English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Size matters. On the eve of the June meeting of the Bank of England, investors are almost certain that it will raise the repo rate for the fifth consecutive time to levels not seen since 2009. The market is facing another question, how big will the increase in borrowing costs be? 25 or 50 bps? The first option is fully taken into account in the GBPUSD quotes and, most likely, will lead to a fall in the pair against the backdrop of sales of sterling on the facts and an increase in British dissatisfaction with the policy of the central bank due to record prices for gasoline. The second option will bring a recession in the UK. BoE will have to choose the lesser of two evils.

When four acts of monetary restriction did not lead to a slowdown in inflation, and at the previous meeting, three out of nine members of the MPC voted for raising the repo rate not to 1% as the majority, but to 1.25%, it is difficult to expect the Bank of England to stop. On the contrary, it has several reasons at once to speed up its pace.

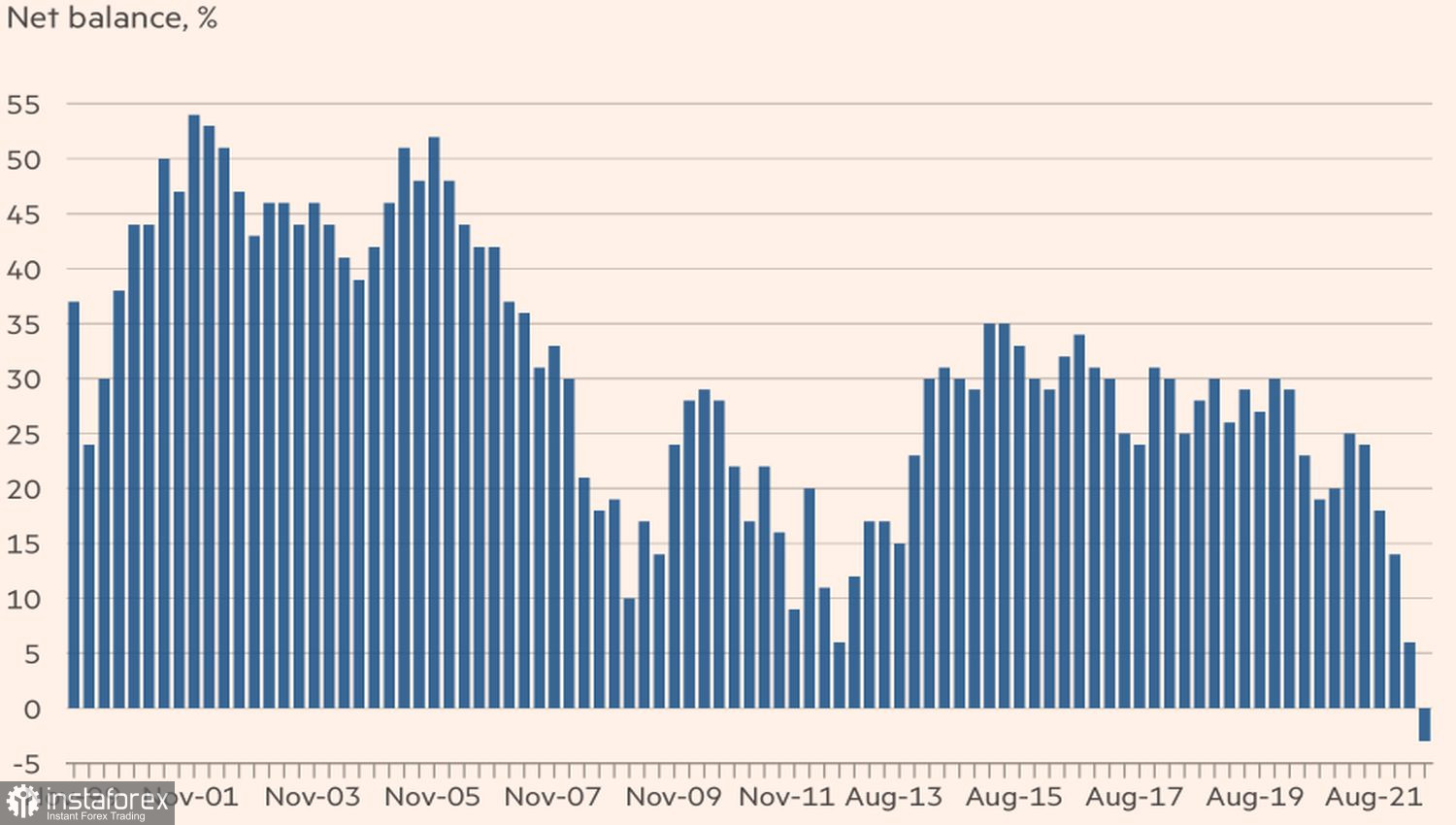

First, a new £15bn fiscal stimulus package from the Treasury to smooth out the worst cost-of-living crisis is likely to be inflationary. It could lead to a further acceleration of consumer prices, necessitating aggressive tightening of monetary policy. Secondly, it is always easier to act with a crowd. When the Fed, the central banks of New Zealand, Canada, and other countries raise rates by 50 bps, why shouldn't the BoE follow the same path? Finally, the dissatisfaction of the electorate with the way the Bank of England is coping with its tasks has reached a historical maximum. The policy needs to be changed, why not do it already in June?

Dynamics of British satisfaction with the activities of the Bank of England

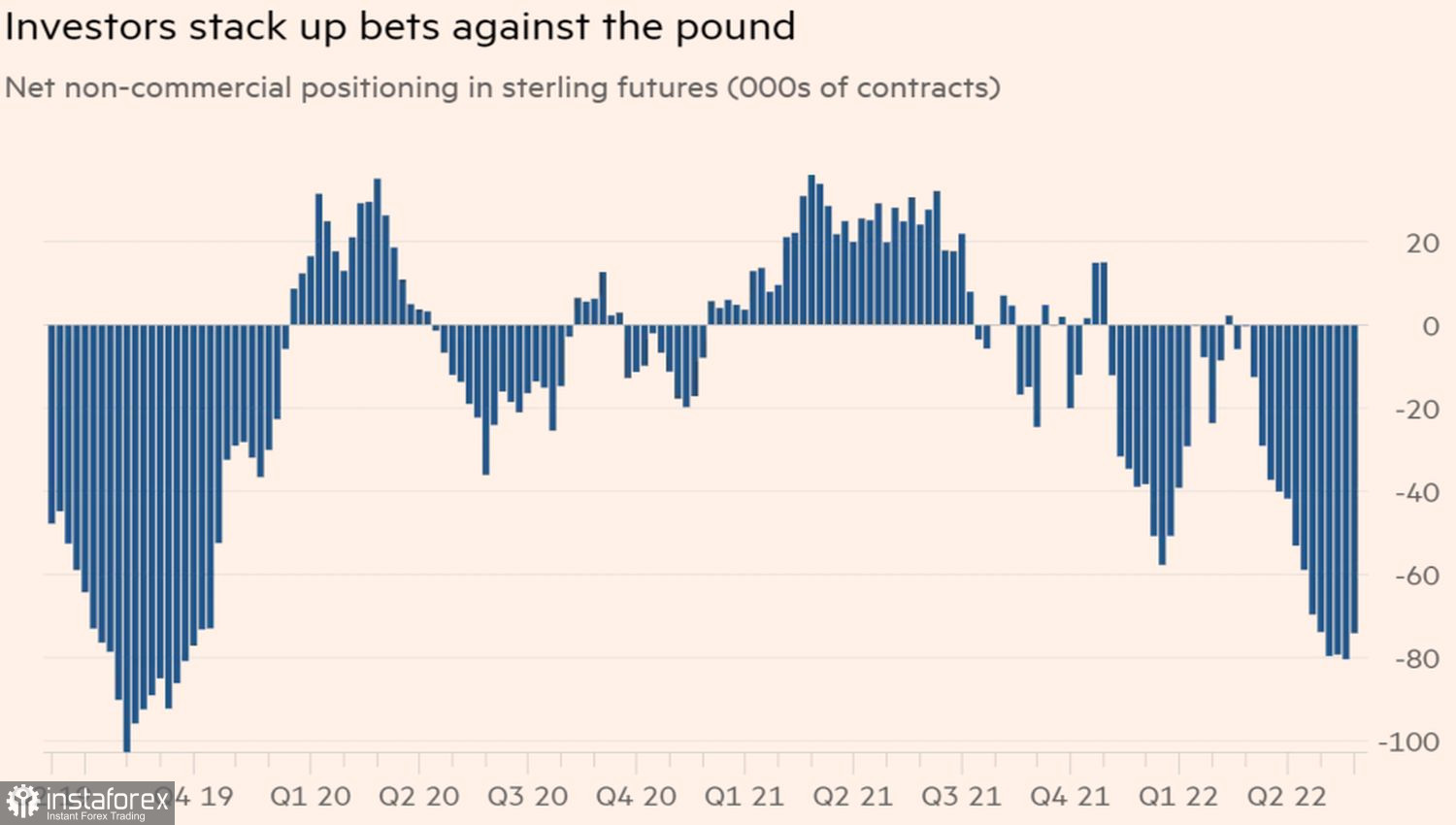

On the other hand, how not to overdo it! According to the World Bank, the economy of the UK in 2022–2023 will show the worst results among the G20 countries, with the exception of Russia. Even if inflation slows in the rest of the world, it is likely to accelerate in Britain in the autumn. This state is closest to stagflation, is it possible to buy a pound in such conditions? Hedge funds think not, and bring their speculative net shorts to their highest levels in three years.

Dynamics of speculative positions on sterling

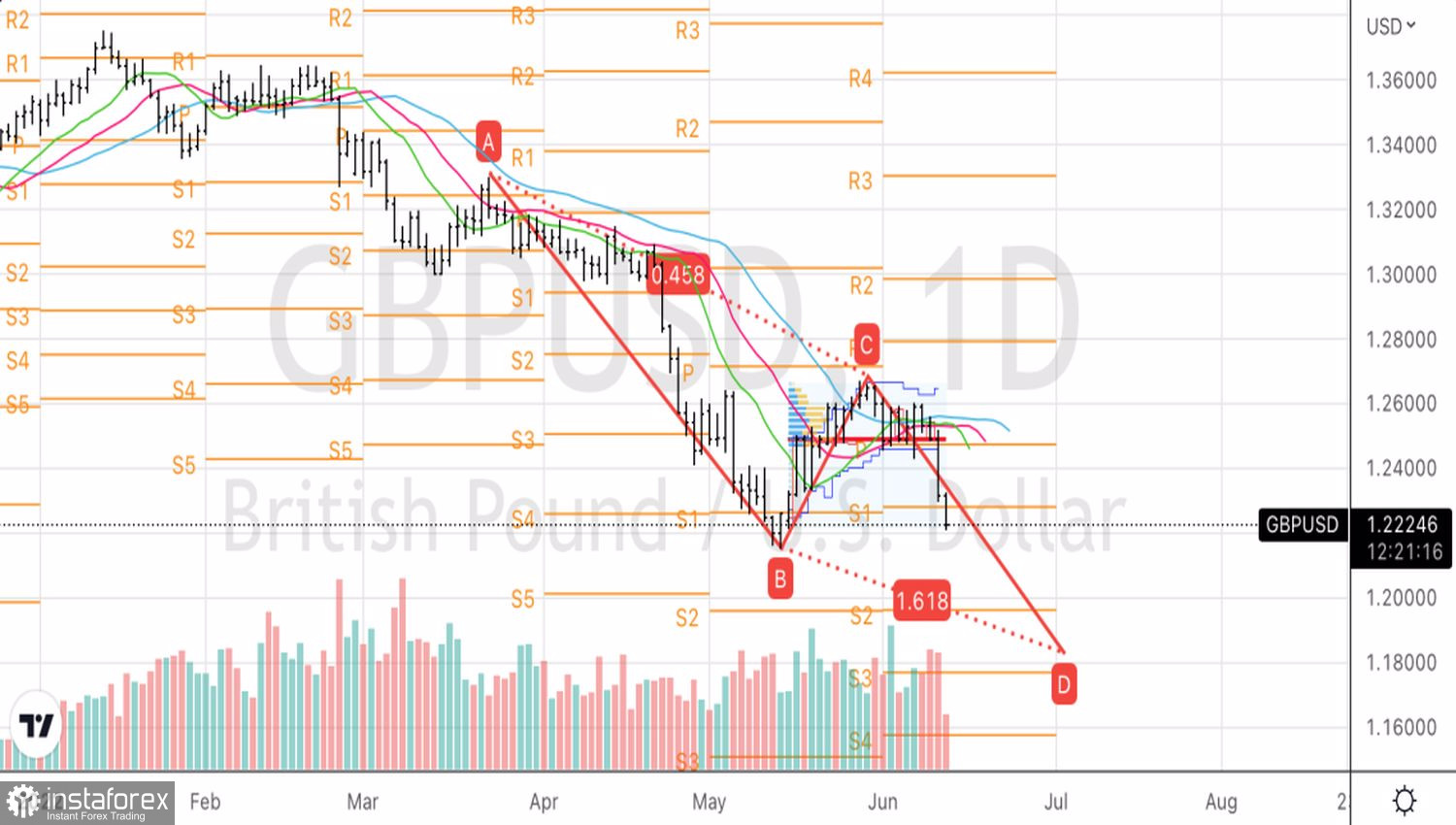

There are always two currencies in any pair. And the fall of the GBPUSD to the very bottom since the end of spring 2020 is largely due to the sharp strengthening of the dollar against the backdrop of an unexpected acceleration of US inflation to 8.6% in May. If investors are arguing whether the Bank of England will raise rates by 50 bps, then with regard to the Fed, we are talking about as much as 75 bps at one meeting.

GBPUSD, Daily chart

Technically, the update of the May low will indicate the recovery of the downward trend for GBPUSD and simultaneously activates the harmonic AB=CD pattern. Its target of 161.8% is located near the 1.183 mark. If in the coming days the pair manages to gain a foothold below the accumulation of pivot points 1.226–1.228, it should definitely be sold against the background of the complete dominance of the "bears."