English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The calendar for the last five days of April looks quite busy. We have data releases on U.S. and European GDP, German inflation, and the U.S. Personal Consumption Expenditures index, as well as statistics on inflation expectations from the University of Michigan. There is enough data for the EURUSD pair to determine its further direction. But why hurry if the Fed and ECB meetings will take place next week?

The central banks are approaching these meetings in different moods. The cooling labor market, declining retail sales, slowing inflation, and the banking crisis dictate the need for the Federal Reserve to put an end to the process of tightening monetary policy. If someone believes that the turmoil in the U.S. credit system has already ended, I recommend looking at the quarterly report of First Republic. This bank avoided bankruptcy but paid a high price. A sharp decline in profitability of operations suggests that it continues to struggle for its existence.

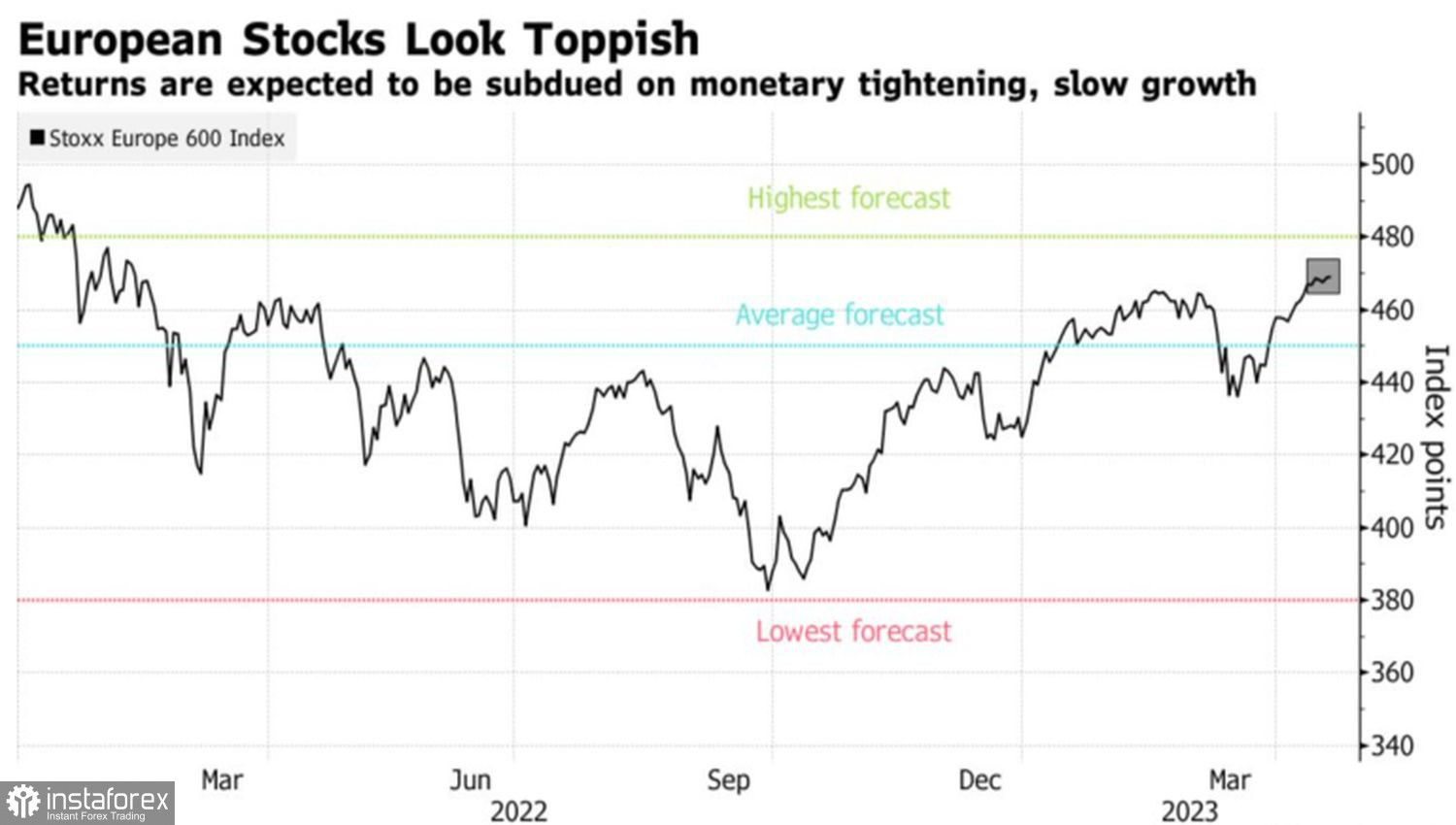

The futures market expects the federal funds rate to peak by June and then decline to 4.5% by the end of 2023. Different preferences apply to the deposit rate. Derivatives predict its increase from the current 3% to 3.75% with subsequent holding at the ceiling, at least until the end of this year. Meanwhile, hawkish rhetoric from the Governing Council members and the continuation of the aggressive monetary restriction cycle could adversely affect European equities. According to the Bloomberg consensus forecast, EuroStoxx 600 will fall by 4% by the end of the year.

Dynamics and forecasts for the European stock market

However, the ECB is much more concerned about core inflation, which continues to update historical highs. This allows the Governor of the National Bank of Belgium, Pierre Wunsch, to say that markets underestimate the determination of the European regulator. In fact, the deposit rate could rise to 4%, not 3.75%, as derivatives predict. Isabel Schnabel, a Governing Council representative from Germany, does not rule out an increase in borrowing costs by 50 basis points at the central bank's May meeting, saying that current inflation data and the currency bloc's economic stability allow for this.

When an ECB dove like Chief Economist Philip Lane says that rates should be raised at the next meeting, the issue with the next act of monetary restriction can be considered closed. The only thing left is to find out the magnitude of the step: 25 or 50 basis points? The futures market gives a 67% probability of the first option, which is also the preference of most Bloomberg experts, but who knows what the European Central Bank will decide on May 4?

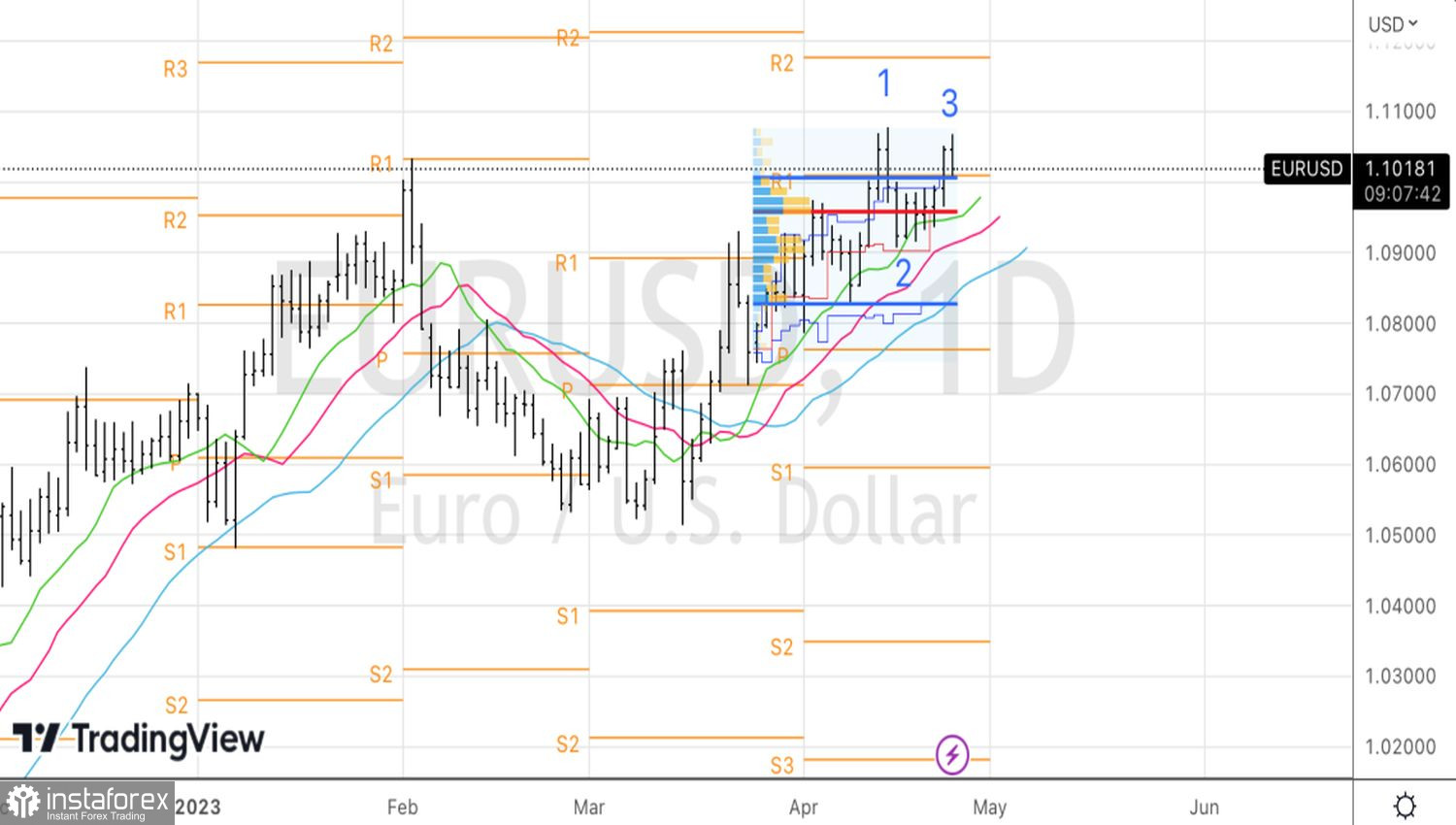

Technically, despite the growth of EURUSD, the subsequent decline in the pair's quotes keeps the reversal pattern 1-2-3 relevant. In the case of its implementation, the risks of a pullback to the upward trend will increase. Therefore, we continue to adhere to the previous strategy—the pair's inability to cling to 1.1 is a sign of the bulls' weakness and a reason for selling.