English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

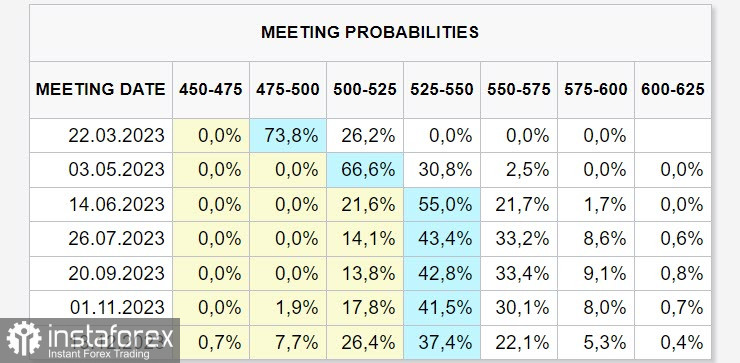

The CFTC has resumed releasing reports after taking a break that lasted nearly a month. The data available so far is from January 31 and is already out of date. The release of the reports is expected to be expedited and by the middle of March, the CFTC's will be back on a normal schedule.

Nevertheless, we can see some useful things from the report. The cumulative short position on the USD increased by 3.6 billion, the largest bearish position on the USD since 2020 was formed, that is, before the Federal Reserve revised its rate targets, the market was actively set up to sell off the USD. That all changed at the February 14 FOMC meeting, expectations for yields of the world's leading currencies were revised, and the new CFTC reports will obviously show a major shift in positioning.

The revised 4Q U.S. GDP data brought a synchronized rise in all price indexes. Moreover, consumer spending increased 1.8% in January (forecast 1.3%), while headline inflation rose to 5.4% instead of the expected 4.9% decline, which means that fears that the slowdown in inflation will prove to be temporary have finally been confirmed.

The strong spending numbers have altered Fed rate expectations, and the futures now show only a 35% chance of a rate cut this year. By the end of the year, the markets are expecting a 5.5% rate, which gives the dollar an extra edge.

Rising inflation expectations have raised market expectations for other policy rates as well, with the recent spike in markets' inflation expectations not coinciding with higher commodity prices, which may indicate fears of more persistent core inflation. Core consumer prices in Japan jumped 4.2% in January, which is fantastic for an economy that has battled deflation for decades.

The market will be focusing on the US Durable Goods Orders report in January with the ISM reports on Wednesday and Friday being the key events of the week. The dollar is still the favorite currency so far, there is no reason to expect a reversal.

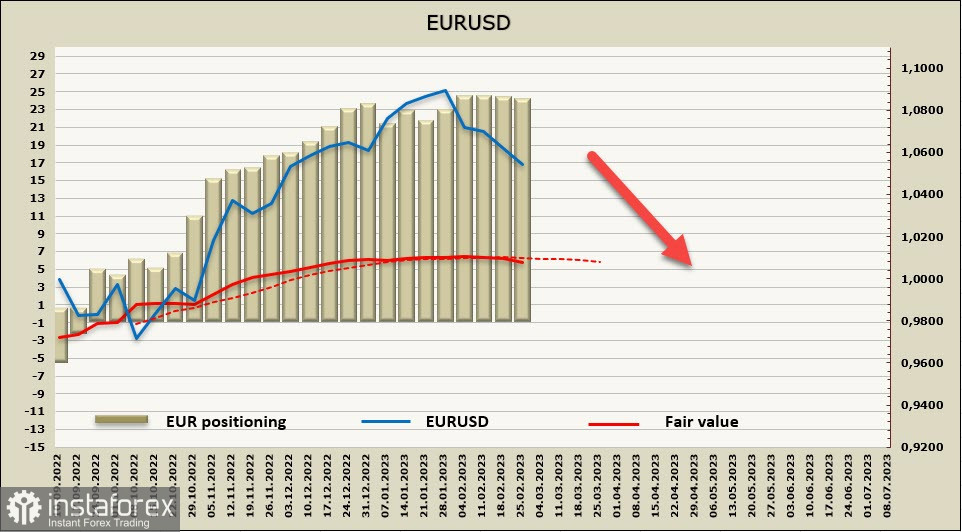

EURUSD

Business sentiment in the eurozone remains subdued, according to the European Commission, confidence across the service and industrial sectors deteriorated in February instead of the expected growth. Obviously, it's not only about the stabilization of commodity and energy prices, the crisis may have a structural nature and be more protracted.

The German economy shrank by 0.4% in the fourth quarter of 2022, double the previous estimate. Falling capital spending and private consumption are primarily to blame. Germany's two-year bond yields rose above 3% for the first time since 2008. Meanwhile, Bundesbank president Joachim Nagel warned that the European Central Bank may have to raise rates significantly in the second quarter as well.

This week's main focus will be eurozone inflation data for February, which will be released on Thursday.

The settlement price goes down, but as long as the latest CFTC data is not available, the direction is tentative and may be subject to adjustments.

The rapid decline of EURUSD increases the probability of corrective growth, the nearest resistance is 1.0605/15, where the sell-off may resume. We assume that the probability of continuation of decline is high, the nearest target is the support zone of 1.0460/80.

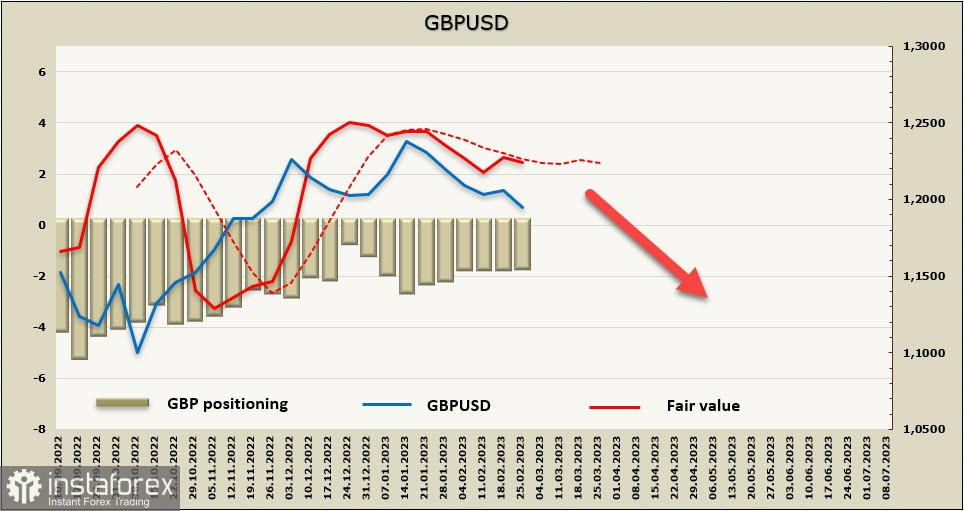

GBPUSD

The GfK consumer confidence index increased by seven points to -38 in February, bouncing back up from record lows but still well below long-term averages.

The growth of the index can hardly be regarded as sustainable, apparently reflecting the expected improvements in personal finances and the general economic situation, as the most difficult phase of the energy crisis is behind us. Nevertheless, the threat of recession is still high, as are inflation expectations.

There will be no important macroeconomic reports this week, but on Tuesday, three representatives from the Bank of England are expected to deliver speeches. This might push the pound if the representatives adjust the rate forecasts. As a whole, the pound, most likely, will follow the general market trends.

The settlement price is directed downwards for the time being.

Pound continues to trade in a wide range of 1.1830/1.2440, but with each passing day, the probability of falling from this range has been increasing. Resistance is at 1.2070/90, in case of attempts to rise to this level, a renewal of the sell-off is likely, I expect an update of the local low of 1.1934, and a long-term target of 1.1640.