English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Trade negotiations between the US and China resume on October 10, and there are no signs that the Chinese leadership is ready to sacrifice its own ambition projects in favor of the deal.

Yesterday, stock indices are traded in the red zone. The S & P500 lost more than 1.5%, and, as Nordea notes, the stock market underestimates the consequences of the recession on a noticeable decline in world trade. In this regard, further growth in demand for gold is expected as the most reliable protective asset.

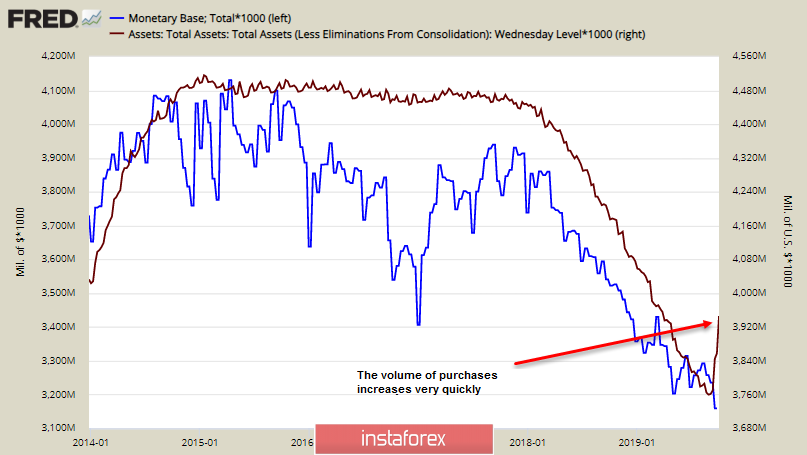

The US Federal Reserve has started buying treasuries again, and although Jerome Powell emphasizes that these purchases are just a "balance sheet" and not a new round of quantitative easing, there is a growing understanding in the markets that asset repurchases are likely to continue.

The monetary base has not yet shown growth, but it is a matter of time. An increase in the monetary base, in turn, will lead to the fact that the dollar exchange rate can begin to decline not only under the pressure of objective reasons, such as a decrease in the Fed rate and a further increase in the trade deficit, but also as a separate measure that aims precisely to reduce the dollar exchange rate in order to delay the onset of recession.

USD/CAD

The Canadian dollar, as expected, has moved to the resistance zone of 1.3300 / 50 and is consolidating.

Oil is still below $ 60 / bbl, and recent macroeconomic indicators point to a growing recession threat. On the other hand, GDP growth in July fell to zero, with a marked fall in the manufacturing sector, which was offset by growth in the services sector.

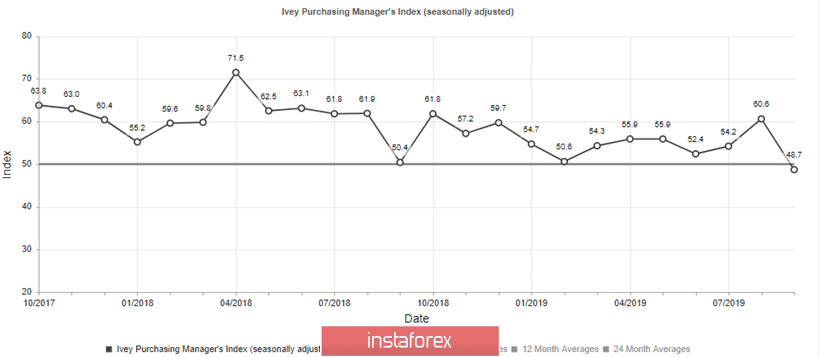

In addition, the PMI Ivey index fell sharply in September from 60.6p to 48.7p. The decline is accompanied by a leading fall in the employment index, which indicates that companies are starting to reduce staff before the threat of further slowdown.

On September 11, an employment report for September will be published. The trend is negative and there is a high probability that the growth rate of employment will fall faster than forecasts. A weak report will also put pressure on the loonies, thus, USDCAD may exit from the consolidation zone upward by the end of the week. The probability of a breakthrough of resistance 1.3380 is increasing. The target is the resistance zone 1.3413 / 33.

USD/JPY

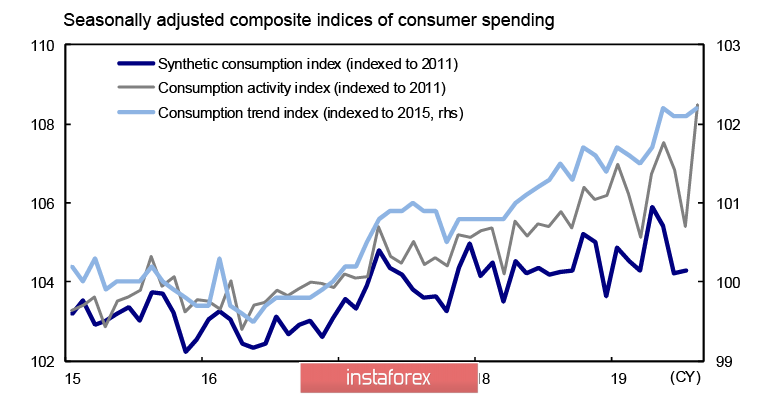

A study of income and expenses for August, published on October 8, shows an increase in real spending on consumption by 1.0% y / y. This is the ninth consecutive month of growth, which is the longest period since the survey began in January 2001. Seasonally adjusted spending rose 2.4% for the month in August. The numbers can be considered an indicator of the unexpected power of consumer spending.

At the same time, Mizuho Bank notes that survey results are often distorted by sampling rules and indicates that there are several synthetic indexes that provide a more accurate picture of real consumption.

Among the most widely used are the Cabinet of Ministers Consumption Index and the Bank of Japan Consumer Activity Index. MIC also publishes the Household Consumption Dynamics Index (CTI micro), based primarily on a survey of income and expenses, as well as the wider Consumption Dynamics Index (CTI macro). By analyzing these indices, Mizuho comes to the conclusion that a substantial, steady increase in consumer spending is out of the question, while real wages per capita remain without signs of growth, and the consumer confidence index continues to fall.

From this, it is clear that the threat of the further introduction of incentive measures continues to remain high. Most likely, it will become clear in the near future that raising the consumption tax rate to 10% does not increase inflation expectations, which means that the Bank of Japan will look for ways to stimulate demand through easing monetary policy, which will also be reflected in attempts to prevent the yen from strengthening against the background approaching global crisis.

The trend for USD/JPY remains downwards. The yen does not attempt to rise above the 200-day SMA and most likely, consolidation is bound to end with the resumption of the movement to support 105.05.