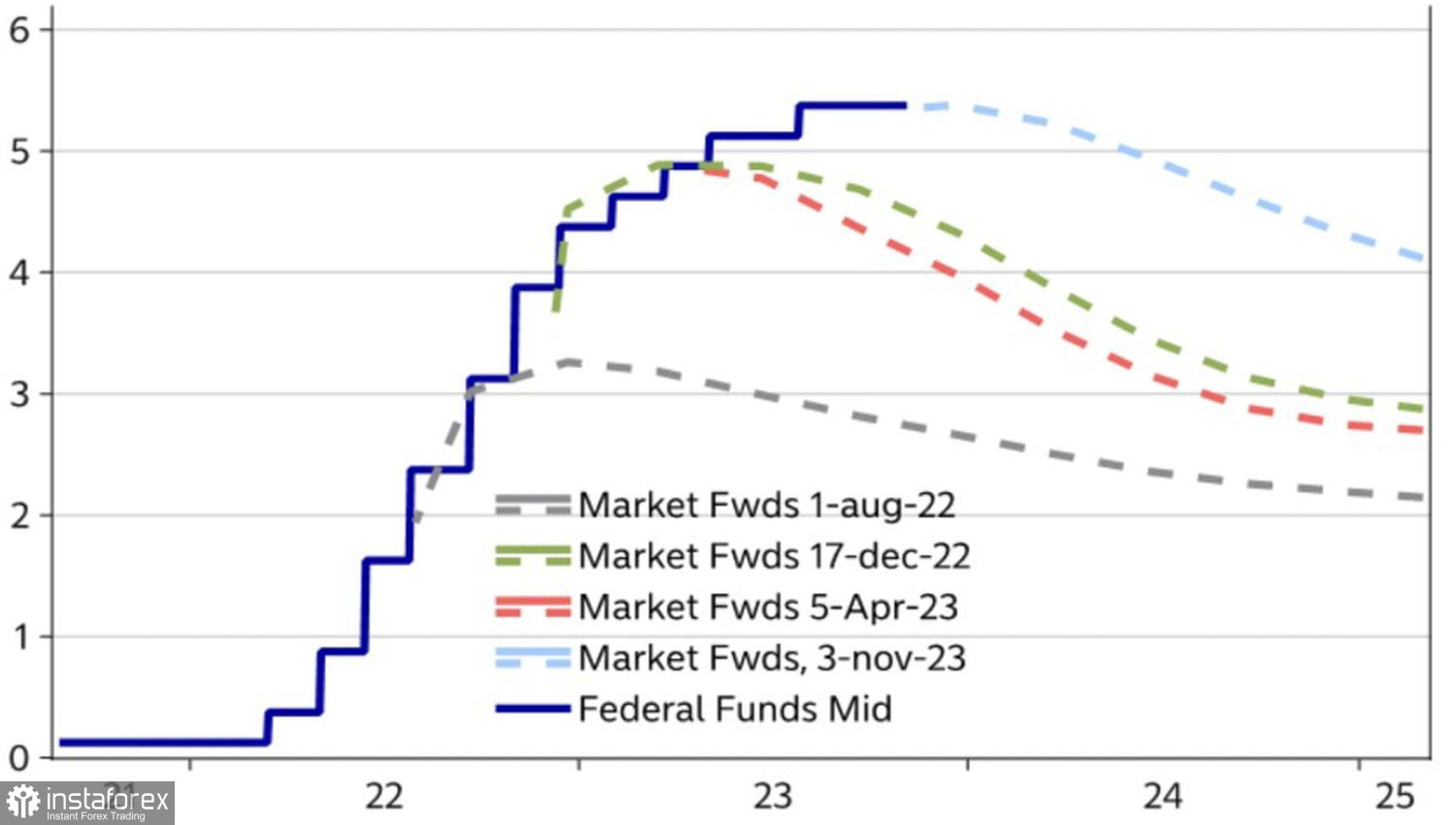

According to the latest Bank of America survey, major banks and investment companies intend to reduce the overweight of the U.S. currency in portfolios at the fastest pace since the beginning of 2021. The main reasons cited are the excessively high share of the dollar, the vulnerability of positions to a shift in the Fed's worldview, and, finally, market expectations of an 80 bps interest rate cut in 2023. This is more than forecast for the ECB deposit rate and the Bank of England repo rate. The question is, will the Fed go for it?

Dynamics of Market Expectations for the Fed Rate

Based on Jerome Powell's recent remarks, it's unlikely. The Fed chair spoke a lot about the central bank's previous, sad experience when, in the 1970s, the Fed believed in victory over inflation, and it unexpectedly rose from the ashes. The resumption of the fight resulted in a double recession for the U.S. economy. Now, the regulator will undoubtedly raise borrowing costs again if it deems it necessary. Such rhetoric is hardly indicative of the end of the tightening cycle of monetary policy. No wonder it has revived the "bears" on EUR/USD.

Thus, if the Fed is not going to step on old rakes, the markets regularly do so in the hope of an early entry into a very successful deal that will subsequently cover all previous losses. The problem is that getting tired of going against the Federal Reserve may happen just when it really starts to ease monetary policy. That's life!

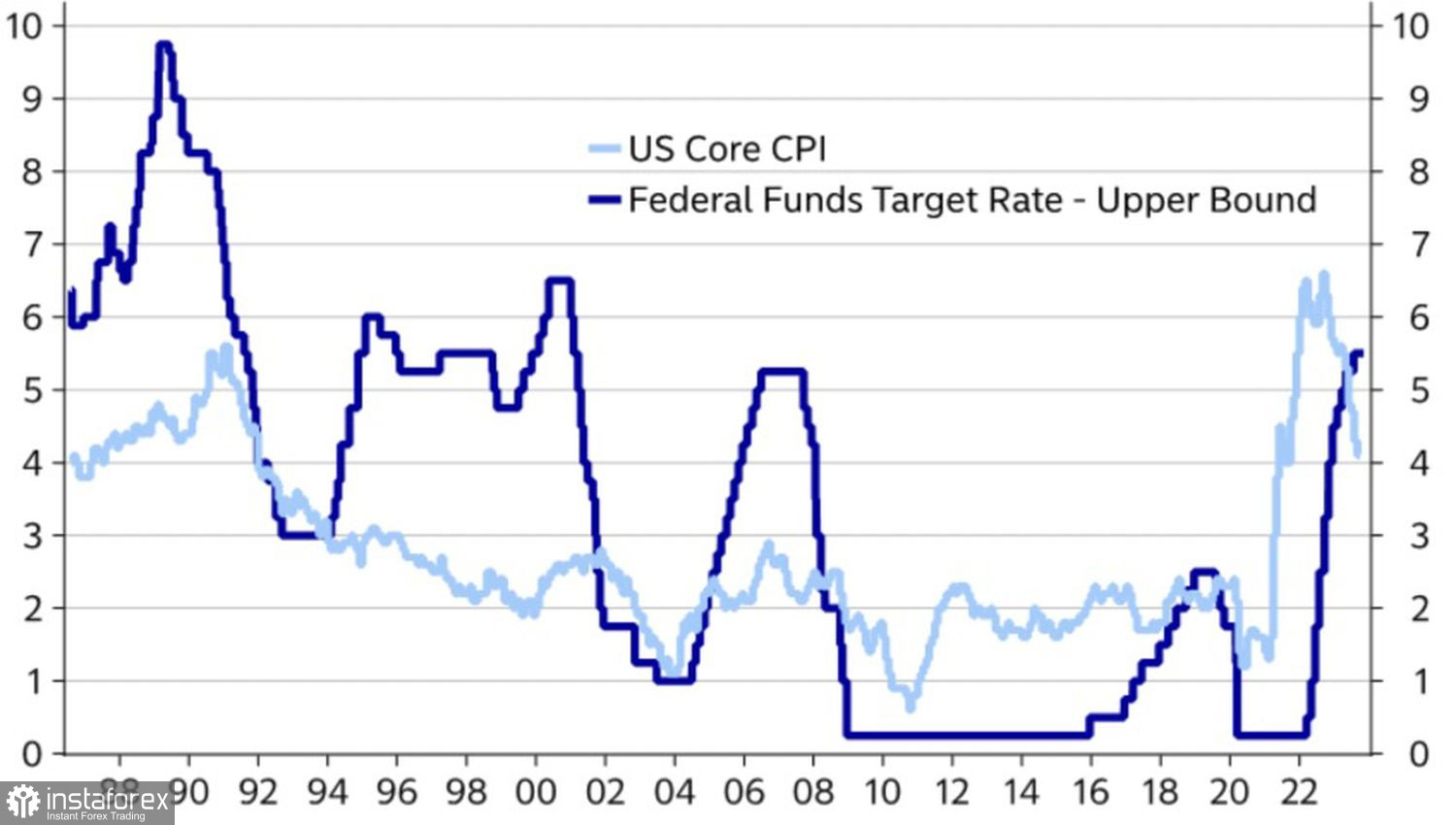

Dynamics of U.S. Inflation and Fed Rates

In fact, if you temper your own greed a bit, it's easy to understand a simple truth. Yes, the bar for raising the federal funds rate is high, but even higher for lowering it. The U.S. economy is solid. Treasury yields have not been this high for the past 16 years. Stock indices look attractive. The influx of capital into U.S. assets strengthens the positions of the "bears" on EUR/USD.

On the other hand, the final verdict for the pair will be rendered by inflation statistics for October. According to Bloomberg, consumer prices and the core indicator should grow by 0.2% m/m for 4-6 months for the Fed to finally start talking about a rate cut.

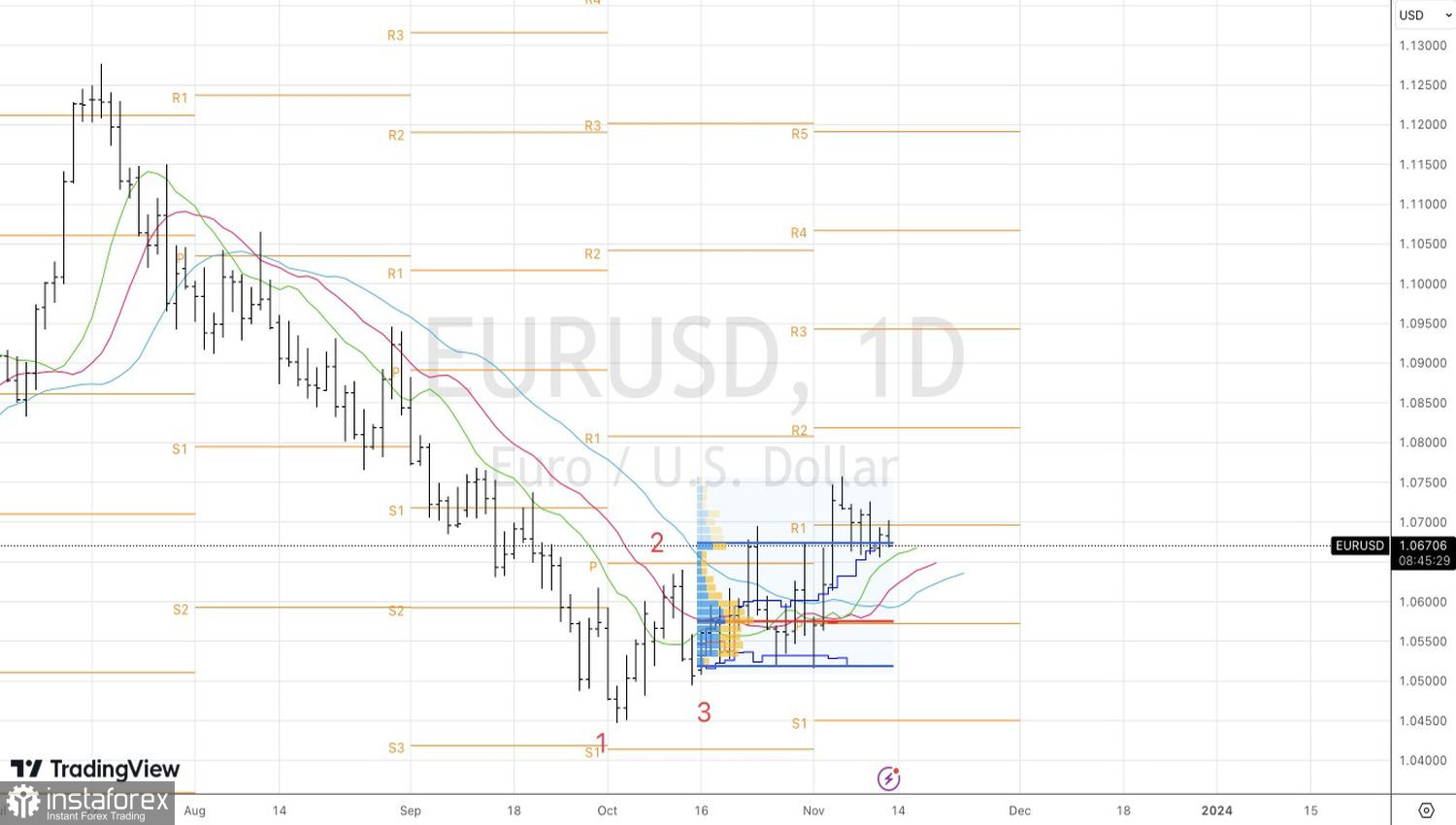

Technically, on the daily chart of EUR/USD, there is a short-term consolidation after the explosive rally. Only successful tests of resistance at 1.07 and 1.072 will allow the pair to rise. On the contrary, breaking through supports at 1.067 and 1.0645 will be the catalyst for its decline.