English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Anything that rises can stay high. After Federal Reserve Chairman Jerome Powell failed to play the role of super-cool hawk and released the market's animal spirits, EURUSD soared above 1.1. No doubt, the major part of the rally is due to the weakening of the US dollar, influenced by the improving global risk appetite due to the unwillingness of the Fed to respond to the improving financial conditions. Nevertheless, the euro is not in bad shape either. It has a stronger-than-expected economy and an aggressive European Central Bank. It is a potent mix which can push the major currency pair even higher.

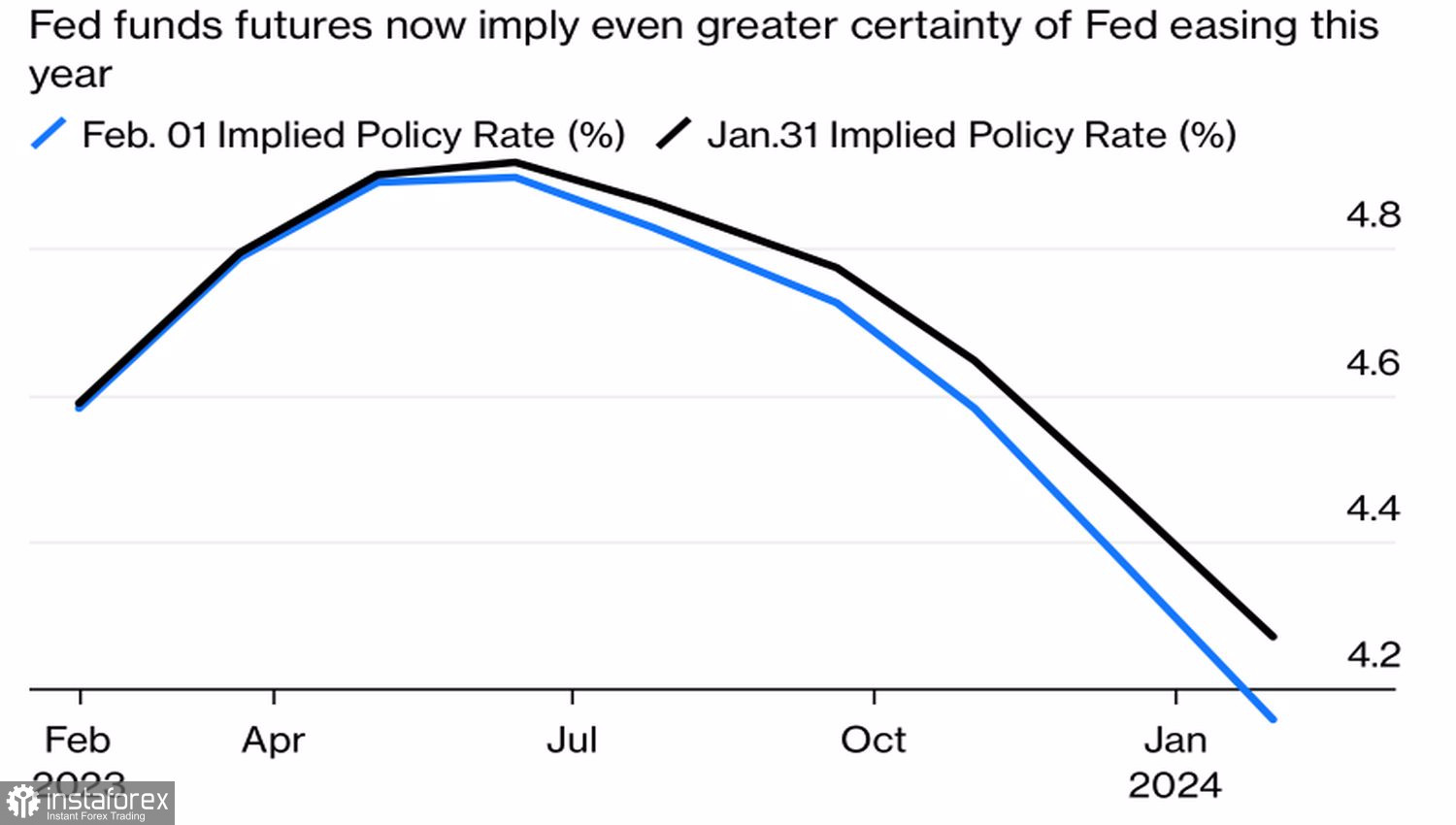

The more Powell talks, the more the markets become convinced that this is just empty talk. The central bank's future decisions depend on incoming data, and the situation is such that inflation is slowing faster than he expects. Even Powell has acknowledged the existence of disinflationary processes. Not surprisingly, in such an environment, derivatives have begun to signal a more aggressive reduction in the federal funds rate by the end of 2023. This circumstance has signed the U.S. dollar's death sentence.

Dynamics of expectations for the Fed Funds rate

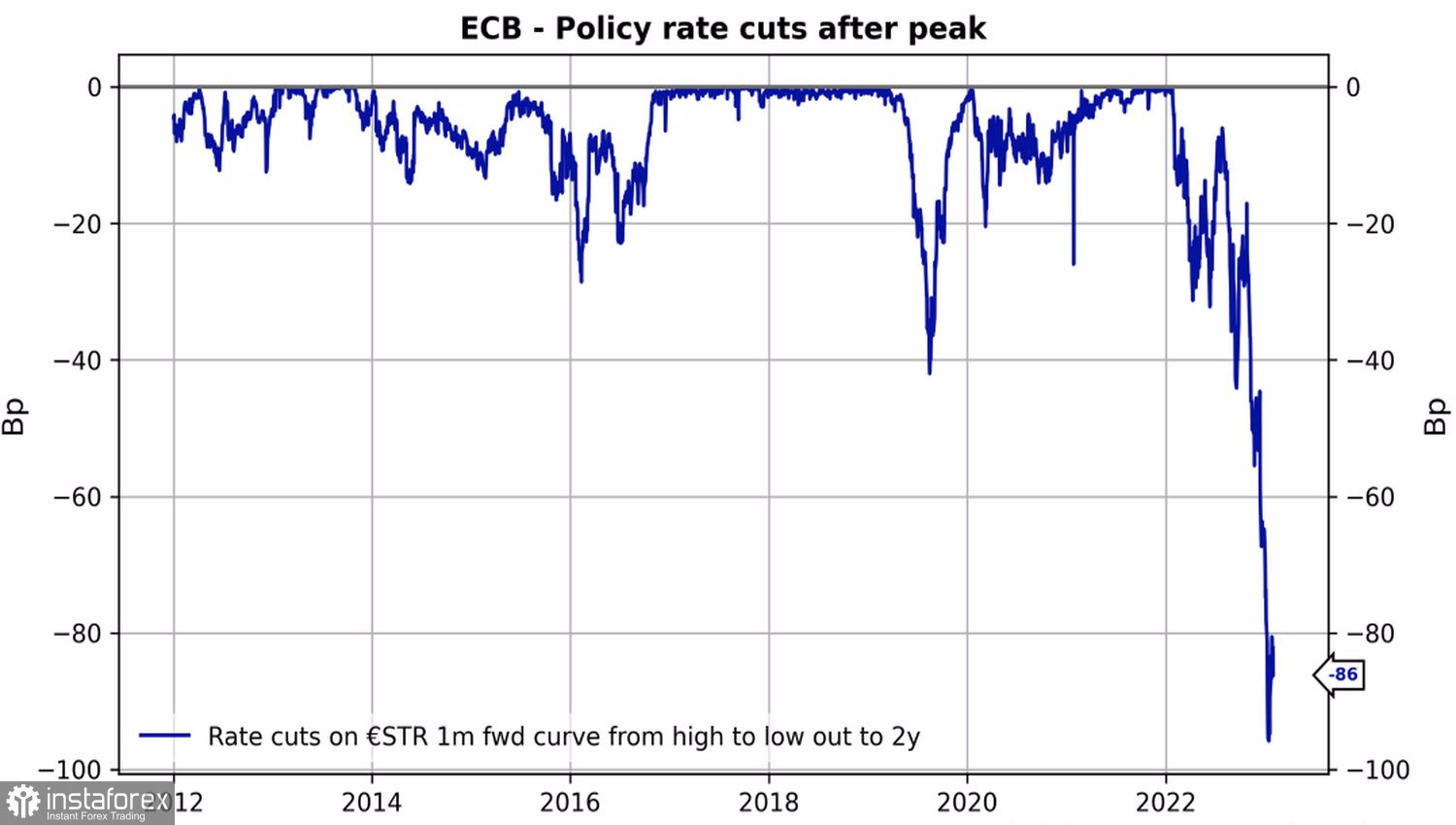

Interestingly, investors want to see a dovish pivot not only from the Fed, but also from the ECB. After peaking at 3.5%, they believe the cost of borrowing will begin to decline. And in 2024, the reduction will be as much as 86 bps, which is equivalent to a 25 bps cut at 3-4 ECB meetings. These projections are based on the market's abating expectations on inflation. While back in late 2022 swaps saw CPI peaking at 5% in September, that figure has now moved to August 2023. Their previous view was that inflation should have slowed to 3% in October 2024. The current one says the rate will see that level in April.

Dynamics of ECB rate cut expectations

Alas, the ECB is unlikely to cut rates without a weak economy. And the economy has been giving pleasant surprises on a regular basis lately. Add to this the positive from the opening of China - and the risks of the formation of a new extreme by European inflation after its slowdown will increase sharply. Central banks should be on their guard against repeating the mistakes of the Fed in the 1970s. Back then, the U.S. central bank believed too early in its victory over high prices.

These developments suggest that ECB President Christine Lagarde and her colleagues would raise borrowing costs to 3.25-3.5%, and then hold them at their peak for longer than the Fed would do. As a result, the differential between U.S. and European rates will continue to narrow and EURUSD will continue to rise. Any form of decline, including the one caused by consolidating long profits, should be considered as a pullback.

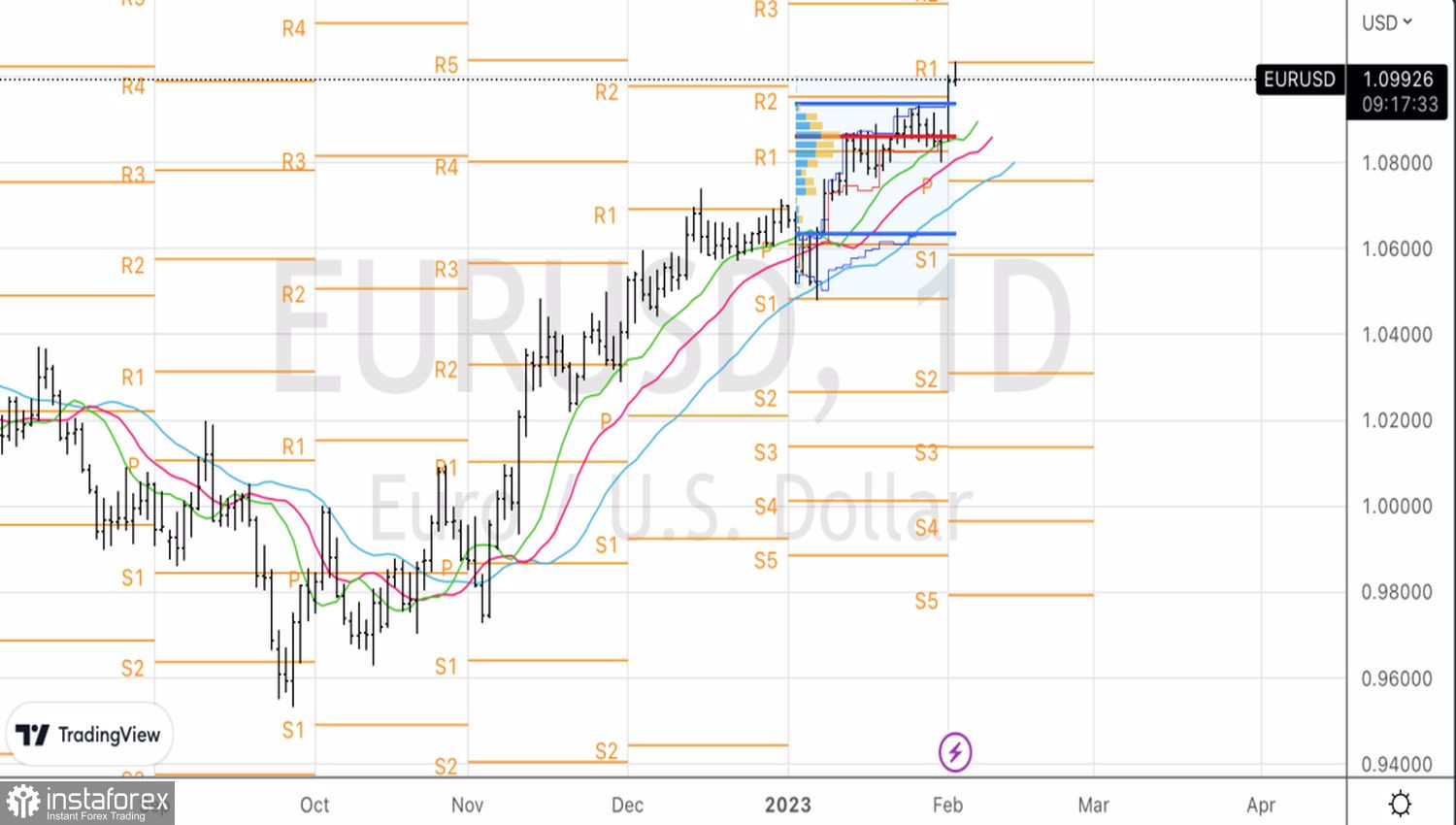

Technically, applying the pattern underlying the 80-20 principle followed by the pin bar on the daily chart creates preconditions for the short-term correction in the direction of 1.094-1.095. The rebound from the formed pivot level and the upper limit of the fair value of the convergence zone will make it possible for us to open longs.