English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The aggressive tightening of the Fed's monetary policy, the armed conflict in Ukraine, the slowdown in the Chinese economy due to the largest outbreak of COVID-19 since the beginning of the pandemic, and the energy crisis—all these events suggest another recession in the global economy. Investors tend to remember the recent past. In particular, the collapses of Brent during the recessions of 2008–2009 and 2020. This circumstance deters buyers of the North Sea variety. However, firstly, the recession has not yet arrived. And secondly, it can be much softer than the previous two.

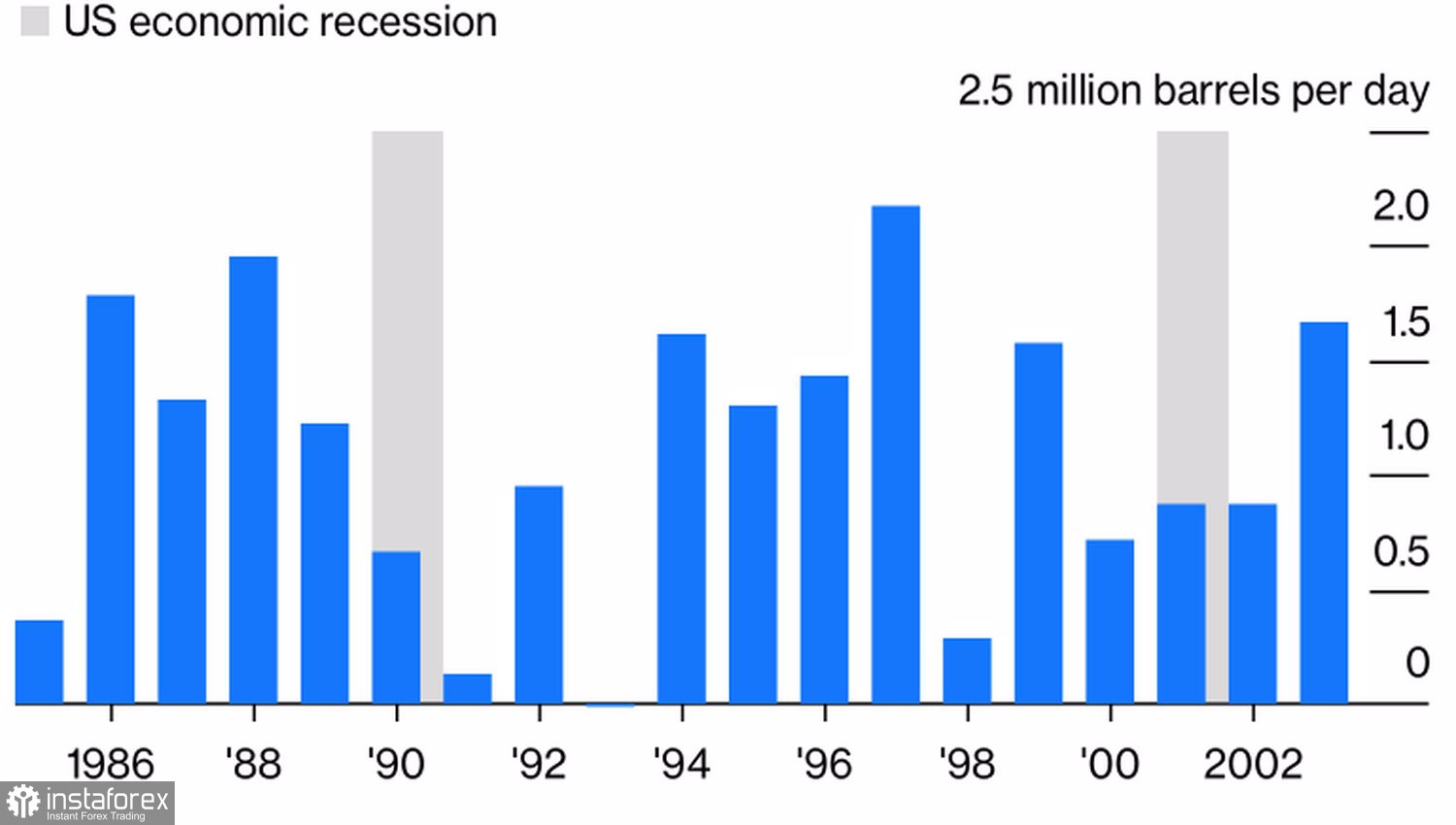

If in 2020, due to the pandemic and lockdowns, the demand for oil collapsed by a whopping 10 million bpd, then in 2008 it fell by 1 million bpd, and in 2009 by another 1.1 million bpd. At that time, the financial world had not seen a fall in the indicator for two years in a row for a quarter of a century, so the collapse of Brent looked logical. The recessions of 1990–1991 and 2001 were very different. Growth in global oil demand has slowed but never abated.

Dynamics of global oil demand

Most likely, a new recession, if it does happen, will be similar to the events of 20 and 30 years ago. In this regard, one should not count on a rapid collapse of the North Sea variety. It clearly has a floor, even though the US Energy Information Administration forecasts shale oil production in the Permian Basin in Texas to rise to a record 5.2 million bpd in June. According to Saudi Arabia, due to a lack of production capacity, an increase in oil production is unlikely to lead to a fall in gasoline and diesel prices. That is, it will ease inflation and the cost-of-living crisis.

The sale of strategic reserves by the United States does not really help the "bears" on Brent. Their value fell to 538 million barrels, the lowest value since 1987. If earlier, sellers were inspired to exploits by China with its 7-week isolation in Shanghai, then the gradual improvement of the epidemiological situation in the country and its intention to gradually exit lockdowns deprive the bears of North Sea variety of the main trump card.

But their opponents are doing much better. According to the IEF research, due to Western sanctions, oil production in Russia decreased by 900,000 bpd in April and will fall by another 600,000 bpd in May. If the European Union nevertheless convinces Hungary not to put a spoke in its wheels and joins the embargo on black gold from the Russian Federation, then the losses may increase to 3 million bpd from July. The exclusion of Russia from the oil market continues, which leads to the expansion of the spread on futures contracts within the backwardation to $2. At the end of April, it was about less than $0.5.

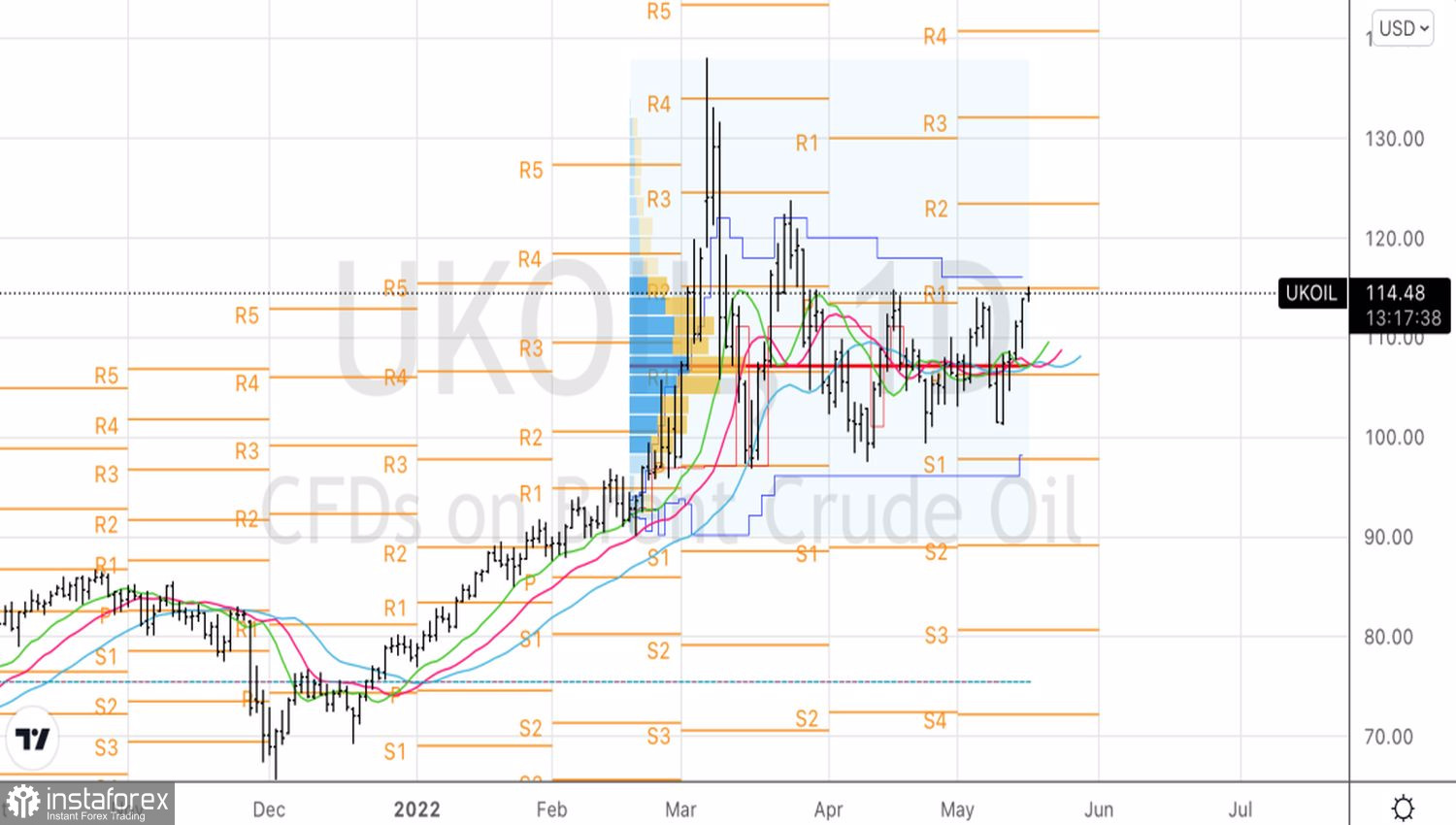

Technically, on the daily chart of the North Sea variety, there is a "Splash and shelf" pattern. At the same time, a break of resistance at $115 (the upper limit of the "shelf") and $116.5 (the upper limit of the fair value) may become a basis for buying. A successful assault on these levels will increase the risks of a continuation of the Brent rally to $118.5 and $123.5 per barrel. On the contrary, a rebound from resistance will allow us to talk about the preservation of consolidation and give grounds for sales.

Brent, Daily chart