English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

This week, the US dollar is trying to strengthen, and its movement is closely linked to expectations from the US Federal Reserve. So, what factors are influencing the DXY, and what decisions from the Fed could affect its further movement?

Last week, the US dollar failed to grow amid negative labor market news and lower-than-expected economic growth.

However, by Friday evening, the reserve currency managed to almost fully regain its position. The reason for the US dollar sell-off was the increase in the manufacturing PMI to 47.6 from 46.4.

Despite the unfavorable US data, the gap between US and European economic growth remains significant, and demand for the US currency persists. According to the international SWIFT payment system, the share of the US dollar in international settlements has grown to 46.5%, while the euro's share has decreased to 24.4%, reaching an all-time low.

Apparently, even a slight positive information flow from the US can exacerbate the imbalance between the euro and the dollar.

Although the number of non-farm workers slightly exceeded forecasts in August, revised statistical data indicated much less impressive employment growth in July and June compared to previous information.

The increase in wages has also stalled, reinforcing the market's hopes that the Federal Reserve may refrain from raising interest rates this month.

The likelihood of a rate hike in September sharply dropped to about 7% from 20% last week after employment data was published.

The initial market reaction was clear, as the US dollar and yields decreased, but this drop was temporary.

Once the emotions settled, the yield of long-term Treasury bonds sharply rose, leading to the strengthening of the US dollar.

It is hard to say what caused it, but the rise in oil prices and more favorable ISM survey results in the manufacturing sector certainly played an important role.

The prospects for the dollar appear increasingly promising. The economy is already demonstrating greater resilience than the Eurozone's economy, and the recent rise in energy prices could further amplify this difference, affecting the euro/dollar pair in terms of economic growth and external trade flows.

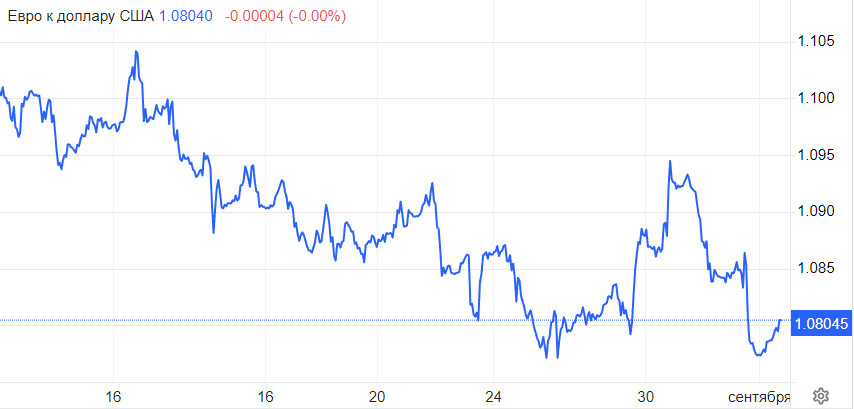

The euro/dollar pair may continue to follow a bearish scenario in the near future, prompting us to anticipate further declines toward 1.0700. Meanwhile, a rise above 1.0785 may lead to a corrective upward movement toward 1.0845.

The only missing component for a full-fledged US dollar rally might be a period of risk aversion in the stock markets.

Meanwhile, in China, a series of targeted stimuli seem to be yielding results and restoring investor confidence.

Last week, Beijing enhanced support for domestic households and the construction industry by providing tax benefits for child and educational expenses and easing housing purchase restrictions.

Despite the current seemingly limited scope of economic stimulus measures, the continuous expansion of these measures is raising hopes that China's economic activity will soon hit bottom.

This cautious optimism also had an impact on commodity markets last week, with industrial metals and energy prices rising sharply.

Oil prices reached their highest level since November as the expectation of increased demand shifted the market balance, where major producers had been curtailing supplies for some time.

Similarly, stocks in Hong Kong surged, and currencies linked to China, such as the Australian dollar, demonstrated some growth as a result of trade.

The exception was the Canadian dollar, which could not capitalize on its usual correlation with oil prices and plummeted after data was published. Figures indicated an unexpected contraction in the economy in the second quarter and shattered hopes for a Bank of Canada interest rate hike.

Analysis of next week's events

This week, there is not much news from the US, and finding positives among them is not so straightforward. Industrial orders are expected to decrease by 2.5%, and the trade balance deficit is projected to rise to $68 billion.

The ISM Business Activity Index in the services sector is also anticipated to slightly decline, though it is possible that business activity in this sector could exceed expectations.

Regarding weekly data on unemployment benefit claims, the forecast remains within average values. While these data may not inspire great optimism, the absence of bad news can be seen as good news.

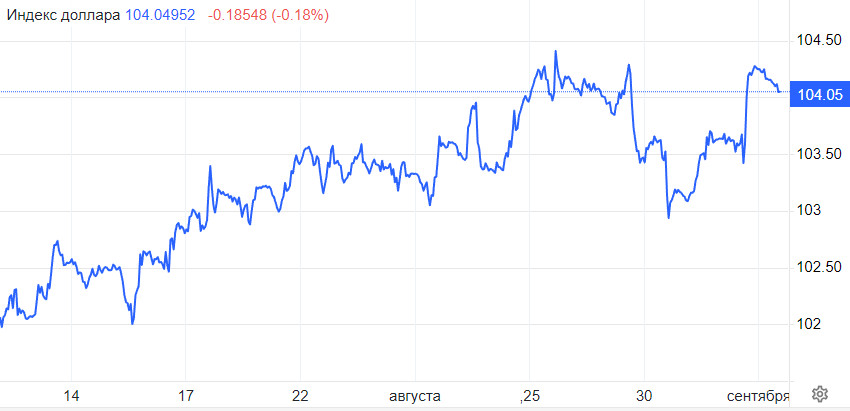

From a technical standpoint, the situation is uncertain right now. The US dollar index approached a resistance level on Friday and stopped. The dollar's value could reach 104.70 without strong positive news support, but for further growth, a significant stimulus is likely needed.

In the second half of the week, several Fed officials will speak at the annual fintech conference in Philadelphia, where they might outline plans for the upcoming session.

In the absence of other significant news, it is their stance that can assess the likelihood of future interest rate hikes, which is currently quite low.

If the odds of tightening do increase, it can be assumed that the US dollar index may continue to rise and reach the range of 105.40–105.60. Otherwise, a downward correction to 103.70 is possible.