English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

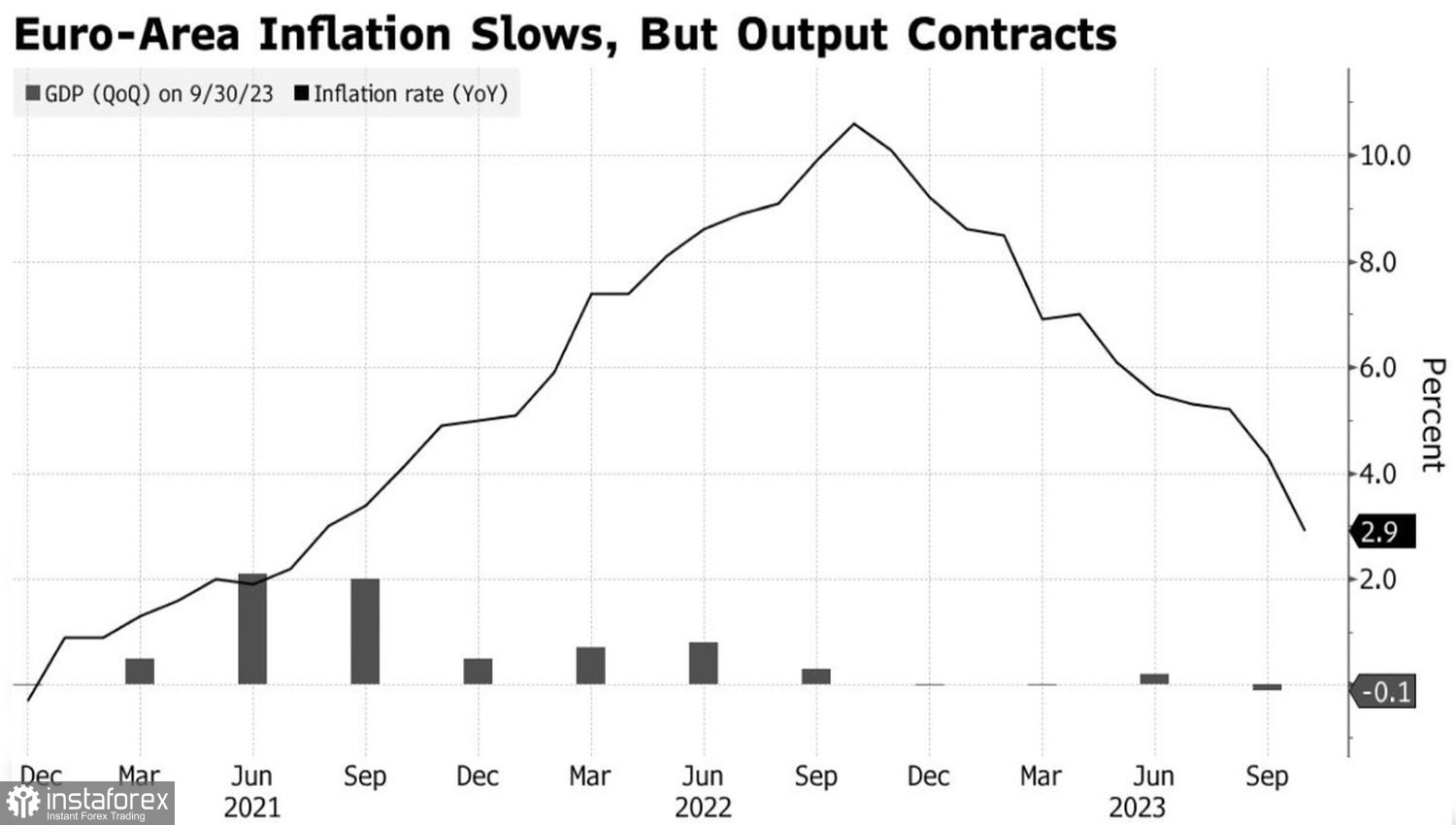

The "bulls" on EUR/USD are not bothered by the eurozone GDP contracting by 0.1% in the third quarter or the slowing inflation of 2.9% in October, which essentially marks the end of the ECB's monetary policy tightening cycle. On paper, this data supports the idea of a dovish ECB pivot in the first half of 2024, which should drive euro enthusiasts away. However, theory without practice is dead. In the real market, the major currency pair jumped to 1.065.

While a rally in EUR/USD on stronger data from the German economy might have some explanation, the strengthening of the pair on disappointing statistics for the currency bloc seems paradoxical. Perhaps the scenario of a GDP contraction and the CPI falling below 3% was already priced into the pair's quotes. As a result, once again, the "sell on rumors, buy on facts" principle has played out.

Dynamics of European inflation and GDP

I have a different opinion. There were a lot of sellers of EUR/USD in the forex market. To close speculative shorts ahead of the FOMC meeting and the release of U.S. labor market data, which is likely to have negative consequences for the dollar, counterparts were needed. When everyone is selling, there's a great opportunity to buy, and the "bears" on the major currency pair took advantage of it. As a result, the euro jumped to $1.065 and is awaiting the verdict from the Fed and U.S. employment data.

Investors are seriously concerned that the Federal Reserve will start putting pressure on U.S. Treasury yields. Its representatives have already taken up the mantra that the debt market is doing the central bank's job. This rhetoric has had a significant effect: the connection between bond yields and the U.S. dollar that was so evident in August and September has been disrupted. The U.S. Dollar Index is no longer receiving the same support from the bond market as it did in August-September.

The Fed likes the dynamics of inflation, but tight financial conditions can put a spoke in the wheel of the soft landing idea. At the same time, the central bank needs to explain its mistakes in previous forecasts. To achieve them, a contraction in GDP by 0.7% in the fourth quarter and an acceleration of PCE are required. Most likely, neither will happen.

As for employment, the surge in September could be the last. Strikes in the auto industry and other factors may slow the indicator down to below the Bloomberg estimate of 170,000. Signs of a cooling labor market and economy will bring back the topic of the Fed's dovish pivot in 2024. Thus, the clear negative impact on EUR/USD "bears" from two key events of the week makes them prematurely unwind their shorts. Weak data for the eurozone serves as the perfect backdrop for this.

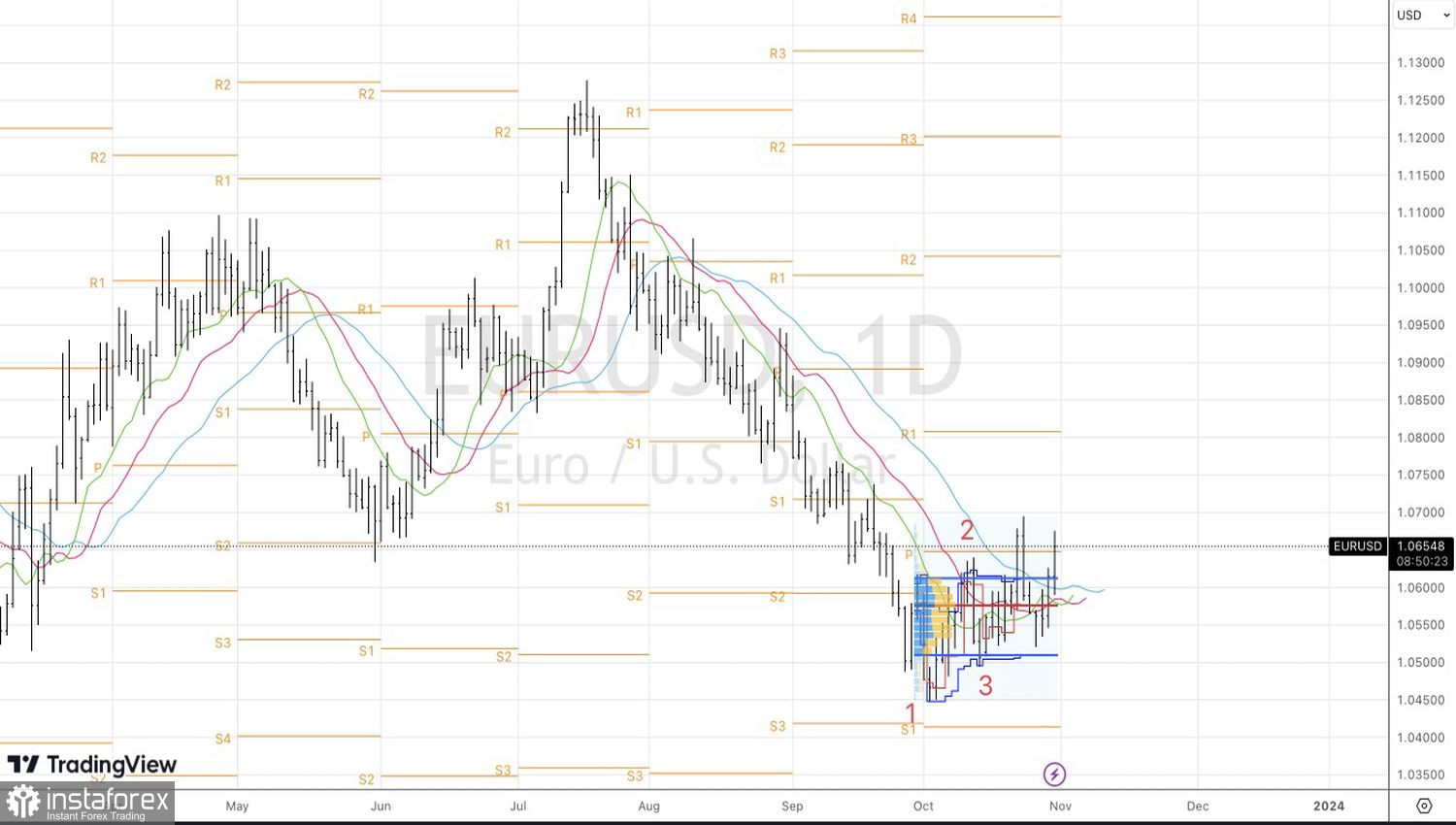

Technically, on the EUR/USD daily chart, the pair is testing the pivot level at 1.065. If it fails, it will create a 1-2-3 pattern, which implies a drop in the pair to the lower boundary of the trading range at 1.05-1.07. Conversely, a breakout of resistance will allow the euro to advance to $1.069 and $1.0715, where it should be sold on the rebound.