English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Market sentiment dipped ahead of the release of key consumer inflation data in the US. This follows the sharp surge observed last week amid strong data on job growth, which raised hopes that the region will avoid falling into recession and that the Fed would stop increasing interest rates aggressively. Additionally, the World Health Organization (WHO) announced the removal of existing restrictions on business activity.

Over the past two months, dollar was trading in a very narrow range, clearly indicating a stable expectation from investors for at least a pause in interest rate hikes in June, if not a complete end to the cycle. The Bank of England, the European Central Bank (ECB), and other major central banks of economically developed countries, excluding the Bank of Japan, will also not stand aside and will raise borrowing costs to curb inflation.

A halt in the decline of consumer inflation, as well as its limited recovery, can greatly change the balance of power in the markets. If the upcoming consumer price data shows even a slight upward trend, the Fed could continue to raise interest rates, not minding the strong labor market figures presented last Friday. It is precisely this scenario that forces market participants to exercise caution, as seen in the decline in market volumes and activity. This situation may persist today and tomorrow until the publication of US inflation data.

Forecasts for today:

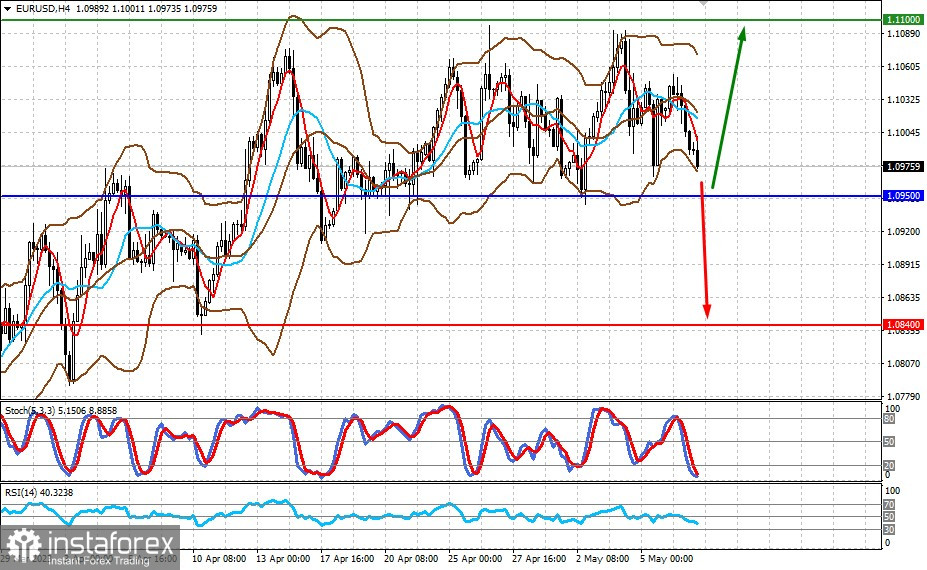

EUR/USD

The pair remains trading within the range of 1.0950-1.1100. Rising inflation in the US may cause a local decline in the pair to 1.0840, while a decrease in the figure will lead to a price increase to 1.1100.

GBP/USD

The pair is consolidating above the support level of 1.2570. If reports show an increase in US inflation, there will be a decline to 1.2480. If not, then there will be a price increase to 1.2700.