English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The longer the military operation in Ukraine lasts, the more likely it is to see the European Union join the US-British embargo on Russian oil. If so, then the IEA's forecast of a 3 million bpd reduction in the supply of oil due to sanctions against Moscow may become a reality, which supports the Brent bulls.

The North Sea variety has been growing for several days on fears that Germany and Hungary will soon stop resisting the idea of a ban on Russian oil imports, and the EU is finally implementing plans for an embargo. According to Moscow, this would be a real disaster for the entire oil market, and especially for Europe. The Americans would be able to cope, but the Europeans would begin to live much worse, their economy would face a recession. Russia claims that substantial discounts on Urals, which has traded at an average of $95 a barrel since the start of the armed conflict, allow it to find buyers. If they are not in Europe, the black gold exporting country will transfer barrels to the Asia-Pacific region.

In fact, of the 4.4 million bpd that Russia exported from March 1 to March 15, 2.7 million b/d went west via pipelines across the Baltic and Black Seas. The rest - to China and other countries in the East.

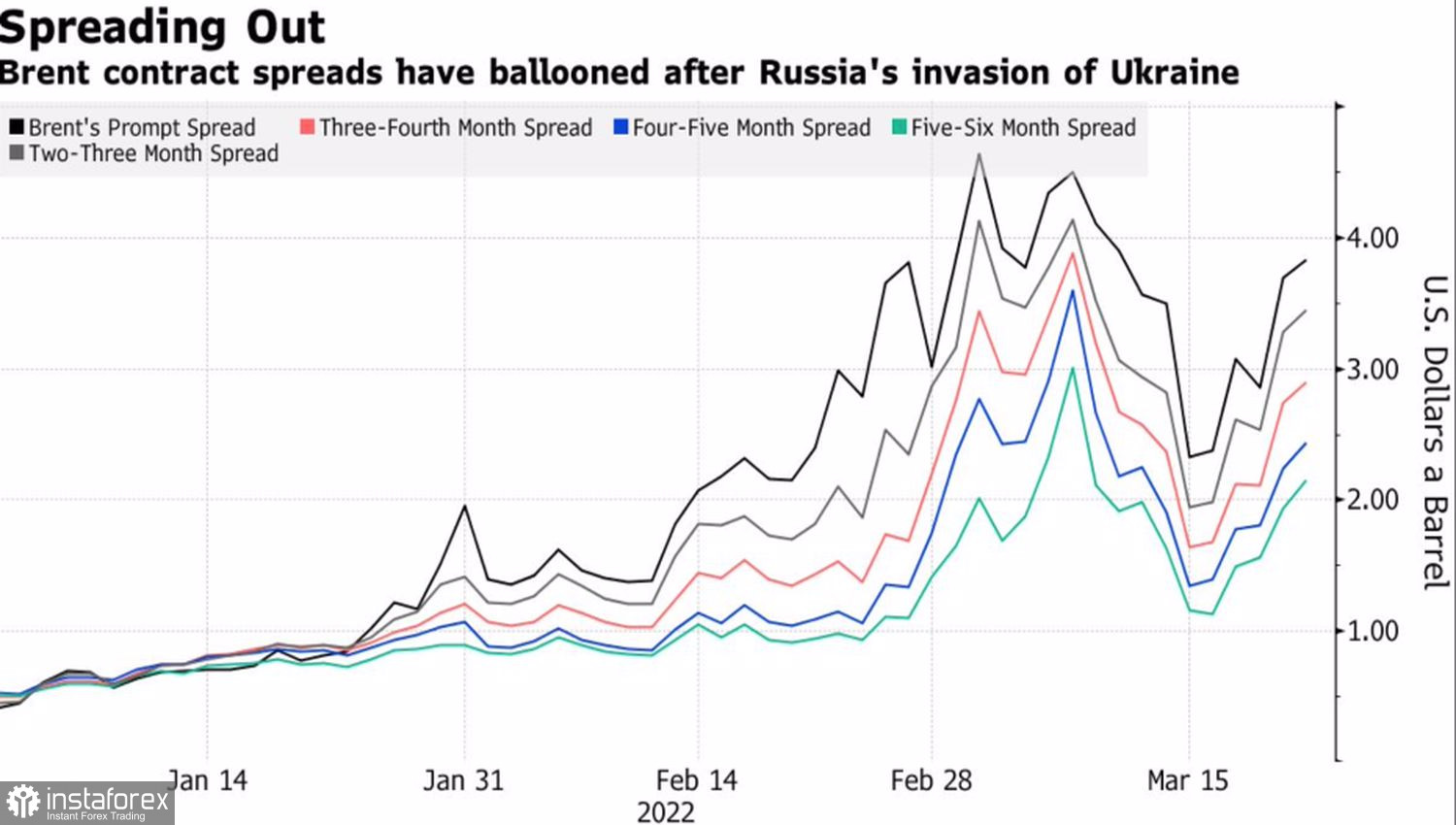

It should be noted that the supply shock is not only related to a possible EU embargo on Russian oil. An attack by Iranian-backed Houthi militants on an oil structure in Saudi Arabia is reducing the production and export of oil from that country. In addition, according to JBC Energy estimates, the difference between planned and actual production from OPEC+ in February was 800,000 bpd, and in March it will increase to 1.15 million bpd. This will contribute to the development of backwardation in the oil market and the growth of Brent quotes.

Backwardation dynamics in the oil market

Of course, rumors about the EU joining the US-British embargo on Russian oil excite the market and push the price of black gold up, but it must be admitted that investors are fixated on bullish news and completely ignore bearish news. For them, it is more important to hear the news about China's readiness to expand monetary stimulus than Rystad Energy's forecast of a potential reduction in global demand by 2 million bpd due to the armed conflict in Ukraine, sanctions against Russia, and inflation.

Let's not forget the historical links between Brent and the U.S. dollar. Assets are moving in the opposite direction, but at present, the Fed's aggressive rate hike, including a possible increase in borrowing costs by 50 bp at once at one of the upcoming FOMC meetings, supports the U.S. currency, but oil is of little concern.

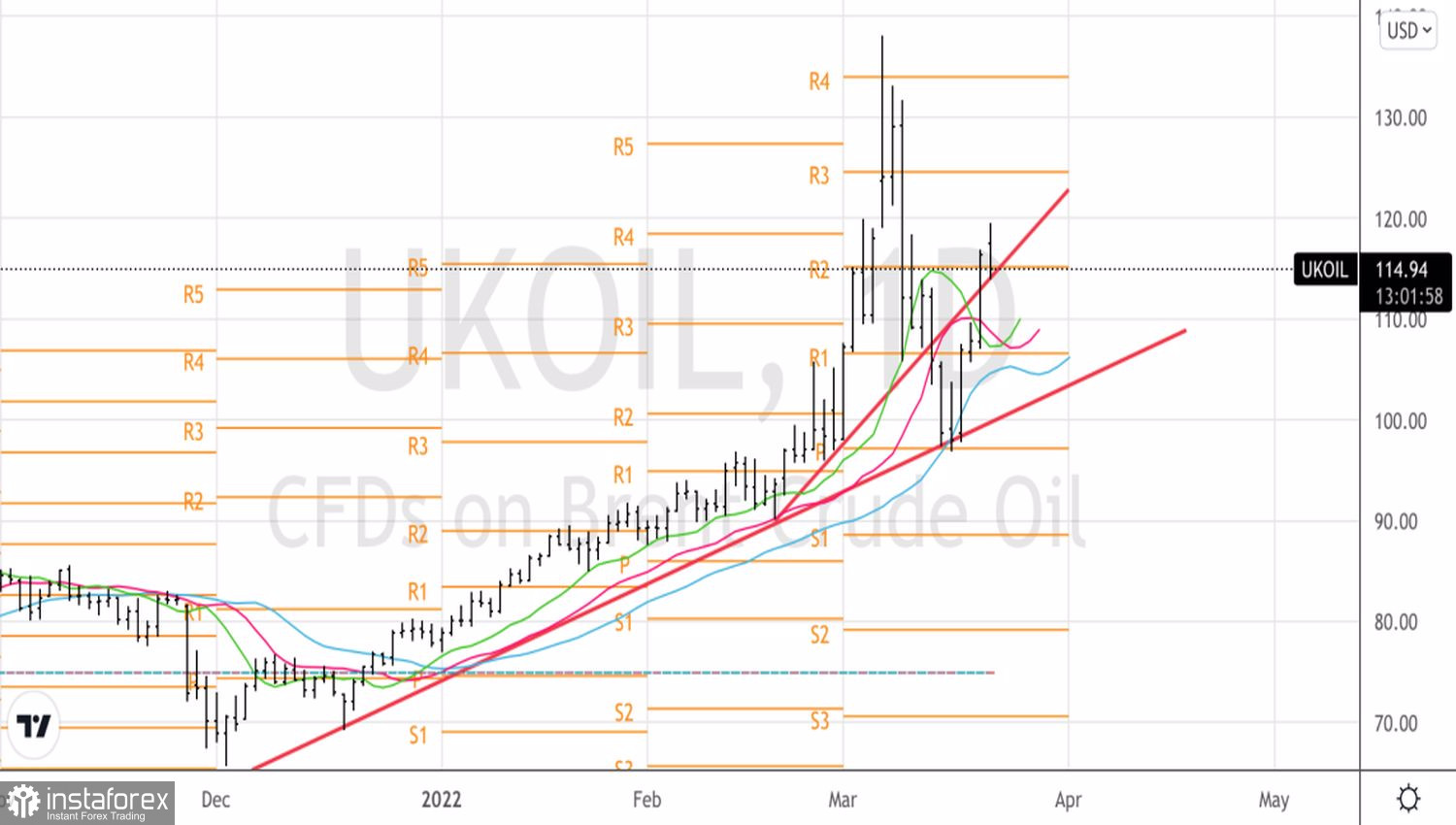

Technically, on the daily chart of the North Sea variety, the Splash and Acceleration Reversal pattern continues to be active. The inability of the Brent bears to storm the Lead-in trend line is evidence of their weakness. If the bulls manage to stay above the splash stage trend line near $115, this will allow the longs formed from the $97-98 per barrel area to increase.

Brent, Daily chart