English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Eurozone

On June 14, the ECB will hold a regular meeting on monetary policy. Throughout the previous week, ECB officials expressed their views on the upcoming meeting, and if the markets were convinced, it is that the time of rate hikes is approaching.

The euro reacted to the change in expectations as the probability of the first rate increase in June 2019 rose from 30% to 90%, that is, the markets see the ECB's fairly clear action plan - the completion of the asset repurchase program in December 2018, then a half-year break to assess the situation and offset possible fluctuations, after which the period of rate increase will begin.

Numerous media outlets last week from "anonymous sources" give such a prospect - a full discussion on the winding up of the buyback program begins on June 14, forecasts for the economy will be lowered, but inflation is raised due to rising oil prices and good expectations on private consumption.

There is another reason why the Euro may accelerate growth – the ECB needs to exit soft monetary policy on time, and in light of the deteriorating prospects for trade with the US, inflation may be temporary or weaker than expectations, so they need to use the "window" in the next six months to change policy.

The euro in the current conditions gets a boost to growth and enjoys it. The potential for growth remains at 1.1930, especially if the outcome of the Fed meeting disappoints the markets.

Britain

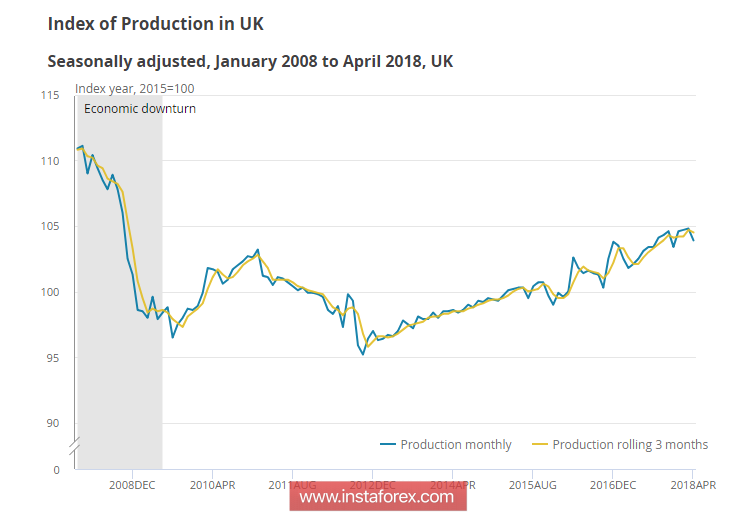

The pound at the opening of the week looks weaker than the euro and is unlikely to grow against the dollar. Published data on industrial production were much worse than forecasted. In April the decline was 0.8% with the forecast + 0.2%, the fall in the manufacturing industry was even deeper, in April -1.4, on an annualized basis, the growth slowed to + 1.4% vs. + 2.9% a month earlier .

Negative was the report on trade - the total trade balance fell to -5.28 billion pounds in April, the worst since October of last year, the deficit in trade in goods increased, while all these indicators were expected to grow, not fall.

Approaching the formal date of the UK's exit from the EU increases nervousness. The probability of a domestic political crisis has increased, the idea of a second referendum is not understood, and the probability of a tough Brexit, that is, the exit from the single market and the customs Union, is growing every day.

The basic economic indicators do not show any improvement after the Bank of England refused to raise the rate in May, this pushes out the probability of an increase by the end of the year and worsens the outlook for the pound.

On Tuesday, a report on the labor market in May will be published, special attention should be paid to the growth rate of wages, on Wednesday - an inflation report. Good data will help the pound stay on current positions, but it is more likely to resume the decline and retest the 1.32 level by the middle of the week.

Oil

Despite a number of negative factors, oil finished the week near the highs. The main factor that constrains growth is the expectation of the OPEC meeting + June 22, as it is expected to announce an adjustment of the restrictions to increase them. In favor of such a decision, Russia and Saudi Arabia are ready to speak, against Iran and Iraq. At the same time, one must give an account that the main task of OPEC + is not the price increase or even the stabilization of stocks, but the creation of a mechanism in which volatility will decrease, since it is the increased volatility that is the main destabilizing factor in the market as a whole.

Reduction of Brent to the limit of the channel at $ 71 per barrel. looks logical, especially if the dollar is strengthened after the FOMC meeting.