English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

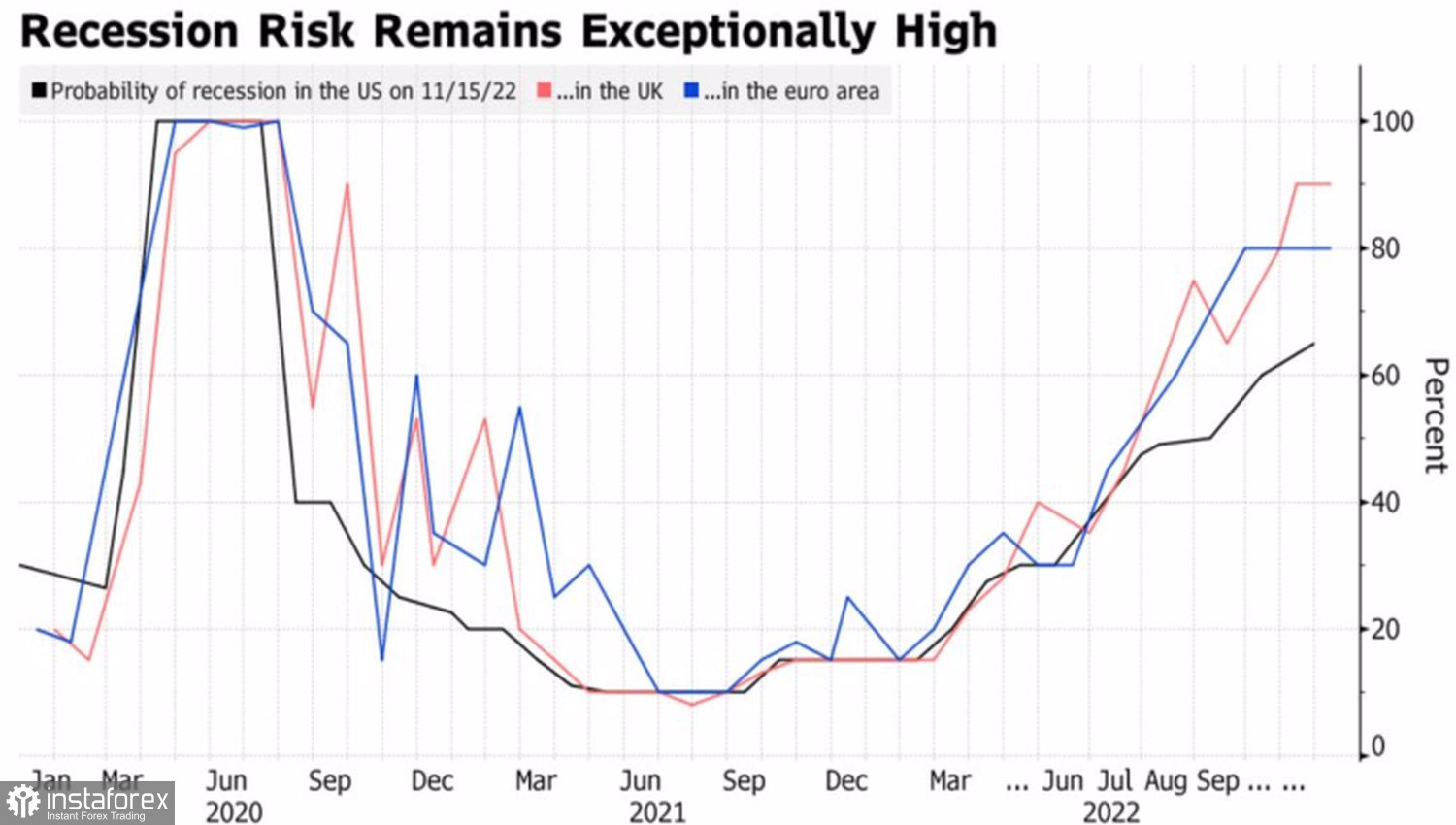

Even though the world's leading central banks are slowing down the rate of monetary policy tightening, they continue to raise rates. Even as signs emerge that economies are either moving toward recession, as in the case of the United States, or are already in recession, as in the case of the eurozone and Britain. The fact that monetary tightening continues cannot but affect oil prices. Recession will lead to a reduction in global demand, which in the context of stable supply leaves the downward trend for Brent in force.

If the latest "dove" in the face of the Bank of Japan takes a step towards abandoning its ultra-loose monetary policy, widening the boundaries of the target range of yields, what should we expect from the rest? If inflation suddenly picks up in 2023, the Fed and companies will have no choice but to keep raising rates. Recession will become a reality, global oil demand will decline, and the Brent bulls will be left fooled.

Dynamics of recession probabilities in the world's leading economies

Their recent activity was associated with China's departure from the zero-COVID policy, with the U.S. decision to start buying oil to replenish strategic reserves after their reduction by 180 million barrels, as well as with the weakening of the U.S. dollar. Nevertheless, the rapid opening of China's economy is fraught with an increase in deaths by 1 million and an increase in infections to 10 million at its peak. If people actively get sick, productivity will decrease, supply chain problems will worsen, which will affect the entire global economy.

No one knows exactly how the situation in China will develop, and uncertainty increases the chances of Brent consolidation. On the one hand, the drop in business confidence in China, according to a World Economics survey, has fallen to its lowest level since January 2013, which undermines domestic demand in the largest consumer of oil. On the other hand, Xi Jinping promised to focus on the economy, which is encouraging for Brent fans.

So far, there are no particular problems with the proposal. Russia continues to supply oil to India on tankers insured by the EU, which indicates that the established price ceiling of $60 per barrel is observed by counterparties. Contrary to Moscow's loud statements that sales will not be made. The current price of oil seems to suit everyone. Problems may start later if prices fall.

Thus, fears about a global recession are pushing Brent down, but U.S. oil purchases to replenish strategic reserves, a weakening U.S. dollar and faith in additional monetary and fiscal stimulus from China are helping to stabilize oil.

Technically, on the daily chart of Brent, a 1-2-3 reversal pattern could be activated if the pivot point at $83.35 per barrel is broken. This would increase the risks of a pullback. On the contrary, a drop below $78.45 would be a reason to sell.