English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Everything eventually comes to an end. The good and the bad. It seems that the best days of the British pound are now behind us. Sterling, which had been leading gains in the G10 currency race for a long time, lost ground in August. Even raising the interest rate by 25 bps to 5.25% did not help. The Bank of England called its monetary policy restrictive for the first time. This suggests that the peak of borrowing costs is already close. If so, then the main advantage of GBP/USD has either played out or is about to do so.

Back when UK inflation continued to rise at 10% or more by the end of the first quarter, while it was decreasing in the US, investors were betting on the BoE's borrowing costs rising to 6.5%. This secured the favorite tag for the pound. However, the CPI's slowdown to 7.9% seems to have removed the blindfold from the sterling fans' eyes. How can one talk about 6% or more now? The economy is already shaky, and on top of that, the central bank will continue to hike rates. Do you want to completely ruin it?

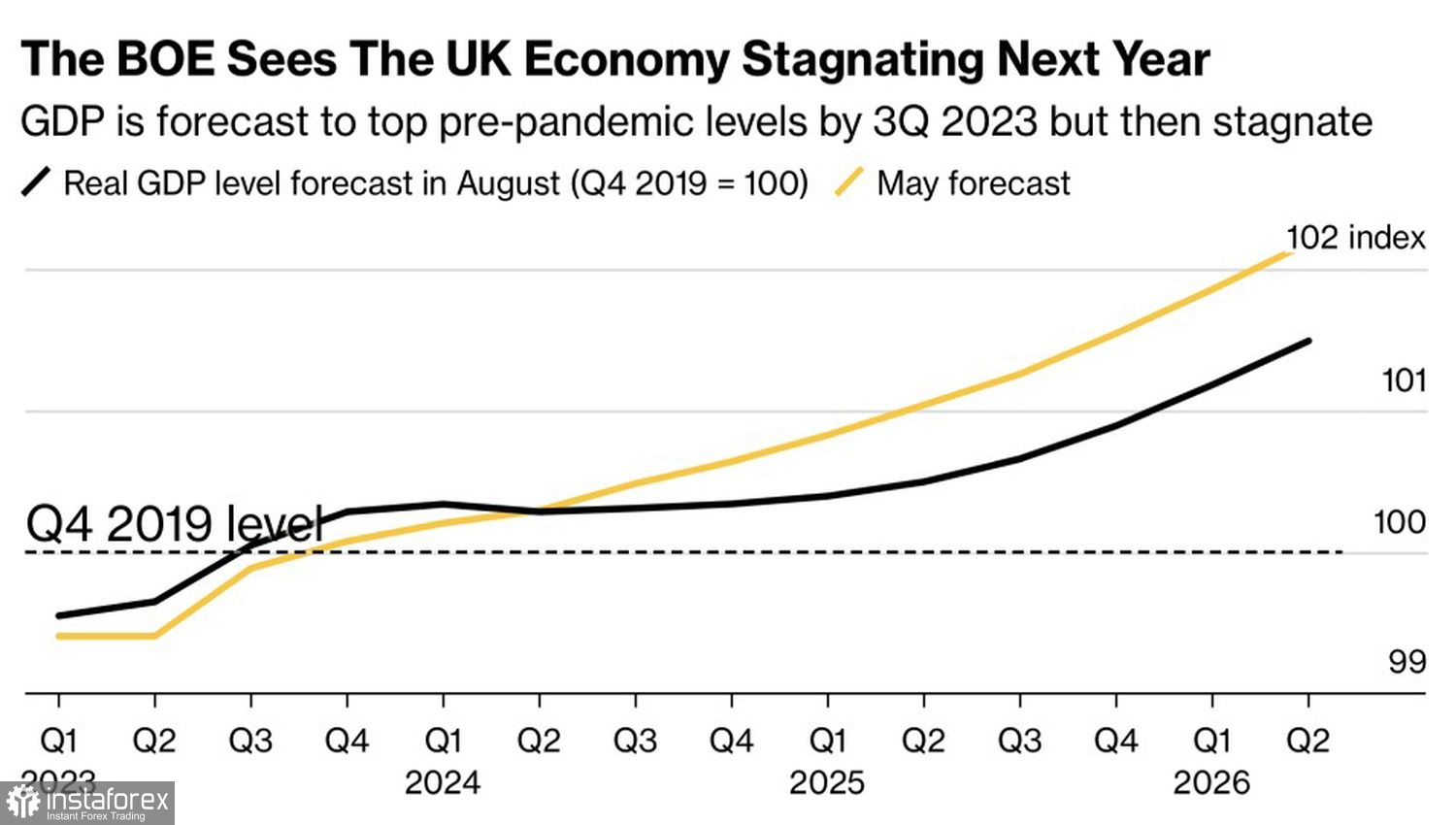

Unlike most G7 countries, Britain will only be able to return to pre-pandemic levels in the third quarter of 2023. Others have done that a long time ago. The US looks good these days, despite the Federal Reserve's aggressive cycle of monetary tightening. Investors, given that it is nearing the end, prefer currencies of those countries that can please it with economic growth. Unfortunately, Great Britain is not one of those.

UK GDP

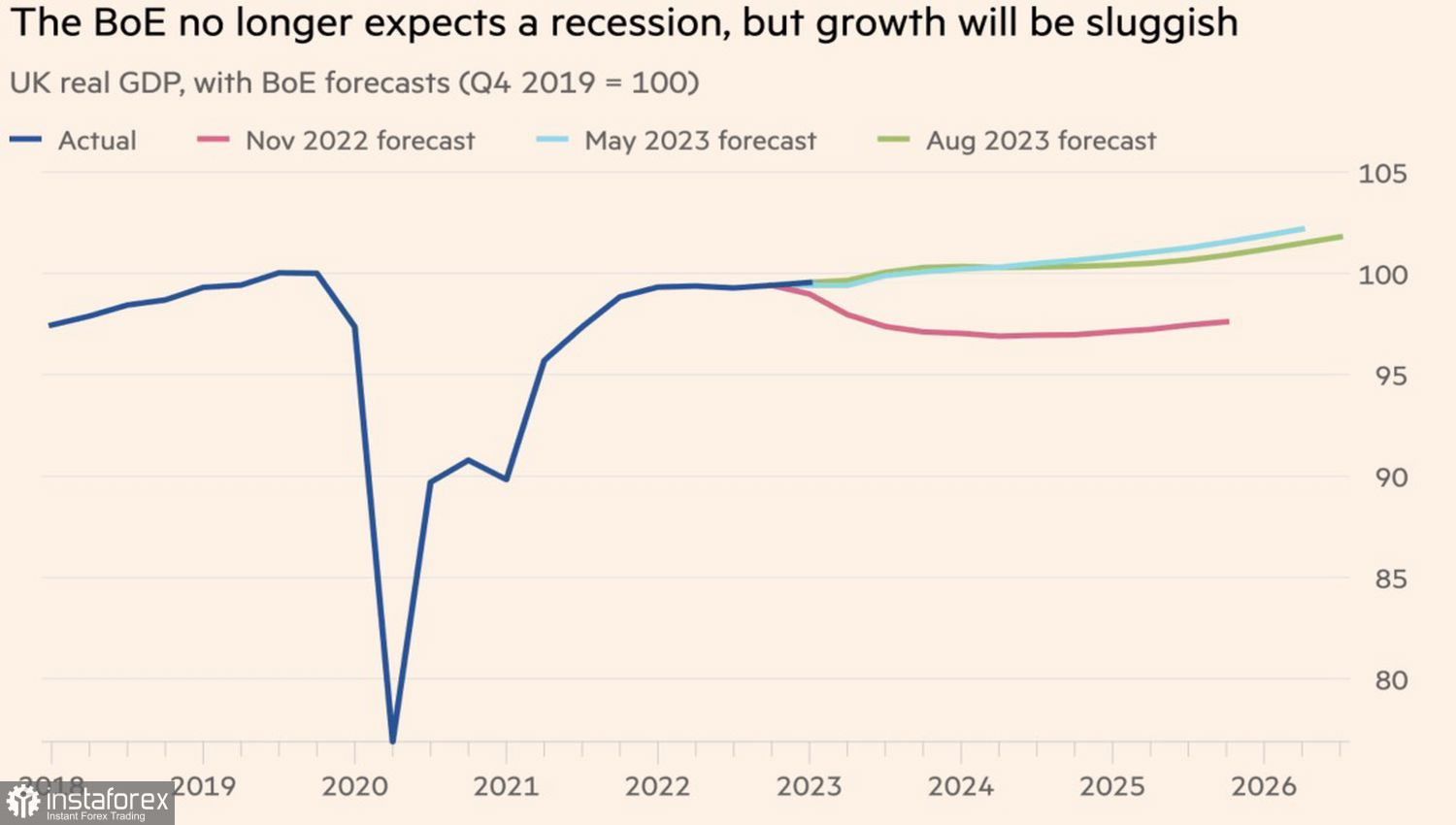

Back in 2022, the BoE forecasted a prolonged recession. The fact that Britain managed to avoid it became the catalyst for the GBP/USD rally. However, now investors have sobered up. They understand that the latest BoE estimates indicate weakness, not strength in the economy. Modest growth of 0.5% in 2023 and 2024, followed by +0.25%. BoE Governor Andrew Bailey and his colleagues believe that the monetary tightening will begin to bite in the future. Chief economist Huwe Pill claims that the rate increase from 0.1% to 5.25% is already working. The labor market is cooling down, which will ultimately slow down inflation.

Unemployment in Britain is rising, and local companies are hiring new permanent employees through recruitment agencies at the slowest pace since mid-2020. At that time, the country was under COVID-19 isolation. On the other hand, salaries are increasing very rapidly. However, looking at their slowdown in the US, one can assume that Great Britain will follow suit.

Bank of England GDP forecasts

This week, the key events for the pound will be the GDP data for the second quarter and US inflation for July. The acceleration of consumer prices in the US amid a weak economy in Great Britain is an argument in favor of extending the peak for GBP/USD.

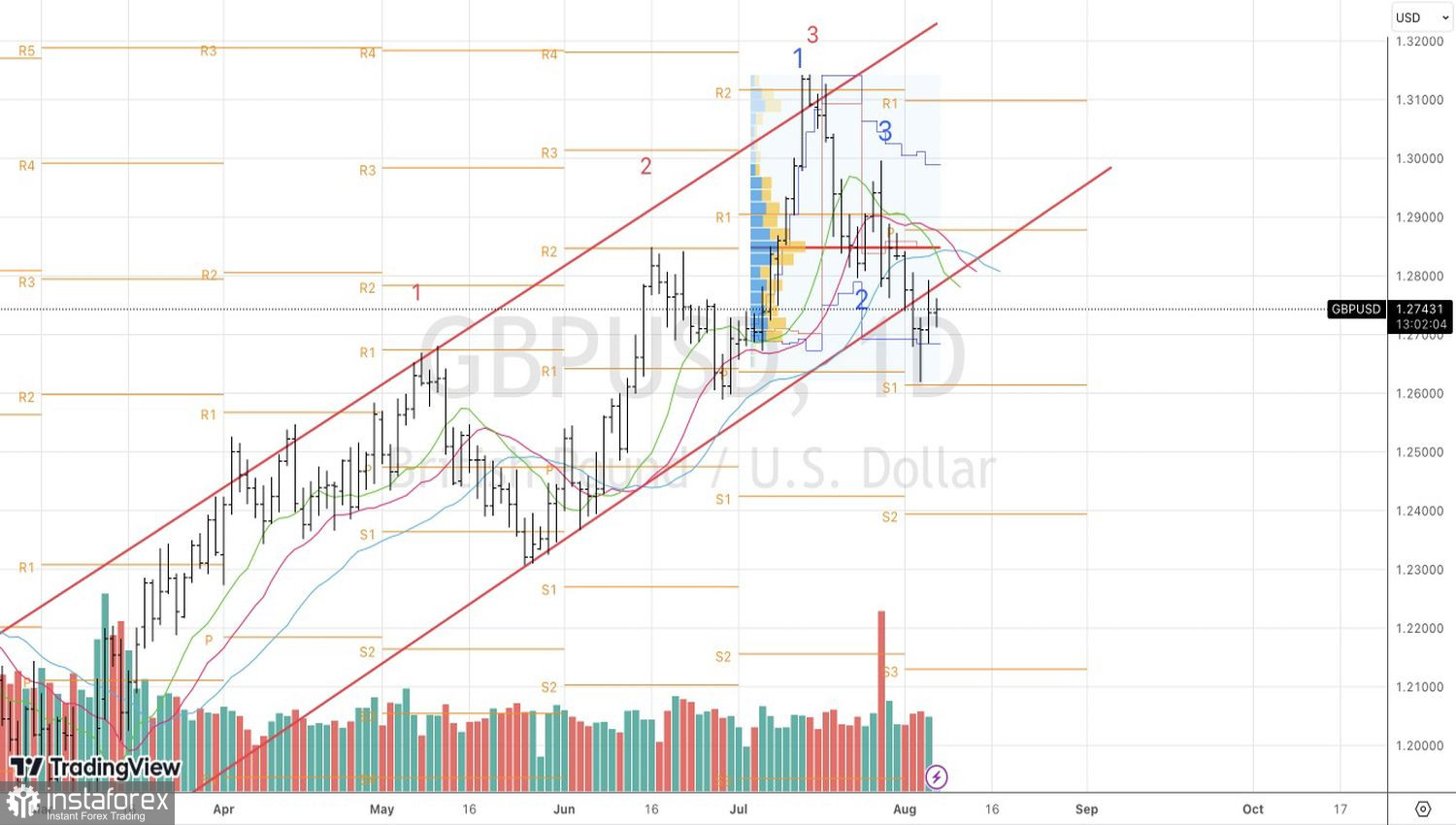

Technically, on the daily chart, there was a retest of the lower band of the ascending trading channel. The rebound indicates the bulls' weakness. At the same time, falling below support level at 1.2685 may become the basis for building up the shorts formed from 1.277.