English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

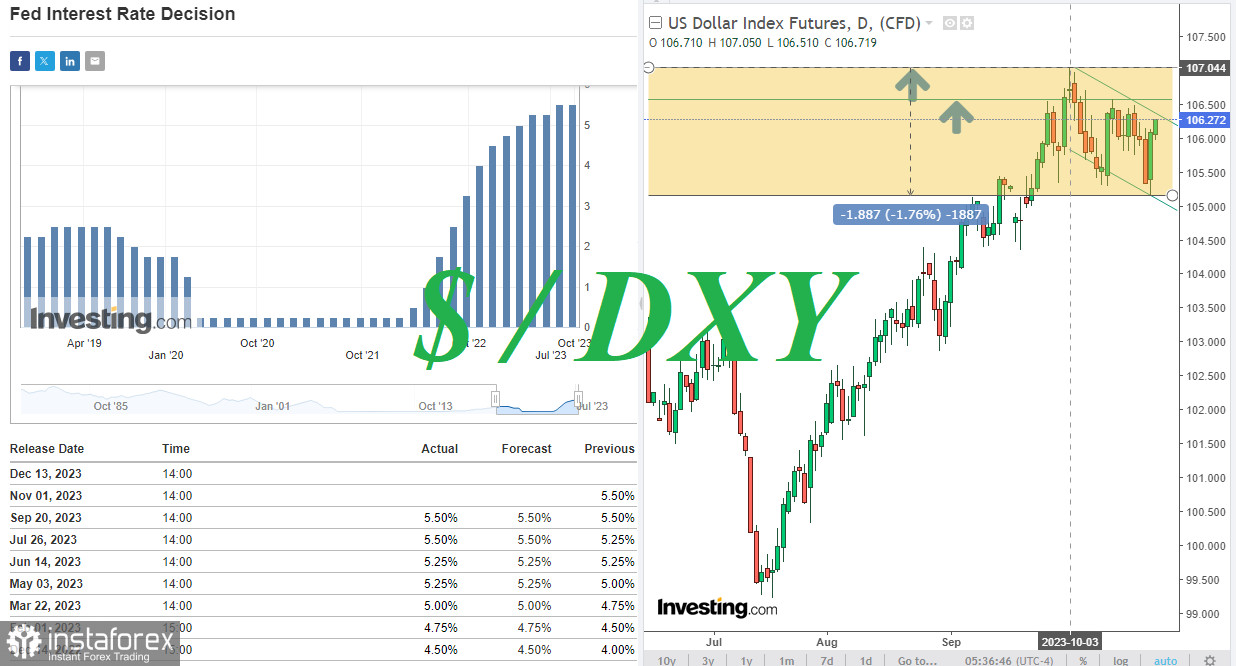

The rise of the U.S. dollar after positive macro data received from the U.S. on Tuesday is accelerating on Wednesday. As of writing, the DXY index was trading near 106.27, 19 points higher than the previous day's closing price and 112 points above the local and over 4-week low reached during the Asian trading session on Tuesday at 105.15.

According to the data published on Tuesday, the preliminary Purchasing Managers' Index (PMI) for manufacturing in October increased to 50.0 (compared to a forecast of 49.5 and the previous 49.8), and the PMI for the services sector also increased to 50.9 from 50.1 in September, which is also better than the forecast of 49.9.

S&P Global Market Intelligence commented that expectations for a 'soft landing' of the U.S. economy would be supported by the improvements observed in October. They noted that, despite the growth of geopolitical tensions and domestic political tensions, expectations for future production had also risen, reaching the highest level in almost one and a half years.

Compared to the similar data published earlier on Tuesday for the UK and the Eurozone, American macro statistics look significantly better. In particular, the composite PMI index for the USA (from S&P Global) improved to 51.0 from 50.2 the previous month, while the similar PMI for France increased to 45.3, for Germany to 45.8, for the Eurozone to 46.5, and for the UK to 48.6.

Furthermore, the American composite PMI is above the 50-mark, which separates the growth of business activity from slowdown, unlike the European PMIs mentioned above.

In other words, the gap between the growth rates of the American economy and the European one is widening, and this is not lost on investors who prefer the dollar over its other major competitors in the currency market.

Today, volatility in the market may sharply increase again at 14:00 when the Bank of Canada's decision on interest rates will be published, followed by a press conference at 15:00 (GMT) where the head of the Bank of Canada, Tiff Macklem, will explain the bank's position and assess the current economic situation in the country and possibly the world. At 17:00, the speech by ECB President Christine Lagarde begins, and at 20:35 (GMT), the speech by Federal Reserve Chairman Jerome Powell will begin.

This is an unplanned appearance, especially in the so-called "quiet week" before the next week's Federal Reserve meeting.

Therefore, it's not excluded that Powell may make unexpected statements today that could trigger sharp movements in the dollar quotes and its DXY index.

In general, market participants expect "bullish" signals from Powell regarding the dollar and the near-term prospects of the Federal Reserve's monetary policy. However, if Powell cannot convince the markets of the strong commitment of the Federal Reserve leadership to a tough policy and limits himself to statements that the current policy parameters will remain unchanged, and the interest rate will not be raised further, the dollar may react with a sharp decline.

From a technical point of view, the dollar index (CFD #USDX in the MT4 terminal) is trading in the stable bull market zone, with medium-term support above the key level of 104.00, and long-term support above the key levels of 101.40, 100.30, and 100.00.

In this situation, long positions remain preferable. The nearest growth targets will be local resistance levels at 106.75, 107.00, 107.32, 107.80, and 108.00.

Support levels: 106.15, 106.00, 105.70, 105.50, 105.20, 105.00, 104.00, 103.00, 102.00, 101.40, 101.00, 100.30, 100.00

Resistance levels: 106.75, 107.00, 107.32, 107.80, 108.00, 109.00, 109.25