English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The Bank of England presented an unusually apocalyptic economic forecast in its quarterly economic review last week, overshadowing the largest interest rate hike in more than a quarter of a century. Nevertheless, the UK markets barely budged. Traders consider the BoE's forecasts useless, given the financial expenses that come from who will become the next prime minister.

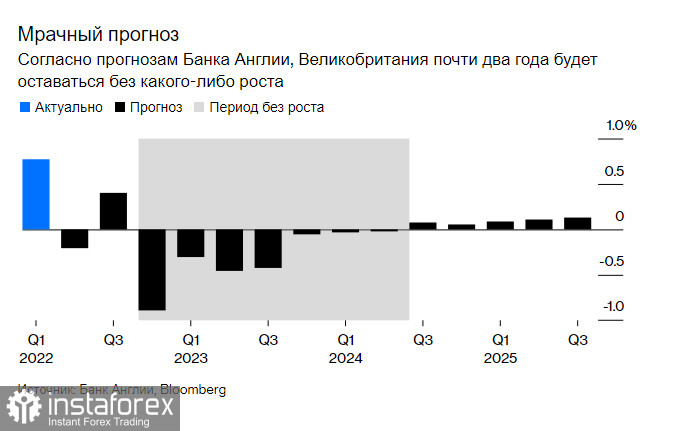

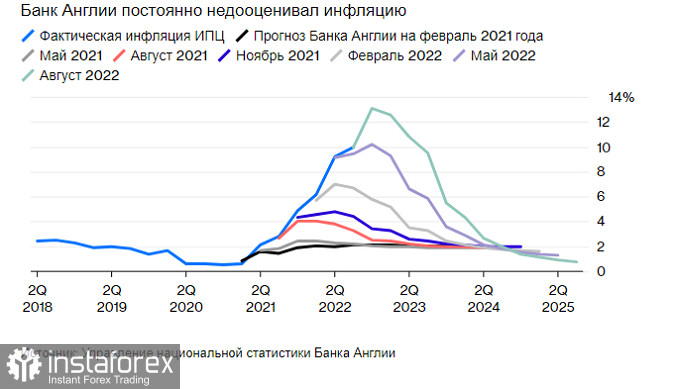

The BoE now expects inflation to peak at 13.3% this year, with annual price growth still close to 10% a year from now. The real shock, however, is its forecast of a prolonged recession, in which growth is not expected for almost two years, and the overall decline in gross domestic product will be more than 2%. Unemployment is expected to rise by two-thirds from the current level of 3.8%.

The BoE repeated the actions of its colleagues from the Federal Reserve and the European Central Bank, canceling forward-looking recommendations. Instead of determining market expectations regarding the future path of interest rate changes, decisions will be made at each meeting. This hardly inspires confidence in the ability of politicians to predict economic prospects, and also risks increasing market volatility in the coming months.

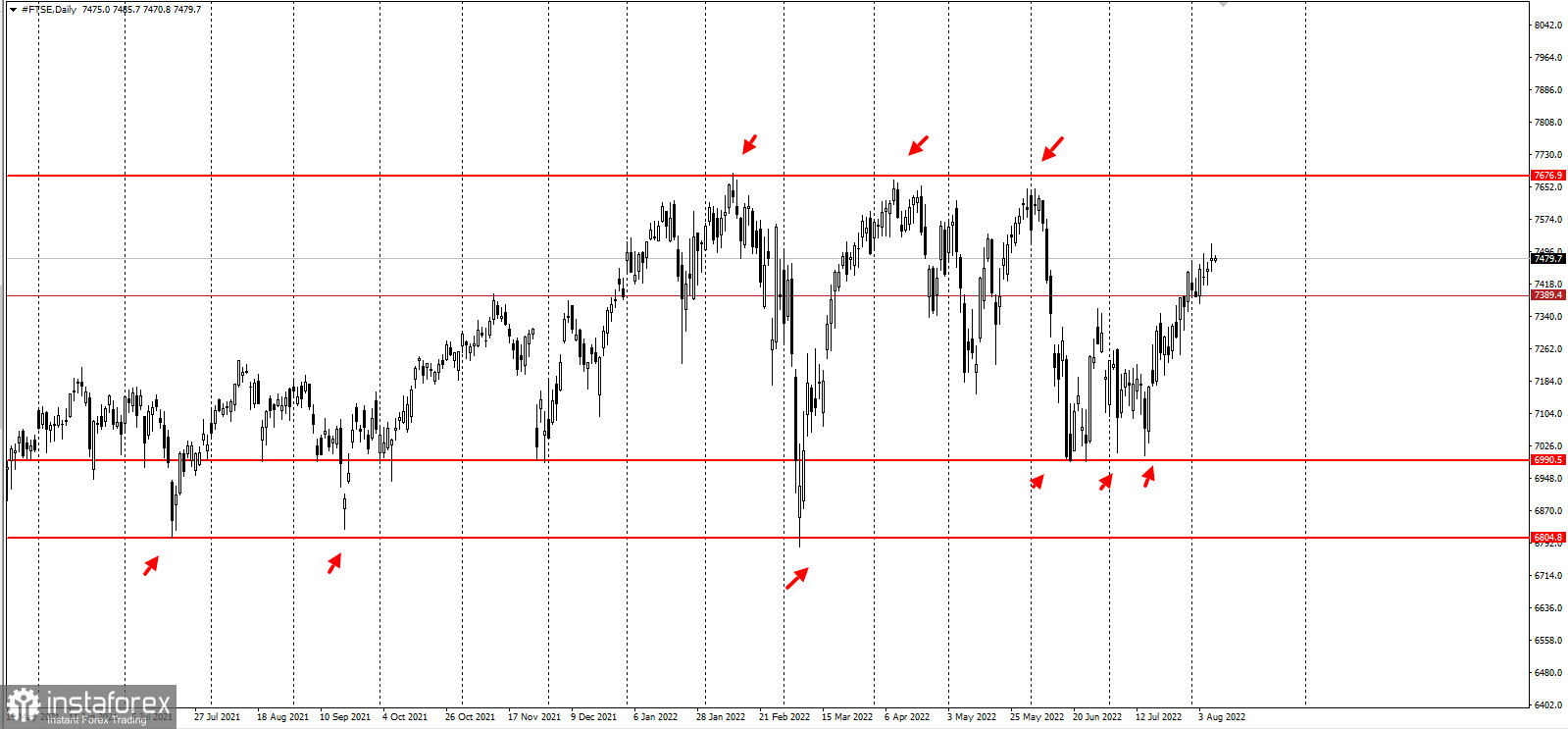

The British FTSE stock index has a very sluggish bullish trend with a huge potential for attacking targets below:

The crucial disadvantage is that the BoE's forecasts cannot take into account any tax cuts that are not yet official government policy. So while Liz Truss, the candidate to succeed Boris Johnson as prime minister, has promised an immediate financial bailout of around 40 billion pounds ($49 billion), and rival candidate Rishi Sunak also promises to shake the magic money tree, this supposed generosity does not figure in the central bank's models.

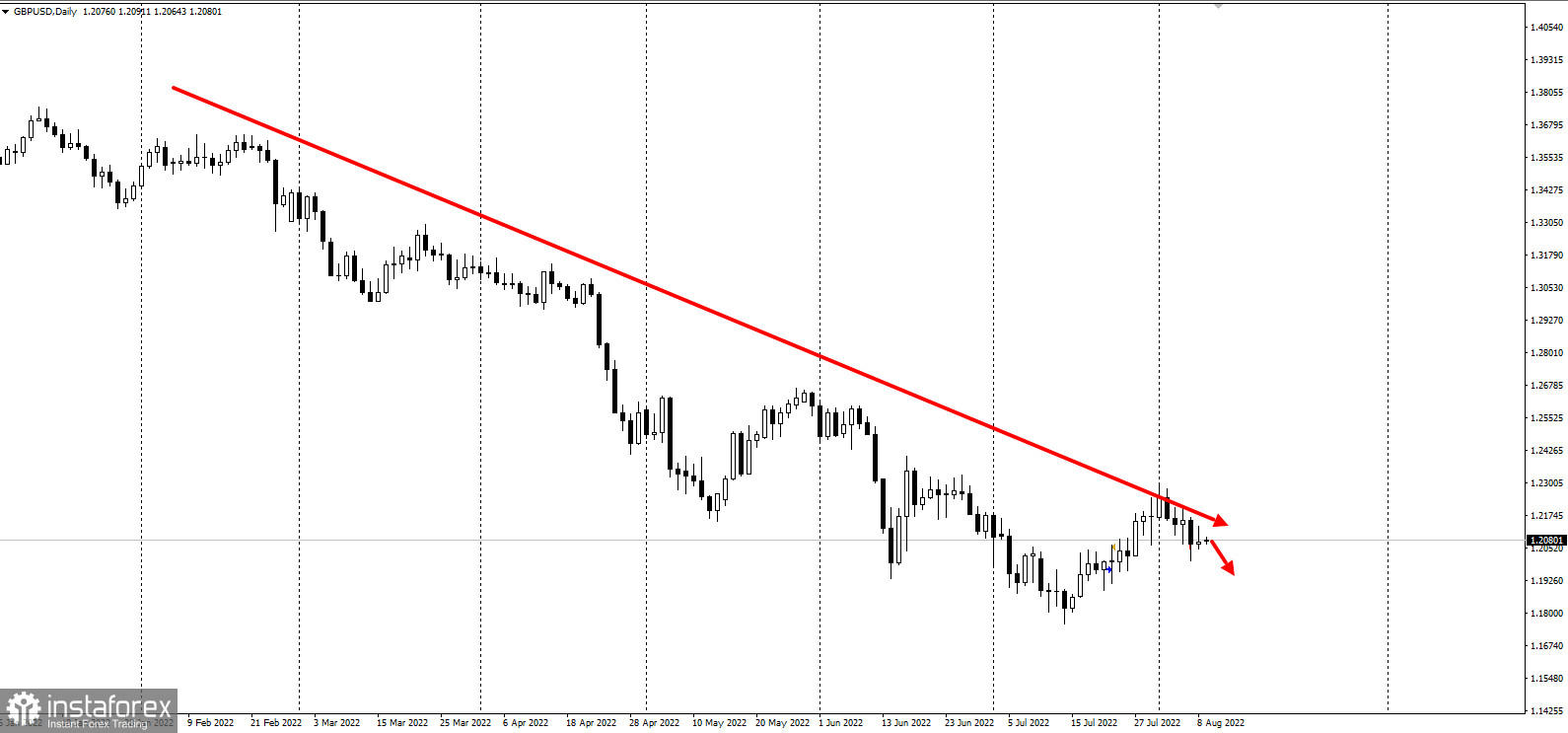

The GBPUSD pair continues to be in a pronounced short trend with good prospects for further decline:

BoE Governor Andrew Bailey refused to answer any questions that concerned the political arena. But with the BoE's own forecasts showing inflation at almost seven times its strict 2% target, relations between the UK government and its central bank are likely to fall on hard times. "The bank may be politically independent, but it is not independent of politics," commented Simon French, chief economist at Panmure Gordon.

Truss has repeatedly stressed that the mandate of the BoE will be reviewed during her administration. Having such a prescriptive goal has become an obstacle for the central bank, and, within reason, it should welcome the changes.

At the moment, the markets interpreted last week's rate hike as a dovish increase. Given that the BoE forecasts an inflation rate of 0.8% by the end of its three-year forecast horizon, raising the cost of borrowing much higher in a recession seems unwise. Two or three quarter-point increases will cause the official interest rate to peak at about 2.5% by the end of the year, at which point policymakers may want to pause to assess how the economy is developing in light of both fiscal stimulus and monetary tightening.

Last week, the BoE needed to send a message about a reduction in inflation expectations, hence the excessive rate hike. Traders have come to the conclusion that politicians have no particular idea of what will happen next for the economy. As the bank tries to communicate its political intentions in the coming months, it needs to be careful not to give too much heat but not enough light.