English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Risk appetite fell sharply after China released weak activity data for July. Oil prices have also fallen to a low since February, while demand for safe assets, such as dollar, increased.

NZD/USD

The Reserve Bank of New Zealand will have a meeting on Wednesday, during which the interest rate is expected to be raised by 0.50% to 3%. If inflation and wages exceed expectations, then the rate hike could be as high as 0.75%, the same as what the Federal Reserve did at its last two meetings.

In terms of Treasuries, the yield on 10-year US bonds fell from 3.47% in mid-June to 2.89%, primarily due to the weakening growth prospects, which prompted markets to evaluate the Fed's interest rate cut as early as the middle of next year.

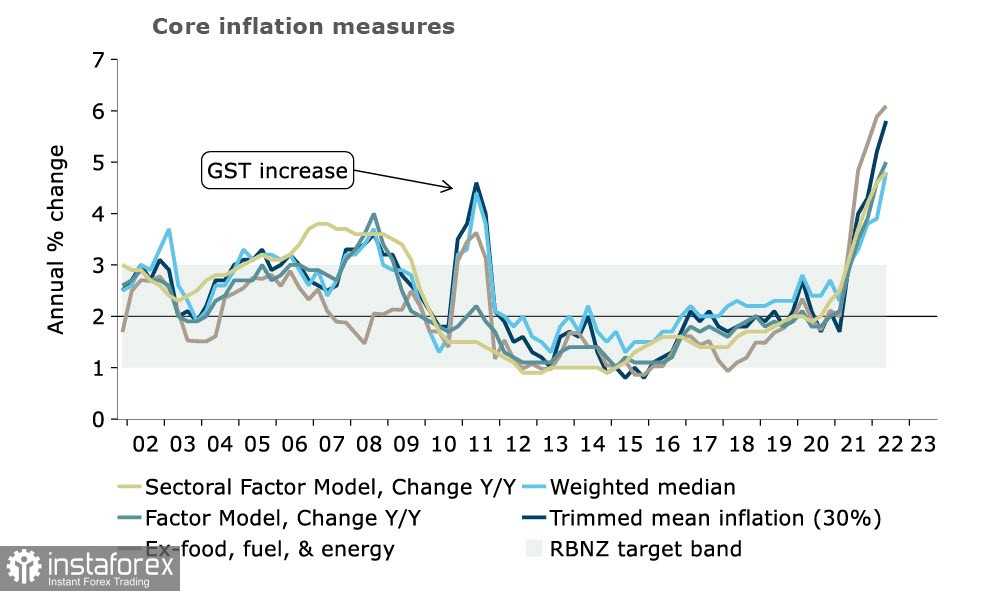

This cannot be said to New Zealand as core inflation pressures continue to rise. The figure is currently hovering between 4.8% and 6.1%, showing no signs of slowing down.

This only means that the fight against inflation is far from over, especially since rapid wage growth is a significant source of risk.

Although the 7.0% increase in the private sector is good news for households, for the RBNZ this means the rate may not be as restrictive as previously thought. It implies that the rate may need to rise above 4% to reduce domestic inflationary pressures.

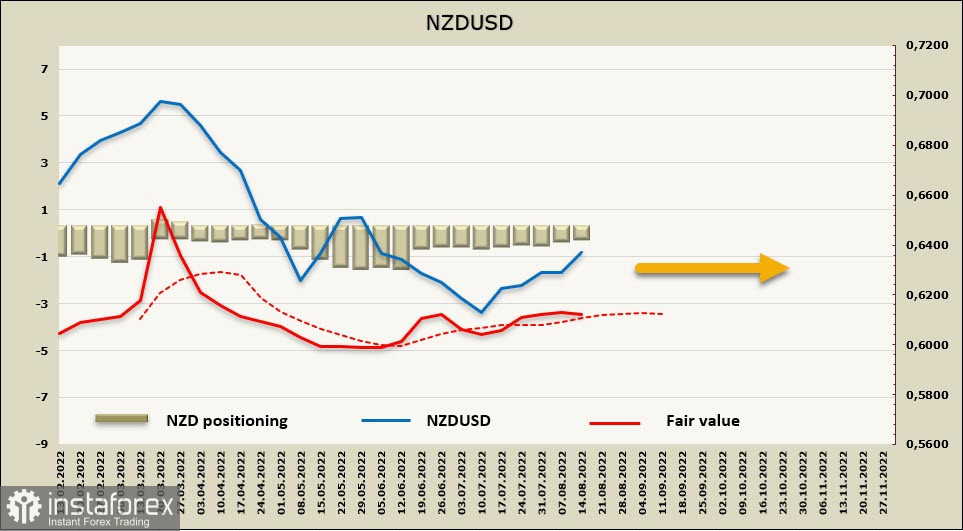

Talking about the NZD positioning, the weekly CFTC report indicates that it is still close to neutral, with net short position falling by 81 million over the week to -17 million. The bearish margin is minimal, while the settlement price is close to the long-term average.

A week earlier, NZD/USD was expected to move to the resistance area of 0.6380/90, but the bulls managed to push it higher. Now, the momentum is weakening, which raises doubts for further price increases.

The pair is also in a long-term bearish channel, and there are no signs of a bullish reversal. This means that the most likely scenario for the coming week is range trading, where quotes will go to 0.6570/90 if the RBNZ takes an aggressive approach to its monetary policy.

If the RBNZ focuses on factors pointing to a slowdown in inflation, then the pair will trade slightly lower and move towards 0.6190/6210.

AUD/USD

The National Australia Bank lowered its short-term growth forecasts. They said consumption is slowing down, while inflationary risks remain high, which holds back GDP growth. They also expect inflation to peak at 7.5% in Q4, then gradually decline to 3% in 2023.

In terms of interest rates, the Reserve Bank of Australia said it could increase by 0.50% in September, then rise again by 0.25% in October and November. If inflation shows signs of slowing down, then the rate will be at 2.85% by the end of the year.

The yield spread will depend heavily on how much inflation will be in Australia and the US by the end of the year. So far, the situation does not look because with a lower rate, it is likely that inflation in Australia will be higher or approximately at the same level as the US.

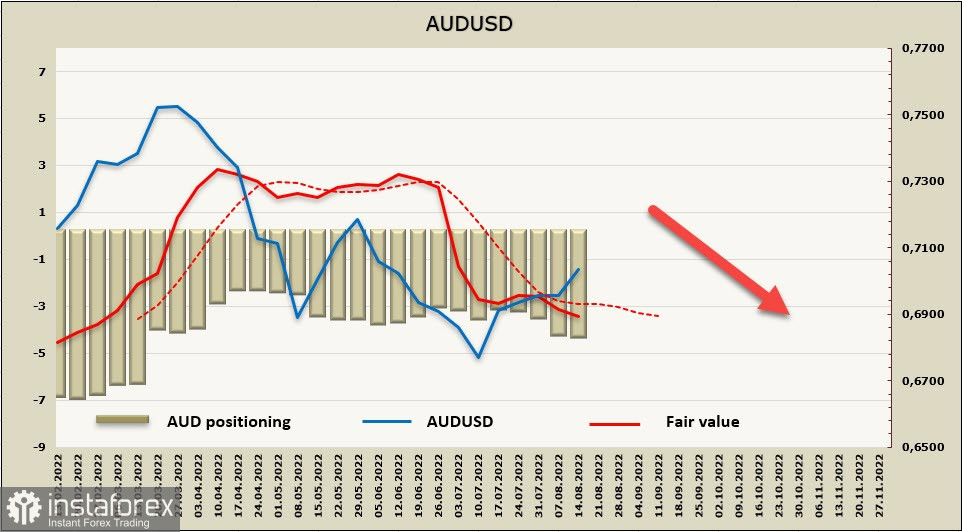

Talking about the AUD positioning, the weekly CFTC report indicates that net short positions increased by 140 million to -4.012 billion. The bearish edge is still significant, and there is practically no reason to expect growth. The settlement price is also below the long-term average and continues to be directed downwards.

A week earlier, AUD/USD was expected to move to the support area of 0.6860/70, but it did not happen. Despite that, nothing has changed in the long term, and the pair remains on the downside. But if the RBNZ shows a hawkish bias today, then a rise to 0.7175 is possible. A slightly more likely scenario is that the local peak at 0.7138 has already been formed and the decline will resume. Long term target is still 0.6464.