English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

On Friday morning, risk assets continue to sell-off. The US stocks closed in the red zone yesterday, so there is no doubt that the European one will also start the day with sales. On the contrary, the demand for gold and the yen is growing. Traders are preparing for the Fed meeting

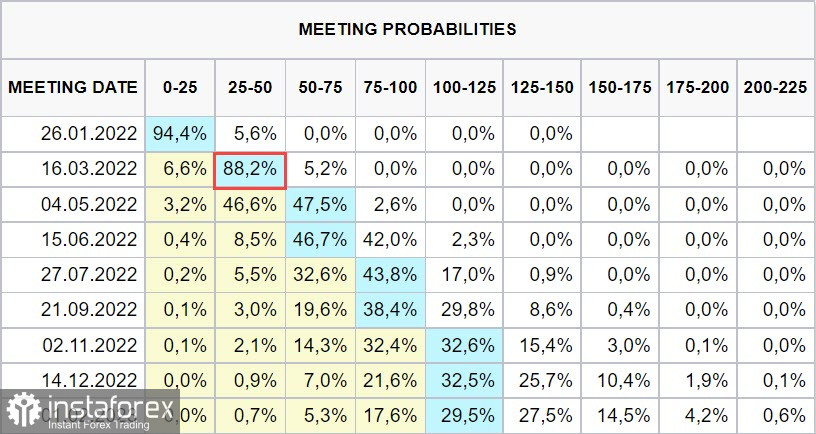

Expectations from the Fed's January meeting are as follows: The US regulator will point out directly that the first rate hike is likely to be implemented as early as March if the economy develops as expected. Both the tight labor market and ultra-high inflation are pushing it to this decision.

The current market consensus is that the Fed will raise rates 4 times this year. There is also a growing belief that there will be 4 hikes next year, and if the US economy recovers as confidently as in recent months, there is a risk that there will be not 4, but 5 increases this year, which means that the Fed will act more aggressively. The CME futures market is convinced that the first increase will be in March.

Now, a real question arises. If the rate is raised aggressively, will it mean a rapid deterioration in financial conditions, which will inevitably push the economy into recession? Yes, there is such a danger. Moreover, many analysts of large banks are already openly talking about it, but the problem is that the Fed simply has no other choice. If inflation is not brought under control (it can be recalled that consumer inflation reached 7% in December, while manufacturing inflation is already confidently double-digit), then this will mean a loss of credibility for the Fed, which, in turn, will lead to a loss of influence on financial markets, and the consequences of this will be much more serious.

In general, the problem facing the Fed looks like this. The US national debt currently stands at approximately $29 trillion. To simplify calculations, let's assume that it is all denominated in 10-year Treasuries, the current yield on which is about 1.8%. It is easy to calculate that just to service the debt with the possibility of constantly updating the debt body. It is necessary to withdraw $520 billion from the US budget annually.

It is not known whether 7% consumer inflation can be offset by 4 rate hikes in 2022, but what is clear is that these hikes will add approximately 1% to 10-year UST yields, which would increase budget spending to $825 billion a year. An increase in rates means a decrease in consumer activity, and a decrease in activity means a decrease in budget revenues, while budget spending is growing rapidly. Another 4 proposed rate hikes in 2023 will raise budget spending on debt servicing to more than $1 trillion.

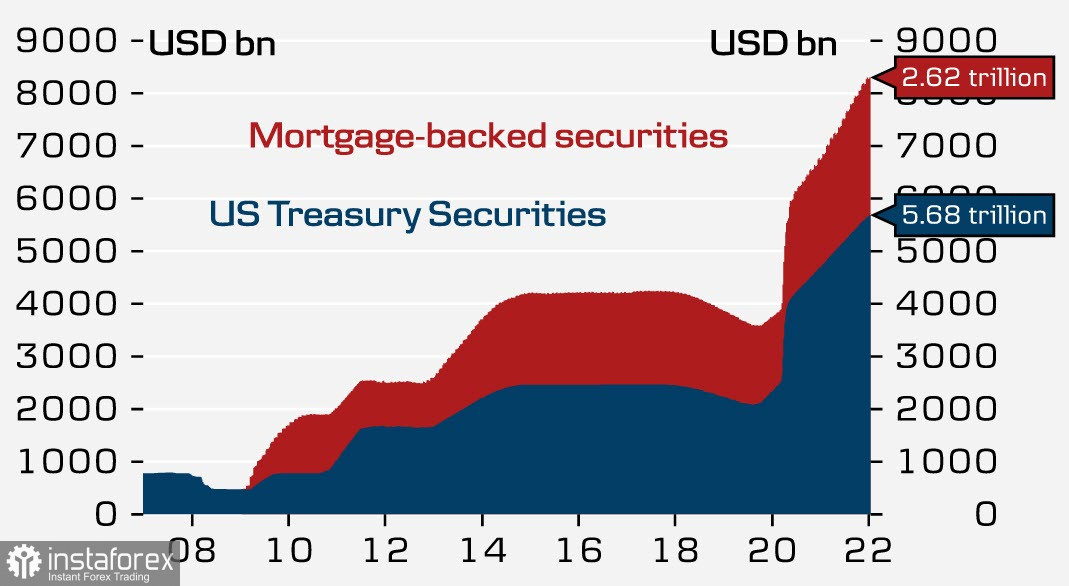

Where should the Fed get additional funds to service the growing debt if financial conditions worsen and the economy slows down? Only through new loans. The US government will place new bond issues that someone has to buy back. Among other things, the Fed intends to announce its intention to begin reducing the balance sheet (quantitative tightening, or QT). Some Fed members have already announced that they would like to see the start of this process as early as possible.

A reduction in the balance sheet will mean that the Fed will not buy back the US government debt, which means that other buyers, that is, Japanese, European, Chinese investors, should buy it.

So, the Fed is faced with the need to curb inflation, and it can do this by provoking a recession in the United States. This is exactly what the Fed's dilemma looks like.

How will the markets react? It is clear that the rate is rising right now, and the recession will come sometime in the future. This means that UST yields will attract new buyers in the short term, which will cause demand for the US dollar.

The growth in demand for the US dollar and the end of QE will mean a large-scale sale of stock markets. As a result, risky assets will decline relative to protective ones. The confident tone of the Fed's accompanying statement will mean the beginning of the process of global repositioning in favor of the US dollar and protective assets, and it is precisely this scenario that Fed officials are apparently preparing investors for.