English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The euro-dollar pair ended the trading week at 1.1315, that is, 100 points higher relative to the opening price on Monday. This is a very modest achievement for EUR/USD bulls, given the fact that during the week the price "walked" within a wide range, the lower limit of which corresponded to the 1.1235 mark, the upper one to the 1.1380 mark. As you can see, neither the bears nor the bulls of the pair were able to develop a downward or upward movement. Traders opened short positions on the upward spikes, and long positions, respectively, on price declines.

As a result, the pair was stuck on the border of 12 and 13 figures, contrary to the hawkish signals of the Federal Reserve members, contradictory Nonfarm and panicked COVID sentiments. Neither bears nor bulls became beneficiaries of the current situation. The fundamental background of the pair is contradictory, and this fact does not allow traders to "unconditionally" accept one side or the other of the confrontation. Take a look at the daily chart: throughout the five-day period, the pair showed increased volatility, as evidenced by the long spires of Japanese candlesticks. But in fact, the pair was marking time, each time returning to the "neutral territory", to the base of the 13th figure. This suggests that market participants need an additional information driver that will unambiguously determine the vector of price movement in the medium term.

The main event of the past week was the unexpected "epiphany" of Fed Chairman Jerome Powell, who announced the growing threat of high inflation. Powell has been repeating the mantra about the temporary nature of the surge in inflation for six months. He assured market participants that the inflationary dynamics was caused only by failures in supply chains, a shortage of goods and a shortage of labor. That is, temporary factors. But speaking in the Senate on Tuesday, Powell unexpectedly admitted that US inflation is long-term. In connection with this "unexpected discovery" (which many experts and some members of the Fed have been talking about for several months), at the December meeting of the Fed, the issue of accelerating the curtailment of the economic stimulus program will be considered.

It should be noted that not only Powell, but also many of his colleagues have tightened their position. In particular, the head of the San Francisco Federal Reserve, Mary Daly, who was previously a consistent dove, said last week that at the moment "there is every reason to accelerate the pace of curtailing the QE asset purchase program." In addition, according to her, the Fed is "most likely" to raise the rate at the end of next year. At the same time, she added that "she would not be surprised if two increases occur within the framework of 2022."

The head of the Federal Reserve Bank of Cleveland, Loretta Mester, in turn, admitted the possibility that the new strain of Covid would worsen supply disruptions and labor shortages and thereby further accelerate US inflation. Given such a scenario, she also supports the idea of early curtailment of QE. Moreover, according to her, next year "at least one or even two rounds of rate increases would be appropriate."

The head of the Federal Reserve Bank of Atlanta, Rafael Bostic, also joined the "hawkish chorus", stating the expediency of early curtailment of the incentive program. In his opinion, this step will untie the central bank's hands on the issue of raising rates next year.

James Bullard, who has long held the most hawkish position among the Fed members, also supported his colleagues at the St. Louis Federal Reserve. Yesterday, he said that the central bank should finish reducing QE by March. This, according to him, will allow it to raise the rate "if necessary." Earlier, he stated that the Fed needs to raise the rate "at least twice" within 2022.

In other words, the Fed has significantly tightened its position ahead of the December meeting. In my opinion, this is a turning point for the US currency. If not for the notorious "Omicron factor", the EUR/USD pair would now be trading around the 10th figure, storming the key support level of 1.1000. But the market, as well as history, does not tolerate the subjunctive mood, so traders are forced to reckon with the new coronavirus threat.

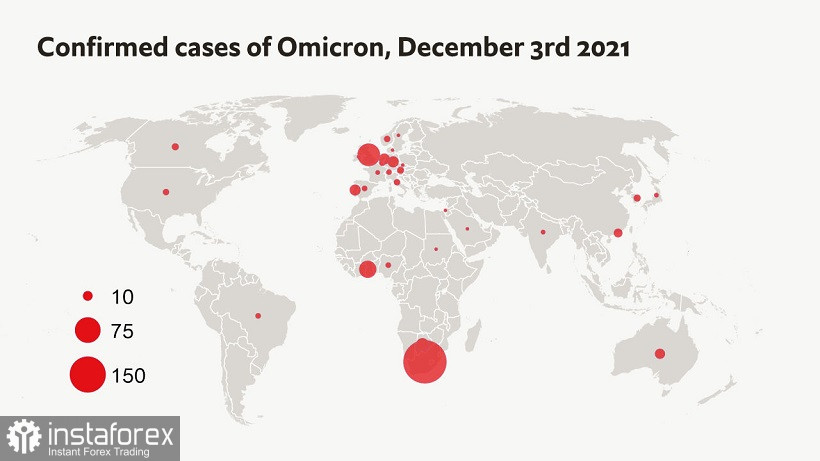

The situation around the new strain remains uncertain. Both optimistic and pessimistic scenarios based on the opinions of individual experts or medical officials are "walking" in the press. The World Health Organization urges not to panic, but at the same time to prepare for the likely spread of a new variant of Covid. To date, it has been found in 30 countries around the world. It is obvious that the number of "infected" countries will grow every day. Against the background of this news, the VIX fear index (which reflects the mood of investors) has grown rapidly, rising by 55% at once, to 30.67 – this is the highest level of the indicator since February of this year.

Uncertainty scares me. The fact is that the resistance of Omicron to the immune response caused by vaccines will be clear in at least two weeks, when it will be possible to determine how many vaccinated and unvaccinated people have become infected with it. In addition, after about two weeks it will become clear how hard people endure the new "modification" of the Covid. On the one hand, doctors from South Africa say that in the vast majority of cases, patients had a mild form: fatigue, cough, low fever. But some scientists suggest that Omicron has a longer transition period from the stage of infection to the stage of possible severe complications. Therefore, uncertainty also persists in this context.

There is only one thing that can be said with some certainty now: Omicron is more contagious and is more easily transmitted from person to person. This information can be interpreted in different ways - depending on how "harmless" the new strain is. If most people carry the disease in a mild form, then the contagiousness of Omicron will "go for good", since it will displace the more dangerous Delta and willy-nilly provide many people with antibodies. But there is another, extremely pessimistic scenario in which Omicron will contribute to a more severe course of the disease, "get away" from antibodies and, again, infect people faster than Delta. This scenario is also not ruled out yet: the final verdict of the WHO will be issued only in a few weeks.

Thus, the further behavior of the EUR/USD pair will depend on how dangerous the Omicron turns out to be. If the risk is high, then many countries of the world continue to be quarantined and massively reduce the number of air traffic. Not only the service sector will be under attack, but also the global economy as a whole.

Trading the EUR/USD pair in conditions of such uncertainty is a "thankless" business. We see that bulls do not dare to go up, taking profits when approaching the 14th figure, and bears do not dare to go down. In my opinion, in the medium term, short positions are still a priority, primarily due to the divergence of the positions of the Fed and the ECB. This uncorrelation has acquired clearer and more categorical forms, therefore, as soon as the "Omicron factor" fades into the background, the EUR/USD bears will significantly increase their pressure, pulling down the price first to the intermediate targets of 1.1250, 1.1200, and then to the main price barrier of 1.1000.