English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Demand for dollar rose amid investor concerns on rising inflationary pressures. The root was the recent surge in oil prices, which reportedly soared to their highest level yesterday because of the global energy crisis. To be precise, WTI hit a 7-year high, surpassing $ 85 a barrel.

But market players are still mindful of the statements made by Fed Chairman Jerome Powell. Last Friday, he hinted at a potential cut in stimulus, reinvigorating expectations on tighter US monetary policy in the near future.

Surprisingly, there are talks that the European Central Bank will go down this path as well, representatives despite expressing their commitment to ultra-low interest rates. Market players are obviously becoming more skeptical lately, ignoring recent warnings from politicians that the central bank is unlikely to change its policy until the end of next year. It seems that it will be up to ECB chief Christine Lagarde to convince people otherwise.

In any case, it is clear that markets are expecting that in three years, deposit rates will rise and return to zero. And with inflation surging, fueled by supply constraints and rising energy prices, they bet that the ECB will join the Federal Reserve in tightening monetary policy. After all, inflation has already exceeded 3%, and it seems that it will continue to grow in the coming months.

However, it should be noted that EU had low inflation rate even before the coronavirus pandemic. So, it is possible that the ECB has more time than the Fed to solve the ongoing issues.

Also, the fact that the central bank is reluctant to cut stimulus indicates their trepidation. Yesterday's report from the Bundesbank confirmed this. Their data showed that problems with delivery weakened industrial production, which, in turn, prevented stronger economic growth in Germany. The bank noted that the easing of restrictions before helped the service sector expand significantly, but due to problems with supplies, industrial production showed modest growth, which affected GDP. The bank's economists said it was the automotive industry that suffered the most. Sadly, macroeconomic activity is likely to weaken more this quarter because of the new COVID-19 outbreak in the region.

Unsurprisingly, business confidence fell to 97.7 points in October, from a revised 98.9 points in September. The index for current conditions also slipped to 95.4 points, from 97.4 points in the previous month. The IFO said supply problems are a headache for businesses, so it is foreseeable that these indices posted declines.

Considering this, it is likely that ECB chief Lagarde will mention new programs to support the economy, especially since the emergency bond purchase program is ending. But as mentioned before, many are expecting rate hikes by the end of 2024. Most likely, by this time, most of the programs to support the European economy will be curtailed in order to prevent its overheating.

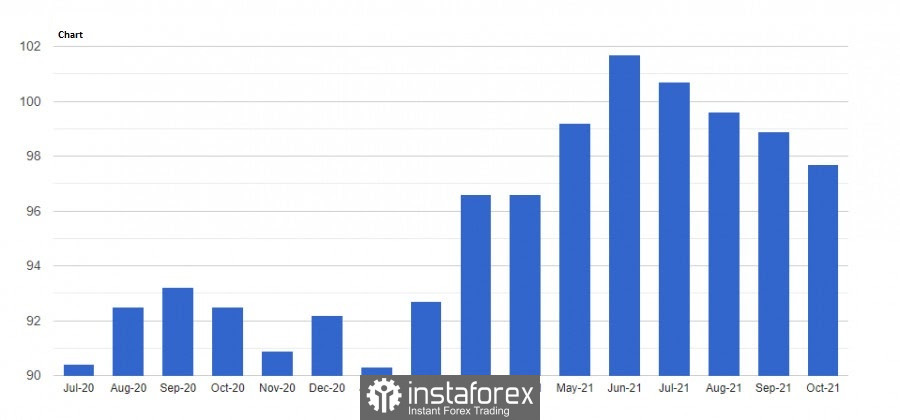

As seen in the graph, the ECB forecasts inflation to exceed 4.0% this year, and then drop to 1.5% in 2023. Most members are not concerned with this score, with Lagarde even saying during the last meeting: "Our forward guidance has already led to a better alignment of rate expectations with our new inflation target. We expect to see further progress in this direction."

Technical analysis on EUR/USD

A lot depends on 1.1590 because failing to breakout will result in a drop to 1.1570 and 1.1540. But the quote goes beyond the level, EUR/USD will rise to 1.1615, and then go to 1.1640 and 1.1670.