English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

A slight growth in risk demand was observed yesterday after Treasury Secretary, Mr. Mnuchin presented a new $ 916 billion stimulus plan to House Speaker, Ms. Pelosi. However, it quickly became clear that there was no desire for a compromise in Congress, and Senate Majority leader McConnell and Senate Democratic leader Chuck Schumer continue to accuse each other of damaging the negotiations.

It should be noted that the recent demand for risk is mainly associated with Biden's victory in the presidential election, since vaccines have long been expected and the market already generally considered the upcoming pandemic relief. However, it turns out that Biden's victory is only clear to his supporters.

On December 7, the state of Texas filed a lawsuit in the US Supreme Court challenging the presidential election results in Georgia, Michigan, Pennsylvania and Wisconsin on the grounds that they violated the US Constitution in the elections. This morning, 17 more states had joined the lawsuit. The Supreme Court accepted the lawsuit, and if the lawsuit is successful, which has quite a high chance, then 4 key states with 62 electoral votes will be deducted from Biden's balance sheet, and electors will appoint the legislators of these states, where the majority is Republican.

However, the markets do not fully understand this news yet. We must assume the possibility of a sharp rise in demand for protective assets. In addition, dollar's prospects may change, which may go up if the news about the trial in the US Supreme Court makes it to the front pages of the media.

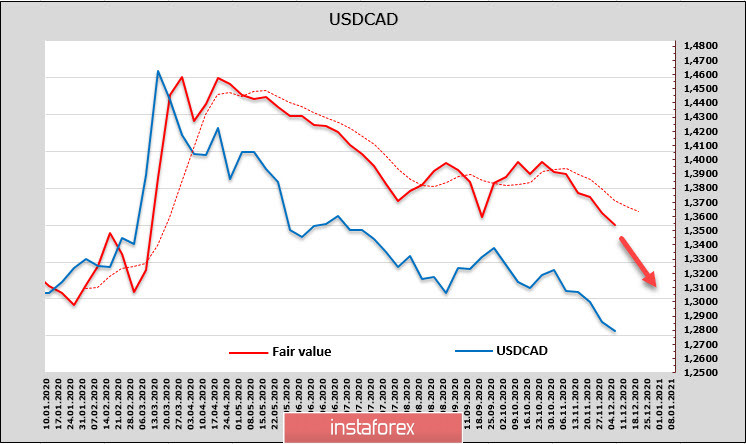

USD/CAD

The Bank of Canada kept the current overnight rate at 0.25%, and the deposit rate also remained unchanged. The QE program is maintained within the current limits, which is about $ 4 billion per week. In an accompanying statement, BoC hopes the pandemic to end soon as effective vaccines have appeared, and notes that the recovery pace in Q3 was in line with expectations.

Moreover, this bank intends to continue its current policy in order to reach inflation of 2%, and assumes that this will happen before 2023. Accordingly, any measures to tighten monetary policy in the near future should not be expected. Thus, the Bank of Canada hinted that there is no intention to change anything in monetary policy, amid Fed's preparation for a new round of QE. This is certainly a bullish factor for the CAD.

Canada's report on employment for November, which turned out to be contrary to a similar report in the US, is pleasant. Thus, the labor market in Canada is recovering more confidently which favors the Canadian currency.

The estimated price is directed downwards and the trend is strong.

The target at 1.2780, which was marked in the previous review, has been reached. The next target is 1.2522, but there is a growing risk of a corrective rollback. It is suggested to sell in case of growth to 1.2930/50, since there are no reasons to close current short positions yet.

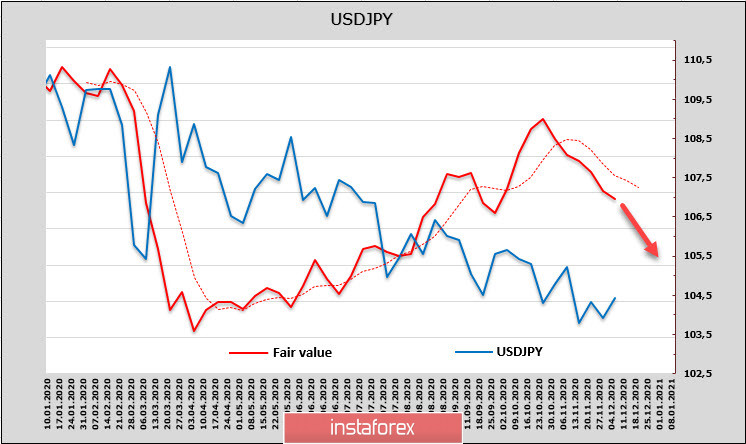

USD/JPY

After a long period of slowdown, positive data finally appeared. GDP growth in Q3 turned out to be slightly higher than expected, while orders for mechanical engineering products increased significantly in October. At the same time, overseas orders rose 20.7% m/m, which should lead to an increase in yen purchases by exporters. However, Mizuho warns that its effect will be temporary, as orders will begin to decline again due to new restrictions.

The estimated price mainly grew from April to October, which gave grounds for a corrective growth of USD/JPY after the failure, but the dollar's weakness was so significant that there was no correction. In the current conditions, there are even fewer reasons for this pair's growth. The estimated price is sharply directed below, which indicates the direction of financial flows from the dollar to the yen.

The current growth is short-term. When the resistance zone of 104.70 /80 is reached, sales will be confirmed with the first target at 103.80/90. An attempt to decline from the forming triangle will follow, so testing the level of 103.19 is likely.