English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Sell the rumor, buy the fact. Expectations of a slowdown in German inflation from 6.1% to 4.6% were one of the drivers behind the decline of EUR/USD. However, the actual data turned out to be even worse: consumer prices slowed down to 4.5% in September. Nevertheless, closing short positions against the backdrop of important statistics from Germany prompted a rebound in the euro. Has the main currency pair found its bottom?

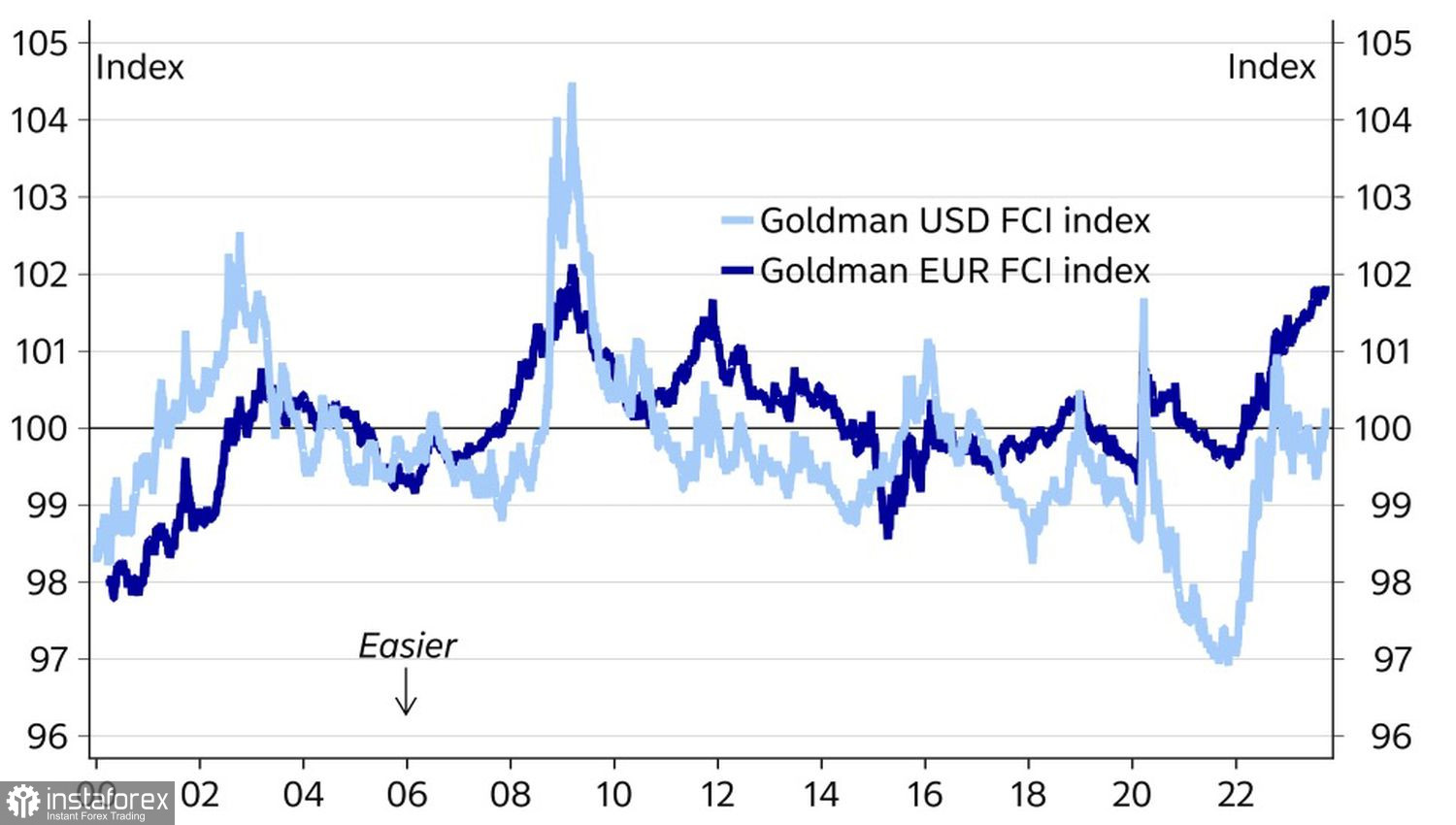

In reality, the market logic is quite simple: the lower European inflation goes, the less likely the ECB will continue its cycle of tightening monetary policy. This makes sense; however, investors are increasingly thinking that the current cycle of monetary restriction in Frankfurt has affected the eurozone economy much faster than the actions of the Federal Reserve. This is evidenced by the dynamics of financial conditions, which are significantly tighter in Europe than in the United States.

Dynamics of Financial Conditions in the U.S. and Eurozone

Thus, the 10 acts of monetary restriction by the ECB have proven more effective than the larger number of steps taken by the Federal Reserve. They have cooled down the currency bloc's economy and reduced domestic demand. The European Central Bank can expect a rapid slowdown in CPI growth. The cycle of tightening monetary policy is complete. The question is whether the economy can withstand it.

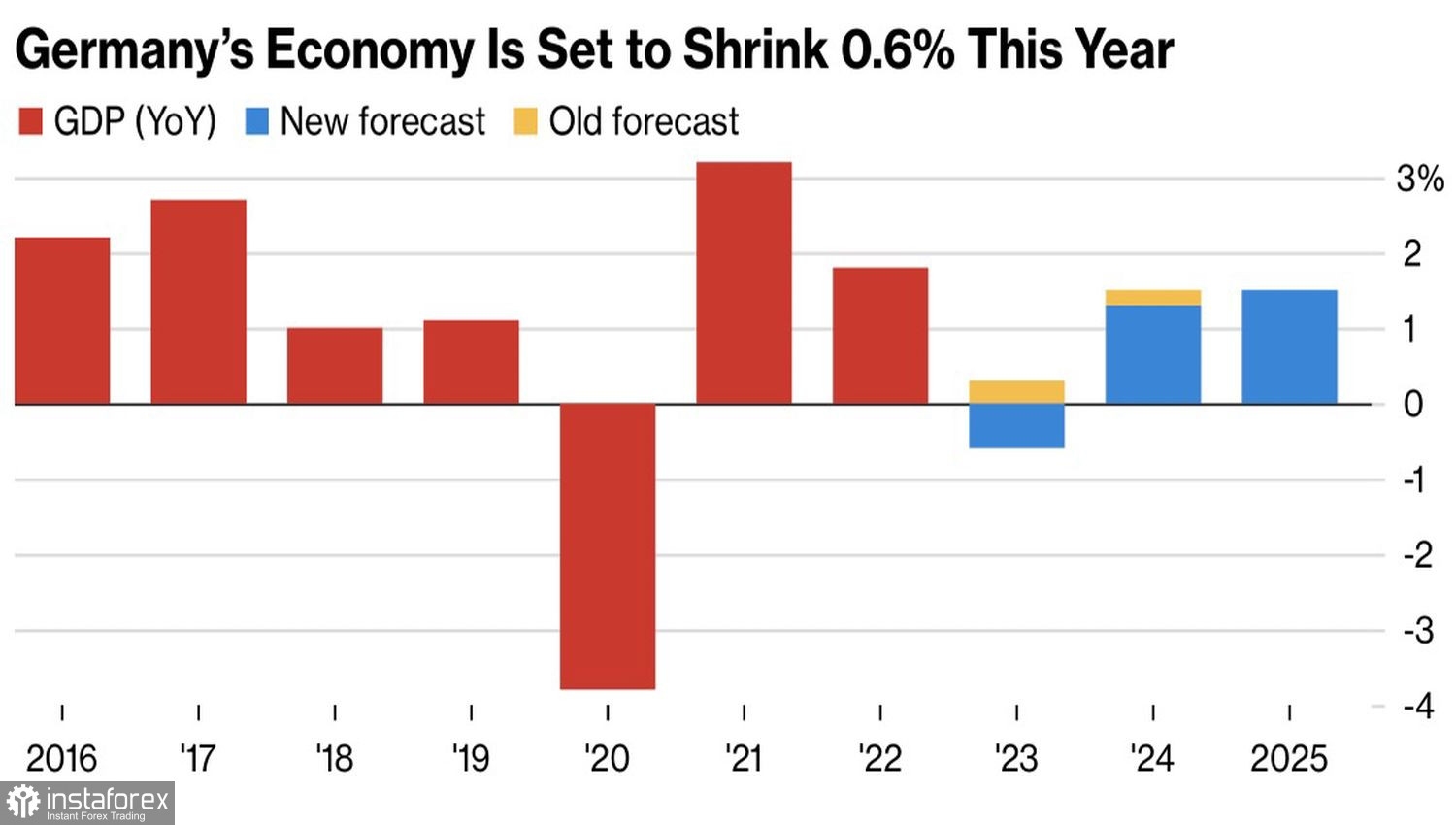

Forecasts from five government consulting institutions indicate that in 2023, Germany's GDP will contract for the first time since the pandemic, with a decline of 0.6%, although the previous estimate was +0.3%. The prospects within the country appear bleaker than the forecasts of the IMF and the European Commission.

Dynamics and Forecasts for German GDP

The main conclusion is that the ECB has cooled both inflation and the economy. It will certainly achieve a reduction in the consumer price index to the target, but a recession may occur more quickly. For Forex, it is important to note that the eurozone is more sensitive to monetary restriction than the United States. The U.S. GDP will not slow down as quickly as its European counterpart, even with the potential government shutdown, resumption of student loan payments, and strikes in the automotive industry. As a result, Treasury bond yields may continue to rally, which will renew investor interest in selling EUR/USD.

According to ING's modeling, if 10-year yields rise to 5%, the main currency pair will drop to 1.02. This corresponds to its movement from 1.1 to 1.06 amid a rally in Treasury yields from 4% to 4.5%. ING considers this scenario quite likely given the Fed's intention to keep borrowing costs elevated at 5.5% for a long time and potentially raise them further if necessary.

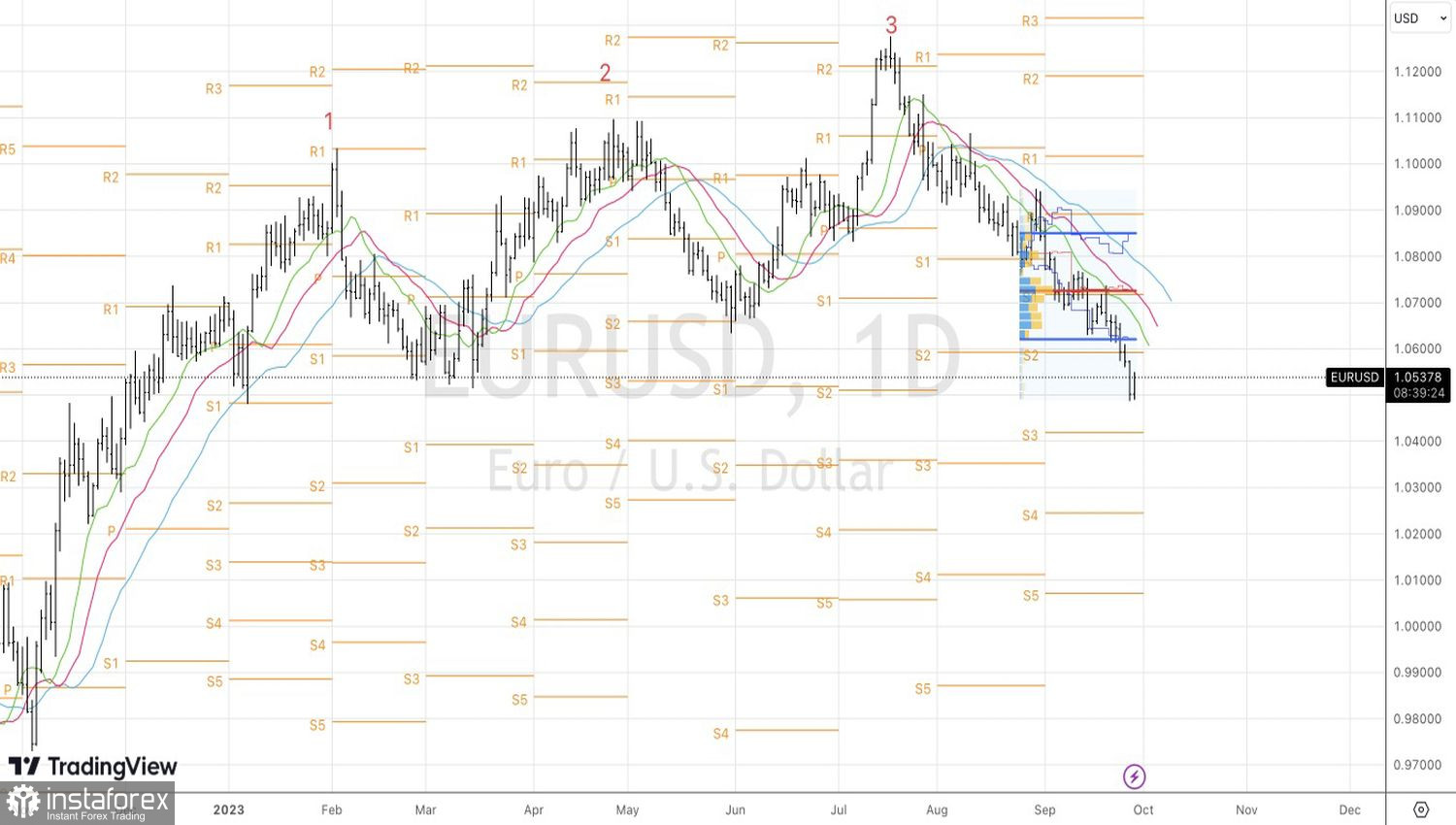

Technically, on the daily chart of EUR/USD, after reaching the short target at 1.051, a predictable rebound occurred. The important pivot level did not give in on the first attempt. Nevertheless, the trend remains bearish. In such conditions, it makes sense to catch rebounds from important resistances at 1.0585, 1.062, and 1.0655 for selling.