English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The single European currency has not fully realized what a gift the ECB has given it. Ahead of the September meeting of the Governing Council, investors were racking their brains over how Christine Lagarde would put pressure on the euro. Show concern about slowing inflation? Hint at an extension of QE? Will she say that the EUR/USD rally is causing concern for the European Central Bank? None of this happened. The main currency pair confidently moved up, however, the fear of falling into a trap forced the "bulls" to fix profits.

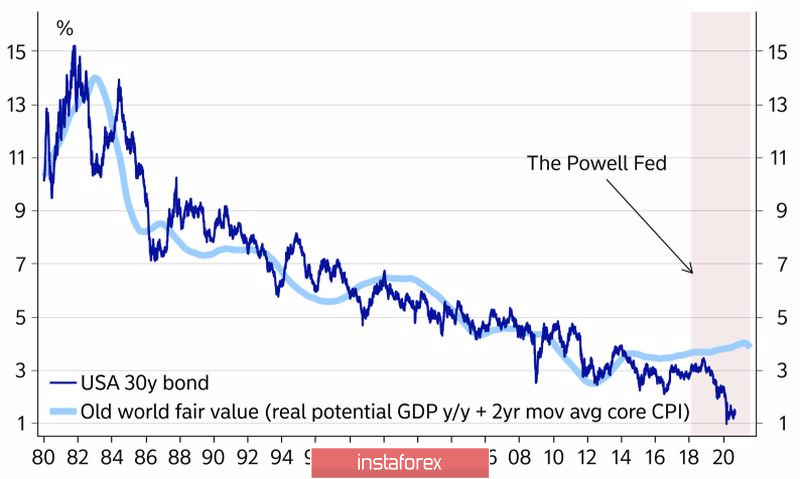

It must be admitted that Lagarde managed to achieve her goal: despite the absence of pronounced "dovish" notes in her rhetoric, the euro could not restore an upward trend against the US dollar. According to some members of the Governing Council, the success of EUR/USD is to blame not only for the rapid recovery of the Eurozone economy and increased confidence in the EU due to the correctly chosen strategy to combat the pandemic, but also for the large-scale monetary expansion of the Fed. This certainly makes sense: the Fed has flooded the US debt market with cheap money. Treasury yields have fallen so low that they do not reflect the positive processes that are taking place with US inflation and GDP.

Dynamics of bond yields and the combined US economic indicator

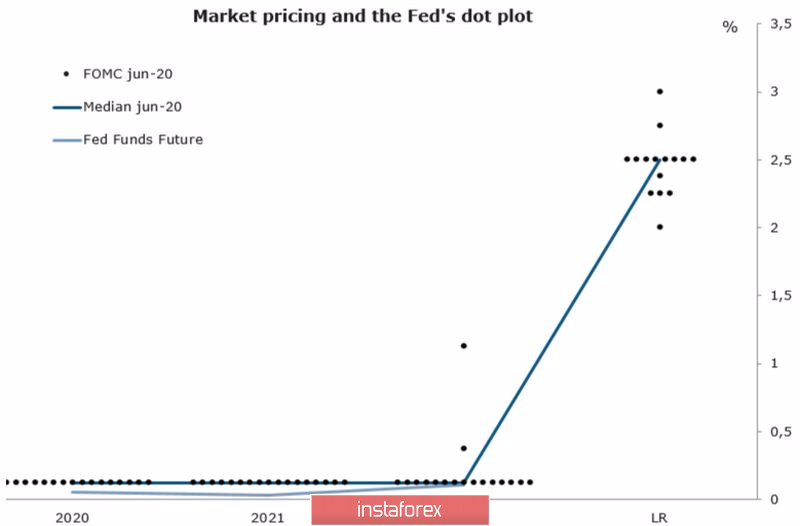

Investors' attention shifted from Christine Lagarde to Jerome Powell, who gave the economy so much stimulus. At the same time, the market has sharp questions for the Fed Chairman, including: to what level does the Central Bank intend to tolerate inflation, what will the Fed do to speed it up, and, finally, will the forward guidance on rates be officially changed? Although most FOMC members approved of the idea of targeting average inflation, some were dissatisfied with it.

To what level will the Fed allow the personal consumption expenditure index to grow? Up to 2.3%? Or up to 2.5%? It all depends on the calculation base. As for the acceleration of inflation, the strategy of keeping the federal funds rate low contributes to the growth of inflation expectations. Most likely, in the FOMC forecasts for 2022, none of the members will expect that borrowing costs will increase.

July FOMC rate forecasts

If the ECB is not concerned about the strengthening of the euro, and the Federal Reserve is rightly considered the largest "dove" in history, then the fate of EUR/USD seems to be a foregone conclusion. "Bulls" are simply obliged to restore the upward trend, however, it is blocked by fears due to the second wave of the pandemic in Europe, the correction of US stock indices, and the associated increase in demand for safe-haven assets, as well as due to Brexit. The consequences of a divorce without an agreement will be terrible for both Albion and the Eurozone.

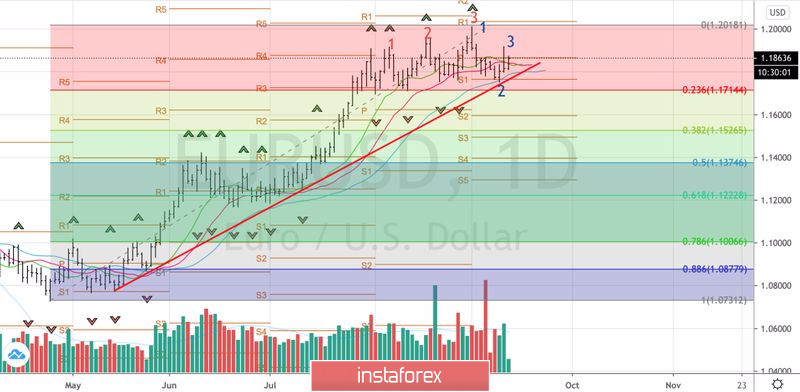

Technically, the formation of a combination of patterns 1-2-3 and "Three Indians" indicates a high risk of a correction in the event of a breakout of support at 1.18 and 1.76. Their successful assault will allow you to form shorts. On the contrary, the growth of EUR/USD quotes above the local maximum at 1.1915 will be a signal for purchases.

EUR/USD, the daily chart