English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Markets continue to be dominated by rapid growth in US yields, with 10-year UST approaching close to 3%, which contributes to a steady increase in demand for the dollar. Assumptions began to be voiced that the Fed may raise rates not by 50 but by 75 points at its June meeting, and rate futures show a 39% probability of just such a move as of Wednesday morning.

Dynamics in favor of the US dollar.

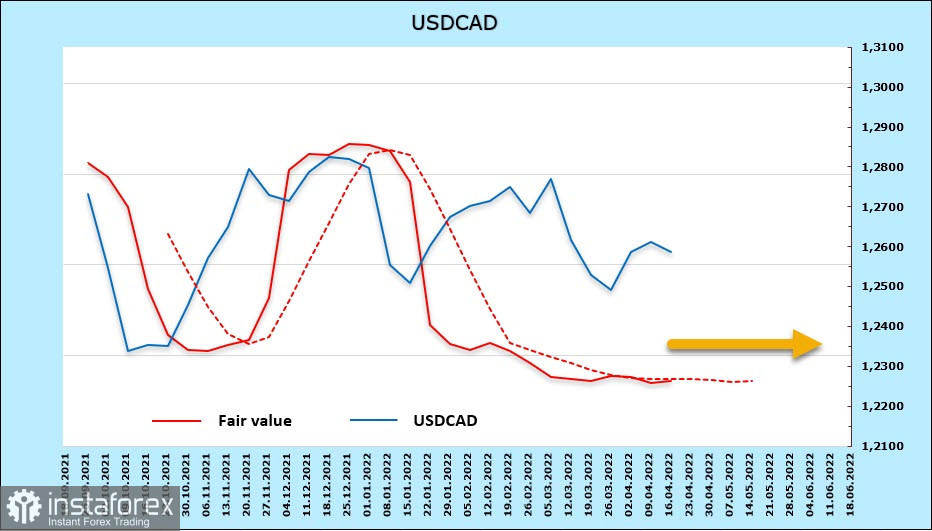

USDCAD

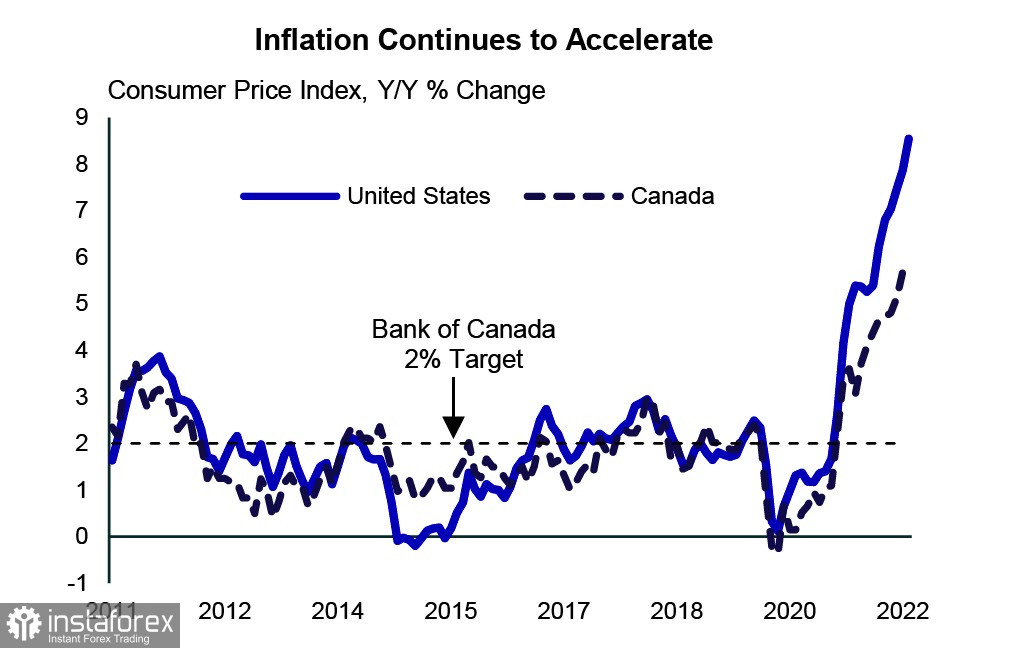

The Bank of Canada, as predicted, raised the rate by 0.5% for the first time in 22 years, also announcing the beginning of quantitative tightening (QT) on April 25, which will eventually lead to a reduction in the balance sheet. The accompanying statement was hawkish, it is expected that at the meeting on June 1, the rate will be raised by another 0.5%, and by the end of the year, it will be brought to at least 2%.

The GDP forecast remains positive despite global risks. The BoC expects real GDP at 4.2% this year and 3.2% next. As for inflation, the forecast has been revised upwards, and data for March is expected at 6.1% YoY, which is less than in the US, but the trend is obvious.

Higher interest rates will make borrowing and servicing accumulated debt more expensive, but this is a problem that all major economies will face except Japan, where efforts to keep yields below the target continue.

The net long position in CAD, as follows from the CFTC report, increased during the reporting week by 407 million, to 962 million. The excess is not expressed. Moreover, the dynamics of UST yield growth outpaces the growth of yields in Canada, which levels out the advantage in futures.

The Canadian dollar has been trading in a range for several months now, its exit is not yet ripe. Given the tightening of the position of the Bank of Canada and the growing likelihood of a continuation of the price rally, a movement to a local minimum of 1.24 looks more likely.

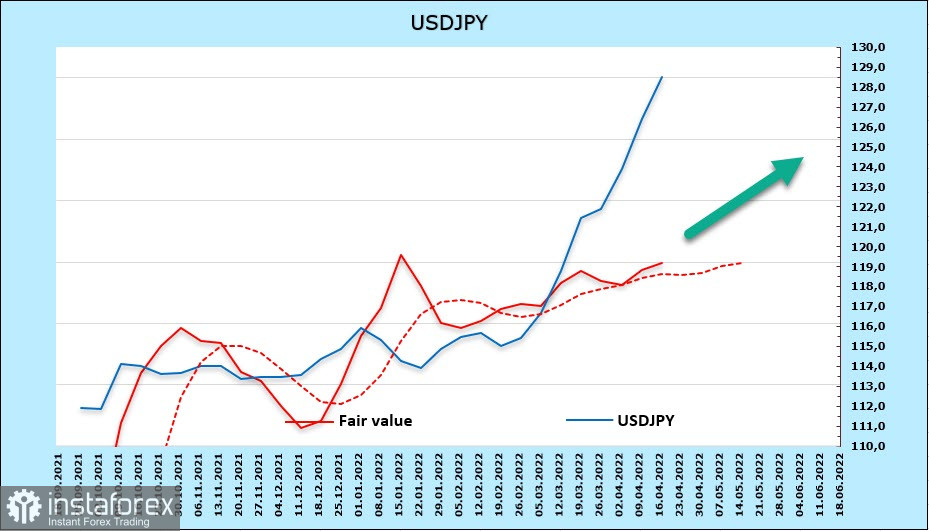

USD/JPY

The Japanese yen is rapidly depreciating as the Bank of Japan is the only bank in the major economies that is focused not on fighting global inflation, but on curbing profitability. Again and again, the BoJ buys bonds at a fixed price as soon as the 10-year yield approaches the 2.5% target, which leads to additional liquidity in the market. The Fed announces a decrease in available liquidity and an increase in the cost of financial services, while the Bank of Japan announces the preservation of financial policy.

As a result, the yen went to a 20-year low. The monetary policy of the BoJ will undoubtedly change, because if it is maintained, then by the summer it will be possible to see the rate of 140 and above, but this will not happen in the near future.

Prime Minister Fumio Kishida told the Upper House plenary meeting on April 15 that "the Bank of Japan (BOJ) is conducting monetary policy to achieve its 2% inflation target, not to manipulate currency rates."

BoJ Governor Haruhiko Kuroda said that "we need to take into account the negative effect" of the weak yen but stresses that he hasn't changed his mind that a weaker yen is a positive factor for the economy as a whole.

Thus, we must proceed from the fact that there are no objective factors for the strengthening of the yen.

The net short position on the yen rose by 648 million in the reporting week, a bearish margin of -11.149 billion. Speculators continue to bet on the weakening of the yen.

The bullish momentum has not yet been exhausted, with the January 2002 high at 135.19 now the main target. Even 3 months ago, such an assumption would have been absolute fantasy.