English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

between the US and China on the trade dispute, most experts are inclined to conclude that no changes have occurred globally, and the prospects remain gloomy.

Mizuho Bank assumes that things will not go further than a short-term interim agreement, while Nordea emphasizes that the global recession is not a consequence of Trump's trade war, but has deeper reasons. The solution of which is unlikely at the current stage. The general mood of the Chinese media remains pessimistic. In addition, Danske Bank notes that the agreements reached do not relate to previously introduced tariffs, as well as another increase planned for December.

Today, the September report on the state of the US budget will be published. According to the CBO, the deficit in fiscal 2019 increased by 205 billion to 984 billion, which is 4.7% of GDP. Cost growth is still ahead of revenue growth, which, against the background of the expected drop in consumer demand, does not allow the Trump administration to abandon attempts to shift part of the costs to trading partners.

EUR/USD

In November, the ECB will resume net asset purchases, and this is a bearish factor for the euro. However, all the negativity is completely offset by the Fed's intention to start buying T-bills immediately at $ 60 billion per month, with an estimated duration of 8.5 months which is equivalent to a new QE wave of 510 billion.

The Fed also explains its actions with the intention "to maintain sufficient reserve balances for a long time at or above the level that prevailed at the beginning of September 2019." That is, the Fed does not formally announce the QE program. Again, if the target is the reserve level, then the price 60 billion purchases may change at any time.

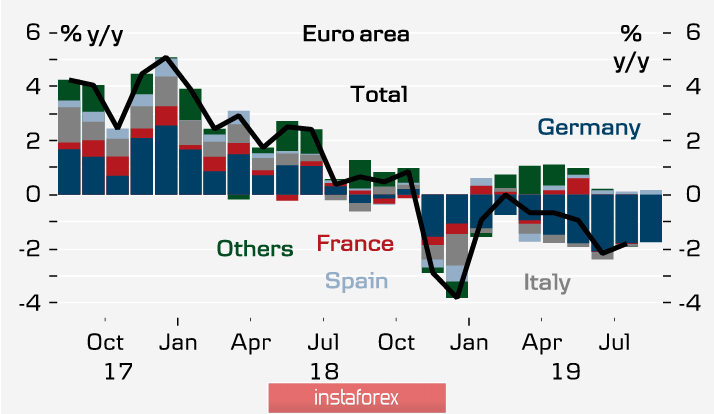

These intentions of the Fed cause significant confusion in assessing the prospects - the long-awaited soft decision of the ECB, aimed at supporting primarily industry, is more than overlapping with the plans of the Fed. It would seem that the euro should continue to recover, however, recent macroeconomic data do not support the growth of the European currency. The level of industrial production in the eurozone fell in August from 2.1% y / y to -2.8% y / y, which is the largest decline is observed in Germany.

Today, the ZEW business sentiment index will be published. A further decline is expected, which under other conditions would be regarded by the markets as a factor contributing to the decline of the euro. However, the players appear to be going to ignore the release, since they come from the real threat of another Fed rate cut in October. An increase in the supply of dollar cash and the absence of clear signs of US confidence in a trade dispute with China. A sure sign of a change in mood is a reduction in the spread between the 10-year Treasuries and the German Bundeswehr, which gives us the right to assume that EUR/USD will continue to grow at the current stage.

As expected, the euro went above 1.10, however, resistance at 1.1052 (50-day SMA) could not be overcome on the first attempt. More so, a decline in support of 1.0940 is unlikely, rather after a short consolidation, another upward impulse will be formed with the target of 1.1107.

GBP/USD

Consultations on Brexit, before the EU summit starting this week, reached the finish line. Apparently, the establishment of a customs border in Ireland is inevitable. The surge of positive on this news turned out to be strong, but not long, since the technical side of the solution to this problem is still completely unclear.

The probability of leaving the EU on October 31 increased from 15-20% to 30%, and the pound has good opportunities to continue growing this week, which will be facilitated by any positive Brexit news. At the same time, it is obvious that the UK economy is close to a recession, which means that after November 1, the Bank of England will be untied in connection with the disappearance of uncertainty, and plans to mitigate monetary policy will become obvious.

The pound leaves the zone of high volatility and waits for news. In the coming days, consolidation is most likely near the maximum of 1.2705 reached on the evening. This is a strong resistance formed by the 200-day SMA. Support is 1.2580. In case of information leakage about agreements, a breakthrough to 1.2820 / 40 is possible, but it will be an emotional surge, not supported by macroeconomic indicators.