English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The US labor market report came out weaker than expected. Only 187,000 new jobs were created (forecast was 200,000), and the previous two months were revised lower by 49,000 jobs, resulting in a net gain of only 138,000 jobs, well below the average values seen earlier this year.

The average hourly earnings increased by 4.4% (forecast was 4.2%), remaining at the same level as in June. This indicates that the market continues to expect higher inflation. However, it is premature to conclude that the chances of another interest rate hike have increased for the Federal Reserve. The US central bank considers that wage growth is slowing down more slowly than inflation and they may need to wait a bit longer to see a natural slowdown in this indicator. The futures market for Fed rate hikes, according to CME data, remained practically unchanged, indicating that the market does not see the threat of another rate hike at the moment.

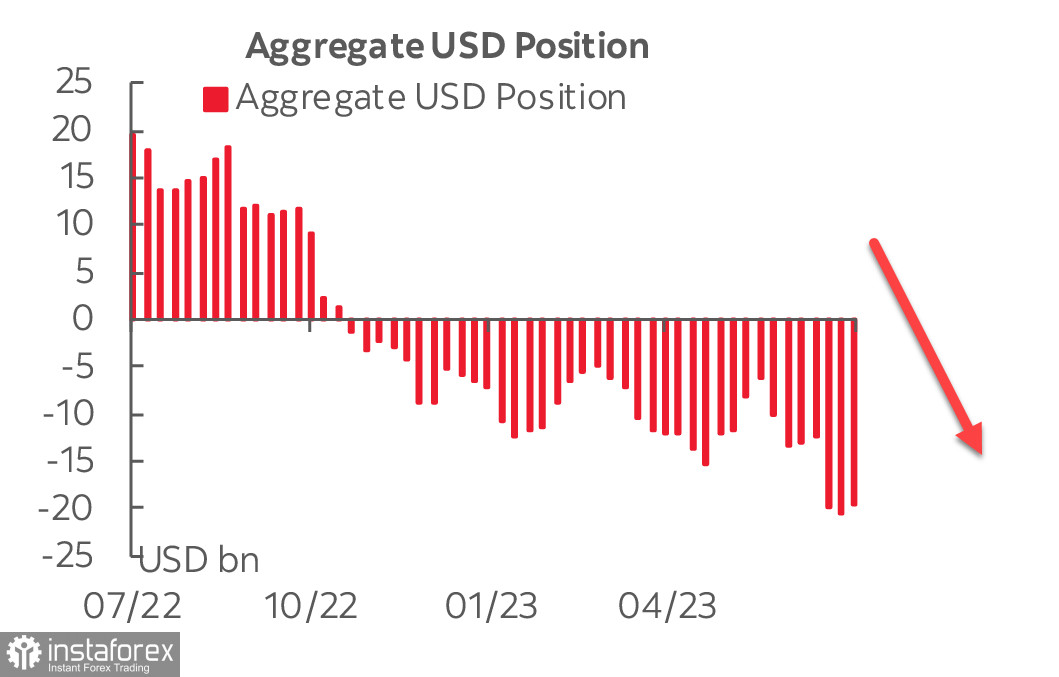

The CFTC report showed that investors are not rushing to change their priorities in the futures market. The net short position on the US dollar decreased by 1.4 billion to -19.2 billion during the reporting week, primarily due to a reduction in the volume of long positions on the euro and the pound. In other words, the slight improvement in the dollar's positions is not due to the strength of the dollar itself, but rather to lower expectations for the two main European currencies, as changes in other G10 currencies are minimal or almost non-existent.

The fact that the US economy is slowing down is evident, with the industrial sector already in a recession, and the service sector experiencing a slowdown in growth. However, the depth of the upcoming downturn is still uncertain. Investors are not in a rush to leave US assets; the debt market saw a slight increase after the nonfarm payroll report, and the stock market decline was insignificant. The dollar remains stable, and at present, there are no apparent reasons for it to become weaker.

EUR/USD

Sentix's index for the eurozone rose to -18.9 points in August from -22.5 in July, indicating a slowdown in the index decline. However, the assessment of the current situation remains negative at -20.5 points, but expectations have increased to -17.3 points, up by 7.3 points.

In Germany, the situation is noticeably more challenging - the overall index has been declining for the fourth consecutive month and is now at -30.7 points. The current situation worsened by 7.3 points. On Tuesday, the inflation report for Germany will be published, and it is expected that inflation will remain at the same level as a month ago, indicating that there is no progress in curbing price growth.

This week, the economic calendar for the euro area is empty, and the euro's dynamics will be determined after the US inflation data on Wednesday.

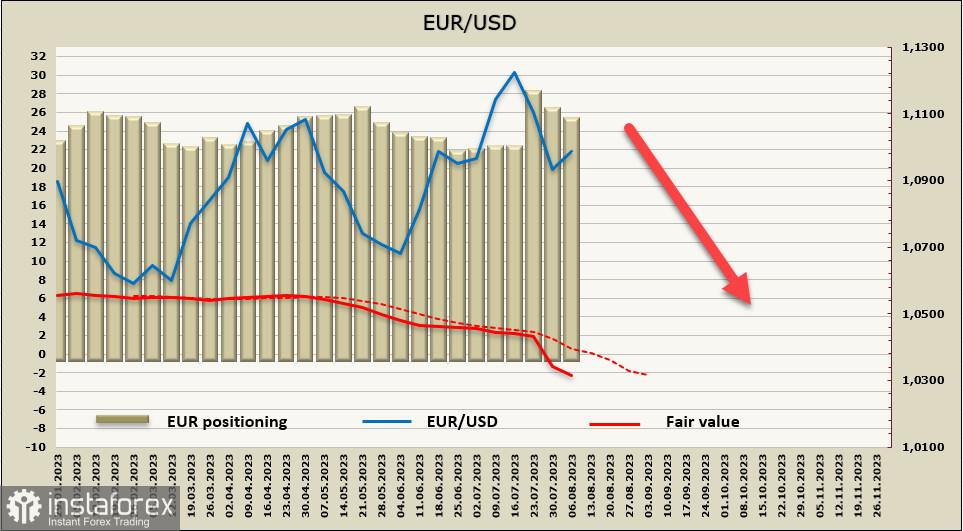

The net long position on the EUR decreased by 0.9 billion during the reporting week to -23.6 billion. Although positioning on the euro remains bullish, long positions have stopped growing and have remained practically unchanged for six months, indicating that investors do not see any good reason to strengthen the euro. The calculated price confidently moves downwards.

EUR/USD has formed a new local low at 1.0912, which exactly corresponds to the target set a week ago, but it lacked strength. Nevertheless, it is expected that the upward retracement is a short-term trend, followed by another wave of decline. It is anticipated that the retest of support at 1.0910/20 will be more successful, and the euro will move lower, with the nearest targets at the technical level of 1.0875, followed by 1.0830. The medium-term target is the support zone at 1.0780/0810.

GBP/USD

As expected, the Bank of England raised its interest rate by 0.25% to 5.25%. During the meeting, the cabinet members had divided opinions - two voted for a 50 bps hike, one suggested leaving the rate unchanged, and the remaining six voted for a 25 bps hike.

The main comment on the decision to raise the rate was that inflation is still at a high level and needs to be lowered, but it was also noted that previous rate hikes negatively affected economic activity. The forward guidance remained unchanged, and the key theses on monetary policy were left unchanged, but there was a caveat - the BoE considers the current rate to be restrictive and will maintain the restrictive rate for a long period to sustainably return inflation to 2%. This may indicate that the BoE is preparing the markets for an upcoming pause.

If the market concludes that the BoE will take a pause at the September 21 meeting, the pound will face additional pressure, and its decline will be highly likely. However, it is premature to make predictions about such a scenario at this point.

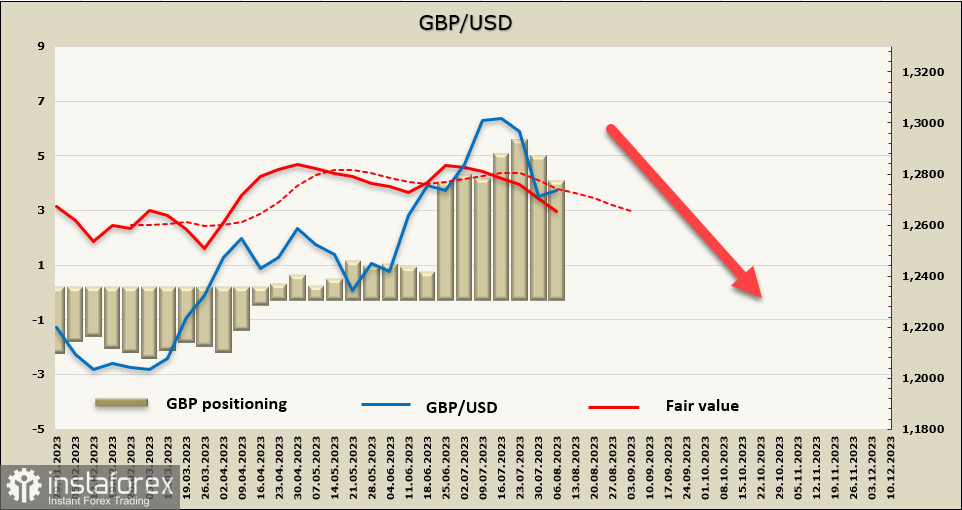

The net long position on GBP decreased by 0.8 billion during the reporting week, to 4.0 billion. The calculated price is directed below the long-term average and is leaning towards a decline.

Last week, the pound set a new local low at 1.2619, and after the correction, which likely has already ended, it is highly likely to resume its decline. The main target is the support zone at 1.2450/70, followed by 1.2240, but it is still too early to say if the movement towards this target will be stable and unstoppable.