English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The NonFarm Payrolls report knows how to surprise. One component of the key report surpassed forecast levels, emphasizing the ambiguity of the situation. But this time, the numbers were "just right": on Friday, almost all indicators came out in the green zone (except for wages), exceeding the forecast values. Such an impressive result allows the Federal Reserve to continue rate hikes, consolidating, so to speak, its success in the fight against inflation.

The language of dry numbers

The figures were really impressive. First of all, the growth was surprising. This component jumped by 517,000 (against a forecast of 193,000). December NonFarm Payrolls were revised upwards (260,000 jobs created vs. 223,000 previously reported). Private sector indicator grew up to 443,000 (the forecast was 190,000). By the way, prior to the Nonfarm, the ADP report came out rather weak at 106,000. In this case, we can talk about a significant discrepancy, which was eventually interpreted in favor of the dollar.

The unemployment rate declined to 3.4% in January, that is the lowest jobless level since May 1969. While most experts were confident that it would rise to 3.7%. In assessing the dynamics of recent months, we can talk about a downtrend here: the indicator has been consistently falling for three consecutive months.

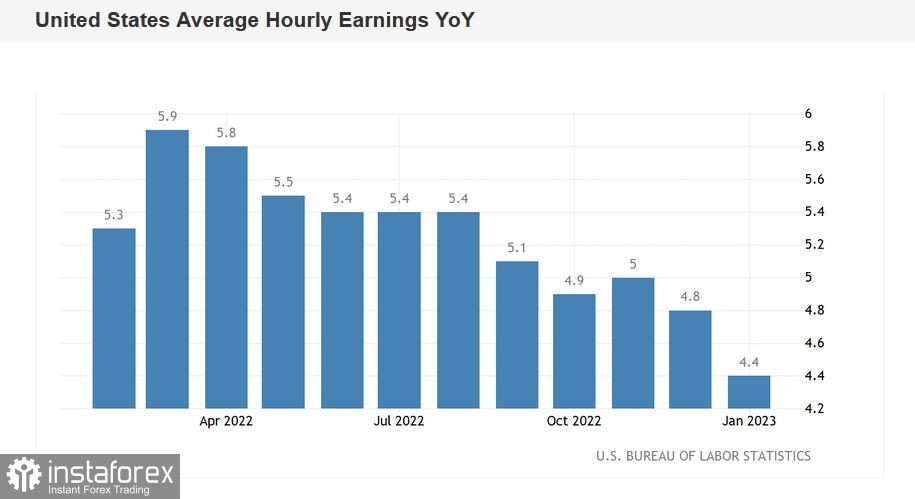

Remarkably, the drop in unemployment to a 53-year low occurred amid a slowdown in the inflation component. Average hourly earnings continue to show a downtrend (in annual terms). Friday's numbers (0.3% m/m and 4.4% y/y) added to recent inflation data.

What did Nonfarm say?

The report suggests that the Fed will maintain a "moderately hawkish" stance on the prospects for monetary tightening at its March meeting. We are talking about an almost guaranteed 25-point interest rate hike in March, and a possible 25-point increase at the end of the May meeting. Although much will depend on the dynamics of inflation indicators, this turn of events looks the most realistic. According to the CME FedWatch Tool, now the probability of the 25-point scenario in March is 86%. As for further prospects, here the market is still undecided. Today the probability of the 25 bps rate hike in May is at 48.2% whereas the probability of rate preservation (under the condition of a 25-point hike in March) is at 44.6%.

The Nonfarm data has strengthened the dollar's position throughout the market: the greenback has updated a two-week price low in EUR/USD, having tested the 7th figure. If it probably weren't for the weekend, the bears could have advanced to the support level of 1.0750.

At the same time, despite the powerful downward momentum, it is too early to talk about a trend reversal. In my opinion, the greenback will feel most insecure in the EUR/USD pair. Bulls will certainly counterattack and will not allow the bears to build a downward momentum.

Bulls lost the fight, but not the battle

The eurozone inflation report was released on Wednesday. The data turned out to be controversial, but at the same time it reflected one interesting trend: amid a slowdown in headline inflation, core inflation continues to stay at a record high level. Thus, the general consumer price index in January rose by 8.5% against the forecast of 9.0% (a downtrend has been recorded for the third month in a row). While the core CPI (excluding volatile energy and food prices) came out at 5.2%, the same as in December. In other words, in contrast to the US, where both core and headline inflation are consistently slowing down, in the eurozone, the core consumer price index remains at an unacceptably high level for the European Central Bank.

Following the results of the February meeting, ECB President Christine Lagarde announced a 50-point rate hike in March, which can be considered as straightforward. But at the same time, she put a question mark on further steps in this direction, "tying" the hawkish rate of the ECB to the dynamics of inflationary growth. Obviously, if core inflation in the European region continues to grow stubbornly (or stay at the achieved level), the ECB will raise the rate not only in March, but also at the next meeting.

In other words, the ECB may well present a "hawkish surprise" in the context of further hikes, while the Fed is more predictable in this regard. The Nonfarm only "approved" the March 25-point rate hike, while the Fed's further steps in this direction are a big question (which, by the way, is evidenced by the CME FedWatch Tool data).

Conclusions

Despite the strong downward momentum, short positions on the pair look, in my opinion, risky. At the beginning of the week, market emotions about strong Nonfarm will come to naught, after which the downward dynamics will probably begin to subside. Therefore, it would be best to maintain a wait-and-see position for the pair: if the bears do not overcome the support level of 1.0720 in the medium term (the lower Bollinger Bands line on the daily chart), then bulls will seize the initiative with a high degree of probability and return the price to area 8th figure, to the previous range of 1.0850-1.0950.