English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

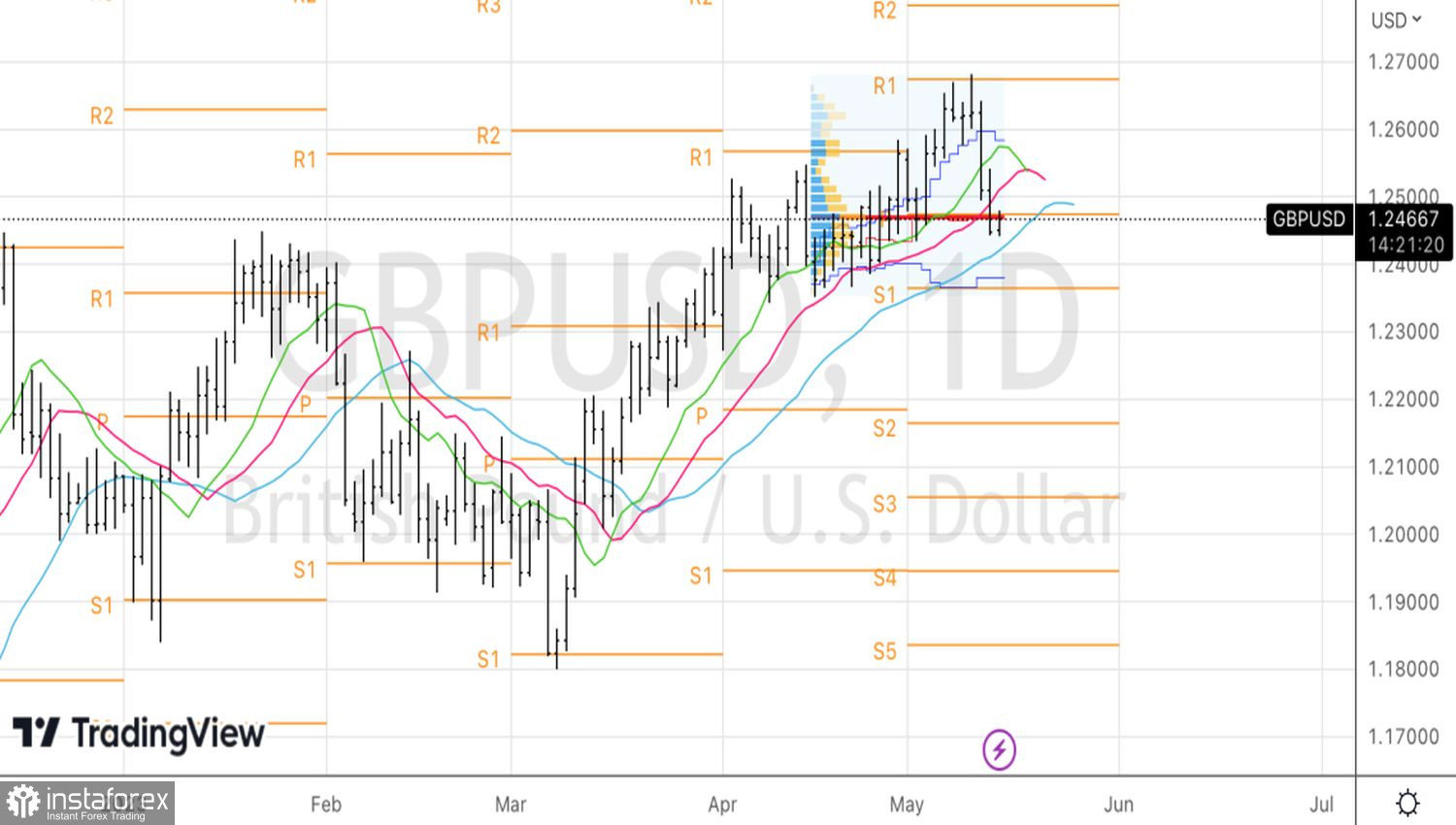

Buy the rumor, sell the fact. The Bank of England's decision to raise the repo rate by 25 bps to 4.5% was widely anticipated in the market and became a catalyst for closing long positions in the pound. This initiated the GBP/USD pullback. Despite the most significant improvement in BoE's economic forecasts since 1997, investors' desire to secure profits and the strengthening of the U.S. dollar against major world currencies left no chance for sterling bulls.

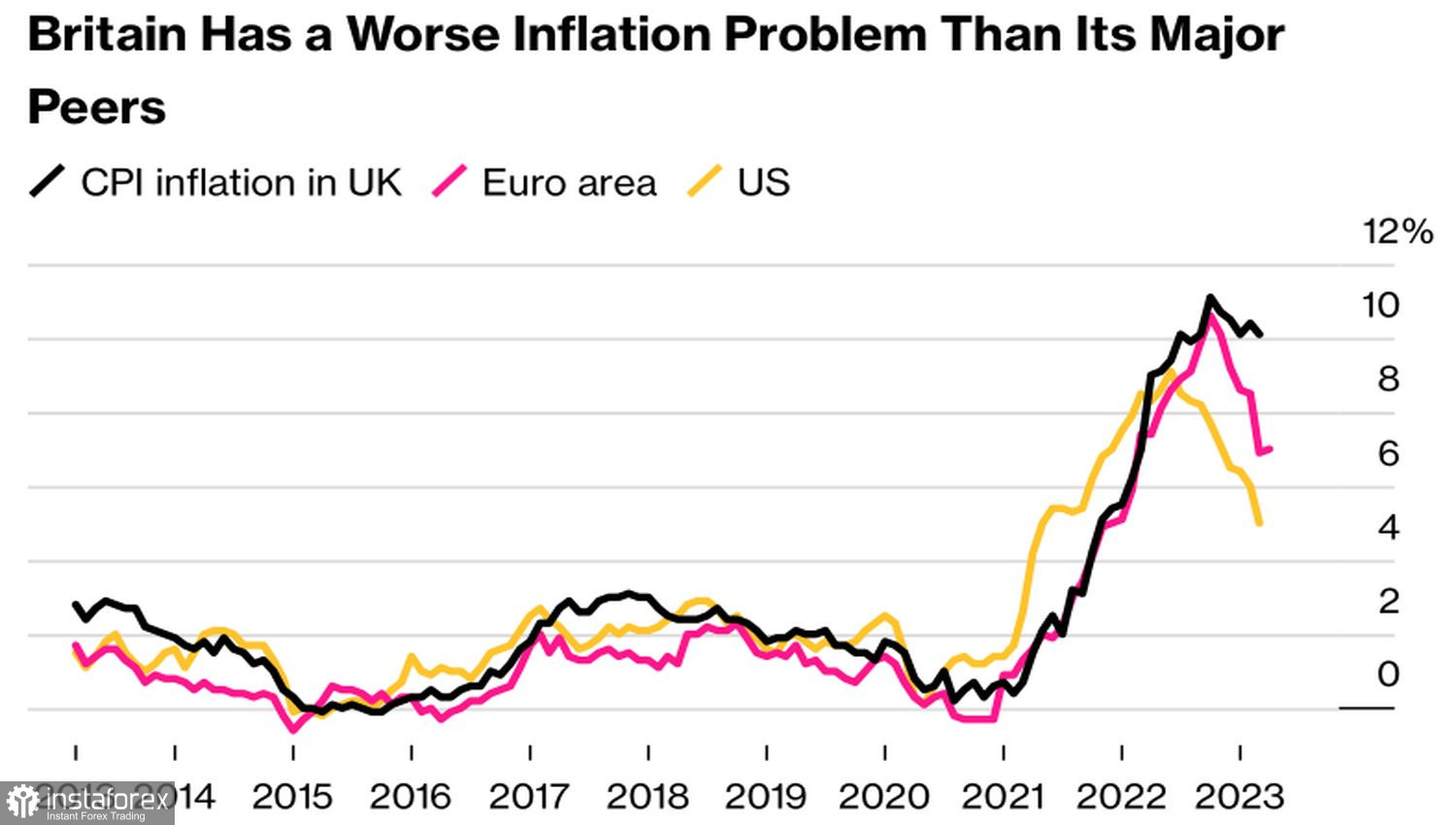

The Bank of England's verdict to raise the repo rate by a quarter point was a forced measure. Inflation in the UK is losing steam much more slowly than in the U.S. or the Eurozone. Salaries are growing faster than the BoE would like. And instead of a recession, the economy is stagnating. Meanwhile, after the Fed and ECB increased borrowing costs, derivatives increased the chances that the Bank of England would make the same 25 bps move, up to 90%. If you disappoint the markets, expect nothing good.

Inflation dynamics

Thus, the BoE had no choice but to raise rates and signal further growth. After its May meeting, investors expect the cost of borrowing to increase from 4.5% to 4.75% in June, with a 65% probability. The chances of reaching a 5% mark in September are estimated at over 50%.

In theory, this should support GBP/USD. However, observing how cautiously MPC members speak about future monetary restrictions, you start to doubt this. According to the head of the Bank of England, Andrew Bailey, the regulator is approaching the moment when it needs to take a break—from the perspective of interest rates. But so far, there is no evidence to know exactly how to act. Chief Economist Huw Pill noted that if the Central Bank sees more evidence that inflation is slowing, then the prospects for borrowing costs will be different.

Thus, the BoE has switched to autopilot mode. It will make monetary policy decisions based on the data. Formally, the UK's GDP growth of 0.1% in the first quarter could have been a catalyst for increasing the likelihood of monetary restriction. The economy has avoided the recession that the Central Bank talked about in 2022. Now it predicts stagnation and inflation at 5.1% by the end of the year.

In fact, the fact that the UK managed to avoid a recession is already accounted for in the GBP/USD quotes. It will not make a difference in the market. Investors are much more concerned about their own mistake regarding the Fed's "dovish" pivot. Recognizing it forces them to return to the U.S. dollar. Derivatives have raised the chances of a federal funds rate hike in June to 17% after the University of Michigan's long-term inflation expectations rose to 3.2%, the highest level since 2011.

Technically, a full-blown correction has begun on the GBP/USD daily chart. A rebound from the 1.2675 pivot level allowed us to sell the pair. Failed assaults on the fair value at 1.2475, as well as dynamic resistance in the form of a combination of moving averages near 1.254, will signal to increase short positions.