English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The dollar is weakening again at the beginning of today's European trading session, while demand for traditional protective assets—U.S. government bonds, precious metals, yen—is growing.

The yield on 10-year U.S. Treasury fell today to a new, almost 4-week low of 3.510%, while gold took off at $1,885.00 per ounce, corresponding to 8-month highs. Silver is slightly behind but has also been bullish since mid-October, trading near $23.70 an ounce in XAG/USD, just below the January high of $24.53.

Additional support for the yen is provided by Japanese macro statistics published earlier this week. Thus, the country's balance of payments rose to 1,803.6 billion yen in November, surpassing the forecast for growth to 471.1 billion yen, which also turned out to be dramatically better than last month's deficit of -64.1 billion yen. At the same time, the core consumer price index in the Tokyo region, published on Monday, adjusted from 3.8% to 4.0% in December, which was the fastest growth in four decades and well above the Bank of Japan's target level of 2%. This increases the likelihood that the Bank of Japan may indeed abandon a large-scale economic stimulus program and a negative interest rate. In this sense, the Bank of Japan has much more room for maneuver, unlike the Fed, and the sellers of the USD/JPY pair have far-reaching levels of profits in short positions.

So, the yen is growing today both against the dollar and in cross-pairs. In particular, the dynamics of the EUR/JPY pair is interesting. As of writing, it is trading near the 141.00 mark, storming strong support levels 141.45, 141.27 and declining to the 140.30 key support level. It is noteworthy that the euro is growing against the dollar in other major cross-pairs. Therefore, it is logical to assume that there will be a rebound and growth of EUR/JPY near the current "round" mark of 141.00, taking into account also the fact that today the pair has already chosen its average intraday volatility of 130–150 points.

At the same time, given the importance of today's publication (at 13:30 GMT) of U.S. inflation data, the option of further strengthening of the yen and a decrease in EUR/JPY down to the 140.30 key support level cannot be rejected either.

As for today's publication mentioned above, economists assume that the consumer price index in December will fall to 6.5% (from 7.1% in November) and the core CPI to 5.7% (from 6.0% in November), which confirms the market's expectations of a further decline in inflation in the United States. Will this support the U.S. dollar, given that the weakening of inflation is still a positive factor for the national economy, and the Fed had already begun to slow down its tightening in December? If the data is confirmed or even softer, a further fall in the dollar is unavoidable.

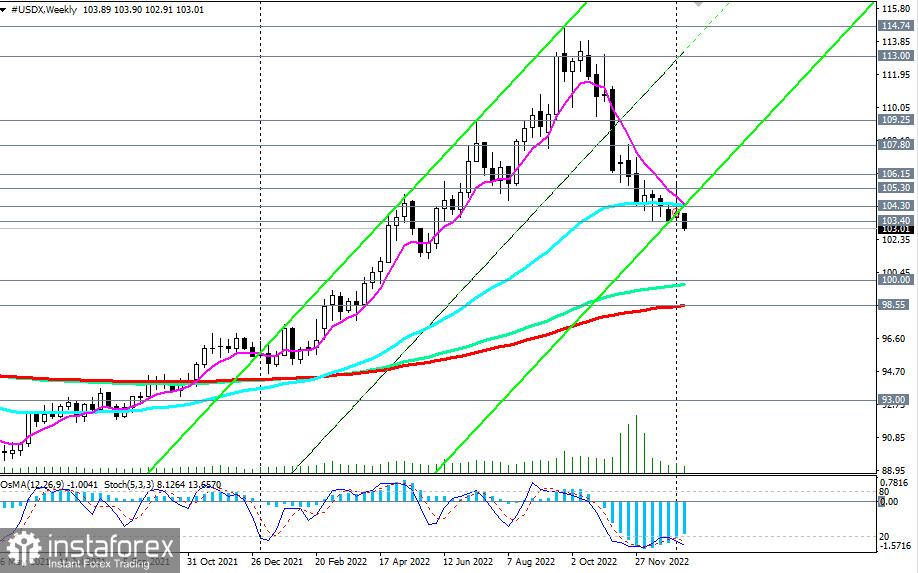

From a technical point of view, the breakdown of this week's low at 102.91 will be a signal for a further fall in the dollar index (CFD #USDX in the MT4 trading terminal). In this case, the decline in DXY may accelerate towards the key long-term support levels 100.00, 98.55. A break of the 93.00 support level will return the DXY to the long-term bear market zone.