English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

For the first time since December, gold went beyond the trading range of $1300-1360 per ounce against the background of the growth of the yield of 10-year US Treasury bonds to 7-year highs. Strong statistics on American retail trade in April made investors believe in a bright future of the world's leading economy and the aggressive monetary tightening of the Fed. The probability of four increases in the Federal funds rate in 2018 for the last month increased from 39% to 53%, which brought the dollar back to life and put an end to the attempts of "bulls" for the XAU/USD to restore the upward trend.

The rally of the US debt market rates, the probability of a rapid normalization of monetary policy and a strong "greenback" is a rattling mixture that forces speculators to close long positions on the precious metal. At the end of the week by May 1, they were reduced to 51,895 contracts, which is the minimum for the last 9 months. From the outside, it looks like the dominance of the "bears", however, since 2015 there have been 5 cases of reducing the number of contracts below 100 thousand, and each time the" bulls " went into a counterattack and raised prices by an average of 4.8% over the next 50 trading days.

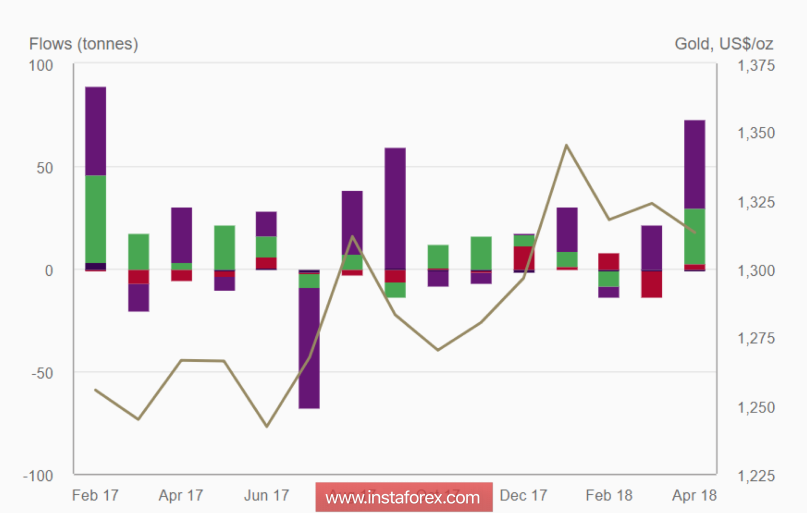

The fall in XAU/USD does not particularly bother the fans of ETF. In April, their reserves increased by $3.1 billion, which is the highest figure since February 2017. Suppose that the futures market does not react to the acceleration of US inflation, permanent geopolitical tensions in the Middle East and around North Korea, the risks of a large-scale trade war between the US and China, but investors continue to buy physical gold.

Capital inflows in gold ETF

According to the analysis of the World Gold Council, the demand for precious metals in the first quarter was the weakest in the last decade, and coin sales by the US Court fell to the lowest level since 2015. At the same time, bulls of the XAU/USD sincerely hope that the physical market has reached the bottom, which will lay the foundation for a gradual recovery of prices to the levels of record highs of 2011. The difference between them and the current value of the precious metal is approximately 32%.

It is is very difficult for non-dividend paying gold to compete with securities, and the strengthening of the US dollar leads to a rise in the cost of imports in countries that are major consumers of the metal, which is reflected in the fall in demand. At the same time, we should not forget that since the beginning of the Fed's monetary policy normalization cycle in December 2015, futures prices have increased by 23% due to the periodic implementation of the principle "sell on rumors (on the eve of the Federal funds rate increase), buy on facts". The futures market is almost certain of its growth of up to 2% at the FOMC meeting on June 13, so gold will likely be under pressure until that moment.

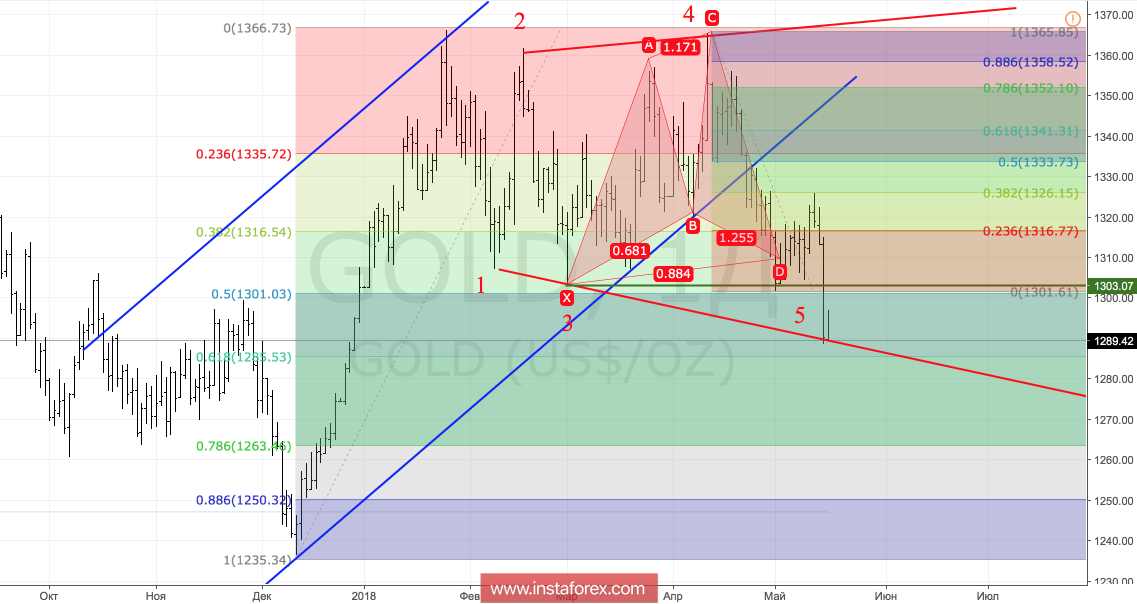

Technically, well-established "broadening wedge" patterns and 5-0 brought futures quotes beyond the range of medium-term consolidation of $ 1300-1360 per ounce and allowed the "bears" to count on the continuation of the peak in the direction of $1285 and $1263.

Gold, daily chart