English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

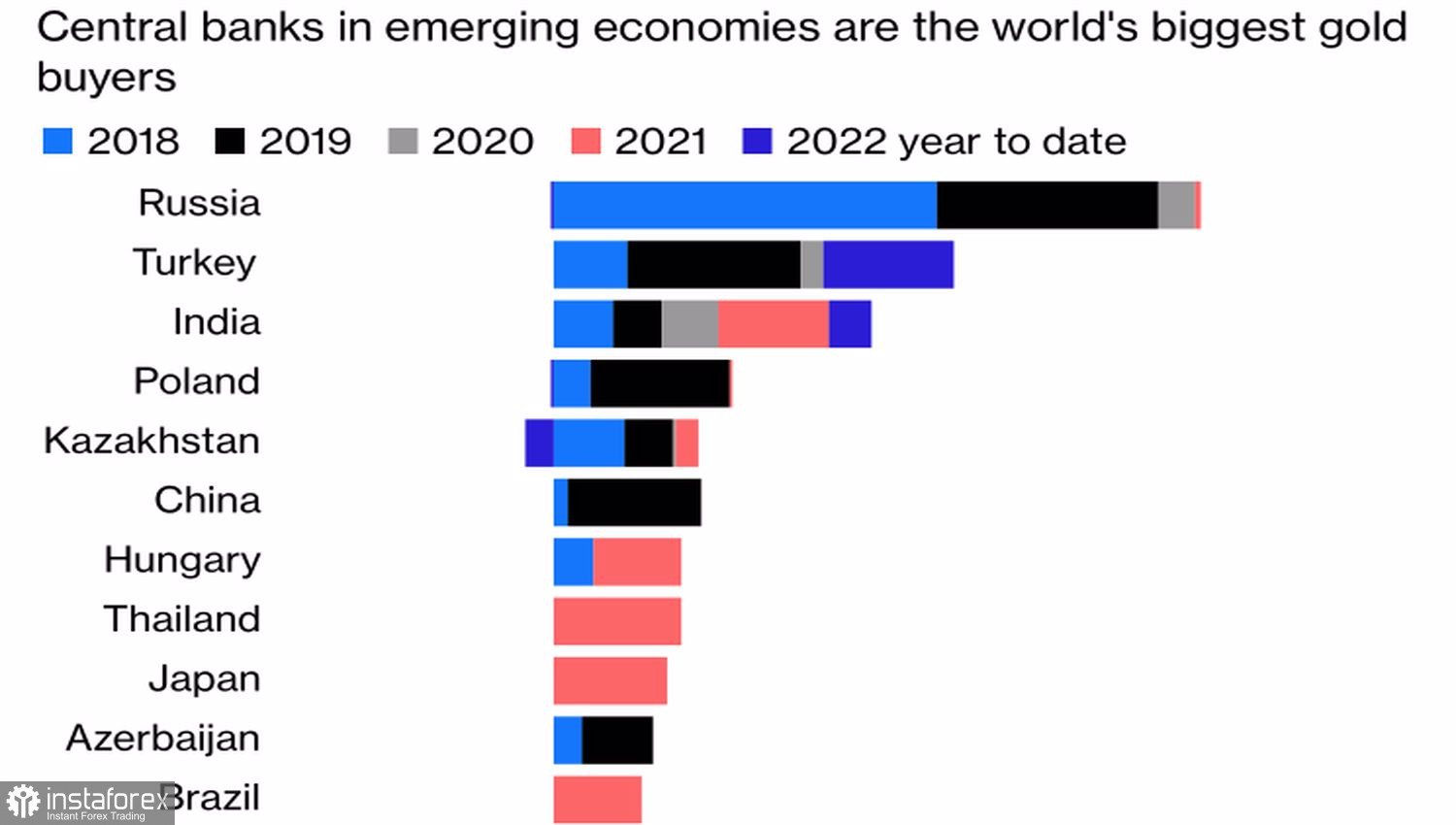

When preparing for the apocalypse, you need not only to dig a shelter and stock up on canned food, you also buy gold. The acquisition of almost 400 tons of precious metals by central banks in the third quarter, which is three times more than in the same period last year, indicates that they hope for the best but are preparing for the worst. Regulators acted aggressively, buying gold on the decline of XAUUSD quotes and showing the whole world what its true value is. As a result, what should have happened happened—the precious metal returned above $1,700 per ounce.

Dynamics of gold purchases by central banks

Its November rally is based on several drivers at once. First, the presumed Republican victory in the US midterm elections. If the Democrats lose control of Congress, then in 2023, when the recession hits the American economy, we should not expect large-scale fiscal stimulus to support growth. The US will look no better than all other countries, and the loss of American exceptionalism will deprive the dollar of an important trump card.

Second, the rise in global risk appetite. History shows that in the first 12 months after the midterm elections, US stocks performed the best in any 4-year term of any president since World War II.

And third, no matter how much optimists would like to think otherwise, the recession is approaching. Its imminent arrival is evidenced by the fact that the yield curve in the US is in the 40-year bottom area. The more it hurts the American economy from the tightening of the Fed's monetary policy, the lower the yield on Treasury bonds will fall. The slower the Fed will tighten monetary policy, which will negatively affect the dollar. The gradual decrease in its share in the gold and foreign exchange reserves of central banks is another argument in favor of the latter buying the precious metal.

Dynamics of the share of the US dollar in the gold and foreign exchange reserves of central banks

Of course, the 5.7% rally in XAUUSD over three days could not have happened without an avalanche-like closing of speculative short positions in gold, which, by the beginning of November, were close to their September peaks.

Whatever it was, the Fed pulled the trigger, announcing the slowdown in monetary restrictions. While gold initially reacted with a decline, the subsequent rally proved that when the monetary tightening cycle matures, the precious metal usually begins to spread its wings, taking advantage of dollar weakness and falling US Treasury yields.

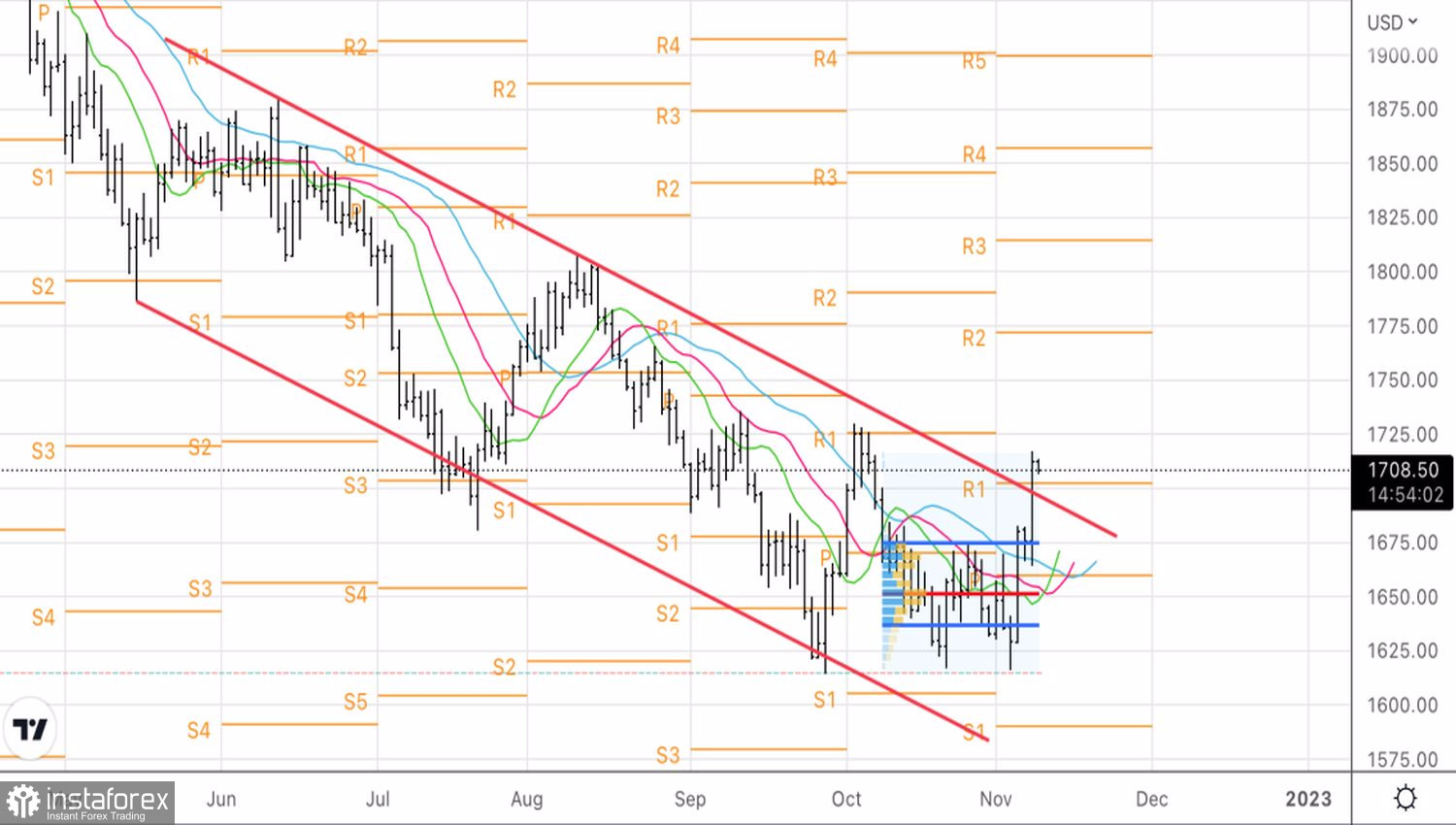

Technically, on the gold's daily chart, several signs indicate a change in the "bearish" trend. This is the triple bottom pattern, the rapid exit of the precious metal beyond the fair value range, a successful test of dynamic resistances in the form of moving averages, and a breakout of the upper boundary of the descending long-term trading channel. In such conditions, gold should be bought on the rebound from the supports at $1,702 and $1,692 per ounce.