English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Consumer price growth is accelerating around the world. For this reason, the real yield of more independent bonds will be below zero.

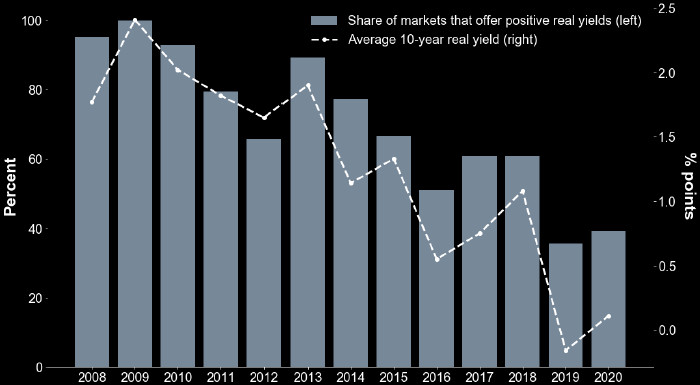

There is no doubt that these processes will intensify the decline in the pool of high yield bonds, more than half of which are issued by developing countries.

According to Bloomberg, only 18 out of 46 emerging economies have 10-year bond margins higher than inflation expected in 2021. Note that at least 90% of these securities are issued by developing countries.

Fidelity International Asset Manager, Paul Greer has pledged to keep inflation low for some time to come, allowing investors to continue looking for the most profitable assets. It is worth noting that the debt of developing countries falls into this category.

The Fed announced a plan in August stating that inflation will be allowed to exceed 2%, and in the future, the current course of ultra-stimulating monetary policy will be adjusted. In his speech at Jackson hole about the fed's transition to a low-inflation targeting strategy, Jerome Powell suggested that low rates will remain at low levels for several more years. This situation focuses on the growth of inflationary pressure.

According to Bloomberg, countries such as South Africa, Brazil, and Indonesia offer real 10-year returns above 4%. While for developed countries like Greece, Italy, and Singapore provide real 10-year returns above zero. High rates of real returns can attract investors to the debt market of developing countries, but this return also implies certain risks. For example, all the above-mentioned countries may sooner or later face a slowdown in economic growth and political instability.

In the coming years, some of the world's largest emerging economies will inevitably face a financial crisis related to the coronavirus pandemic. Rising health spending to fight the spread of the virus is driving the rapid growth of budget deficits in developing countries. So, the budget deficit in Brazil and South Africa in 2020 is more than 15% of GDP (according to Oxford Economics). Moreover, the need to refinance debt with an upcoming maturity will increase their need for borrowed funds to 25% of GDP this year. According to a recent report by Bloomberg Economics, South Africa's financial situation has the most unfavorable prospects today, and the country's economy is facing a period of sluggish growth. As for Brazil, the government's decision to give out cash directly to the population of the country is in danger of violating its financial sustainability. Indonesia, whose Central Bank purchases sovereign bonds on the primary market, is in a similar situation today.

According to Nick Eisinger, head of active operations in the debt market at EM Vanguard Asset Management, several bullish scenarios for developing country bonds are possible. First, the influx of high-yield hunters ' funds into this market. Second, there are good opportunities in the remaining high-yield bonds in the global economy with a positive credit history.